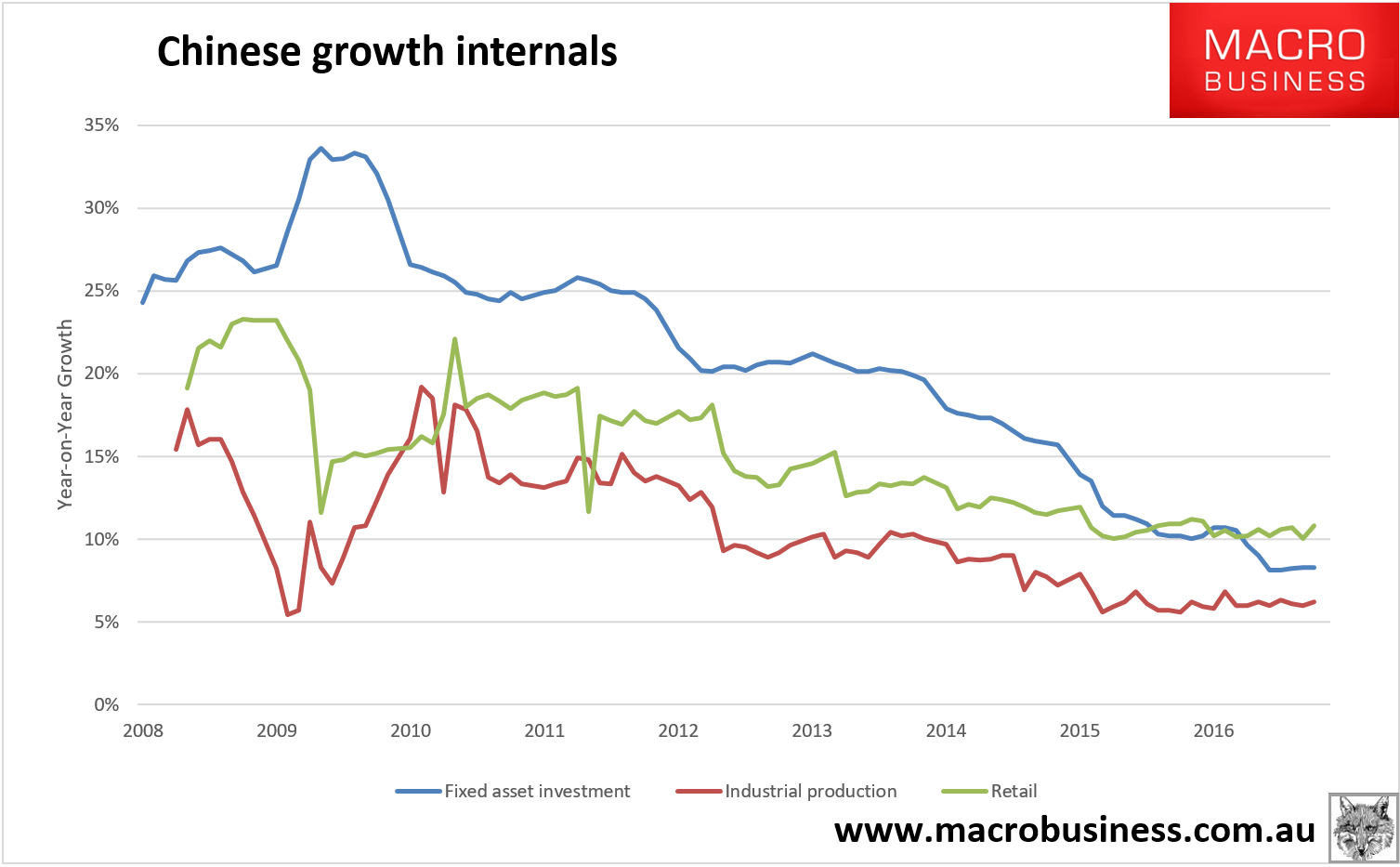

China’s November data dump is out and shows few surprises with Industrial Production growth stable at 6.2%, Fixed Asset Investment growth steady at 8.3% and Retail Sales rebounding a little to 10.8%:

A picture of stability.

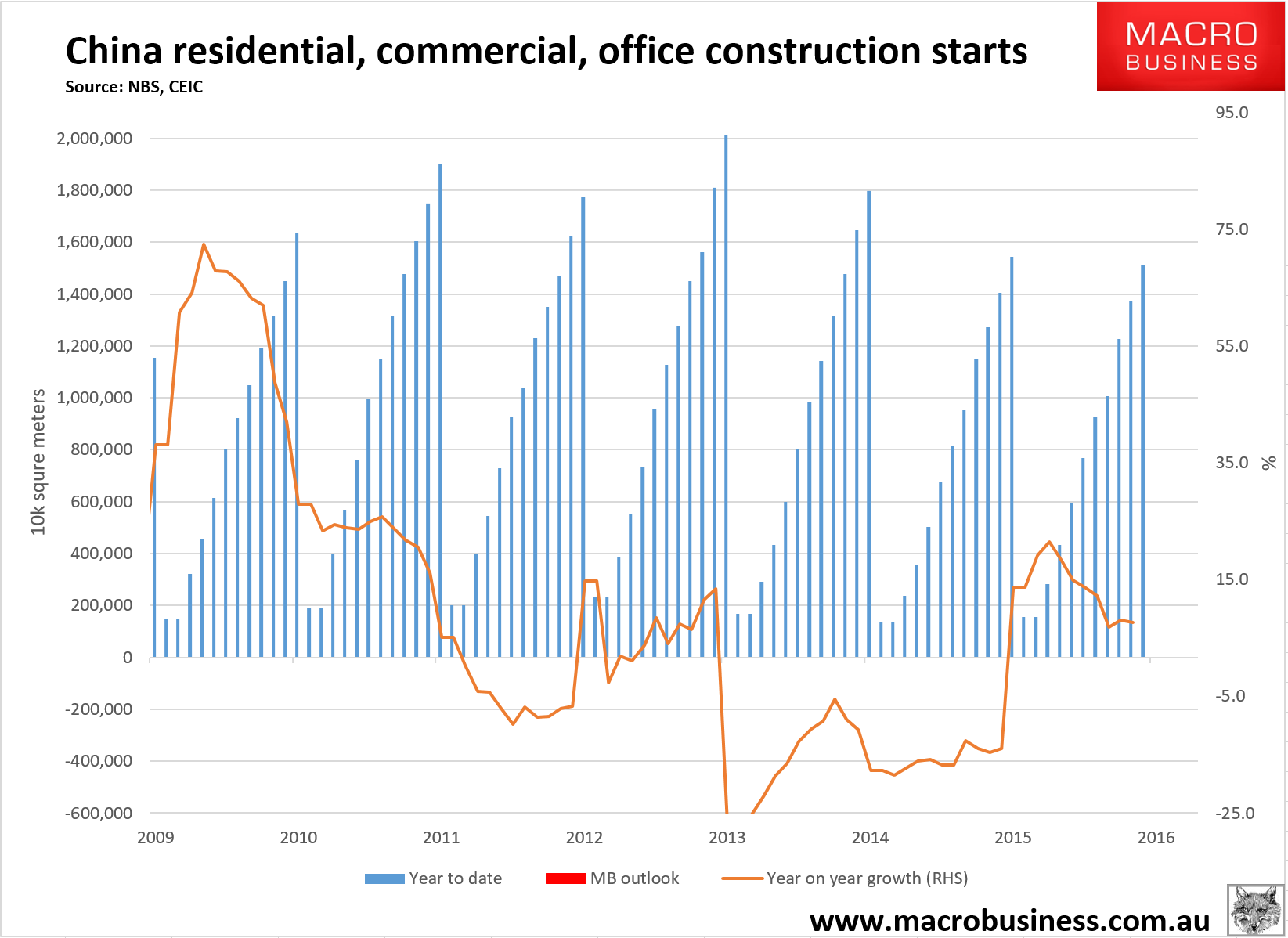

Digging into the all-important real estate statistics we find new construction starts resuming their growth fade down from 8.2% to 7.6% year to date:

I still expect this keep fading but obviously it’s going to put in a decent year over year growth performance. Moreover, sales are still 24.3% year to date so I’m not expecting a collapse by any means.

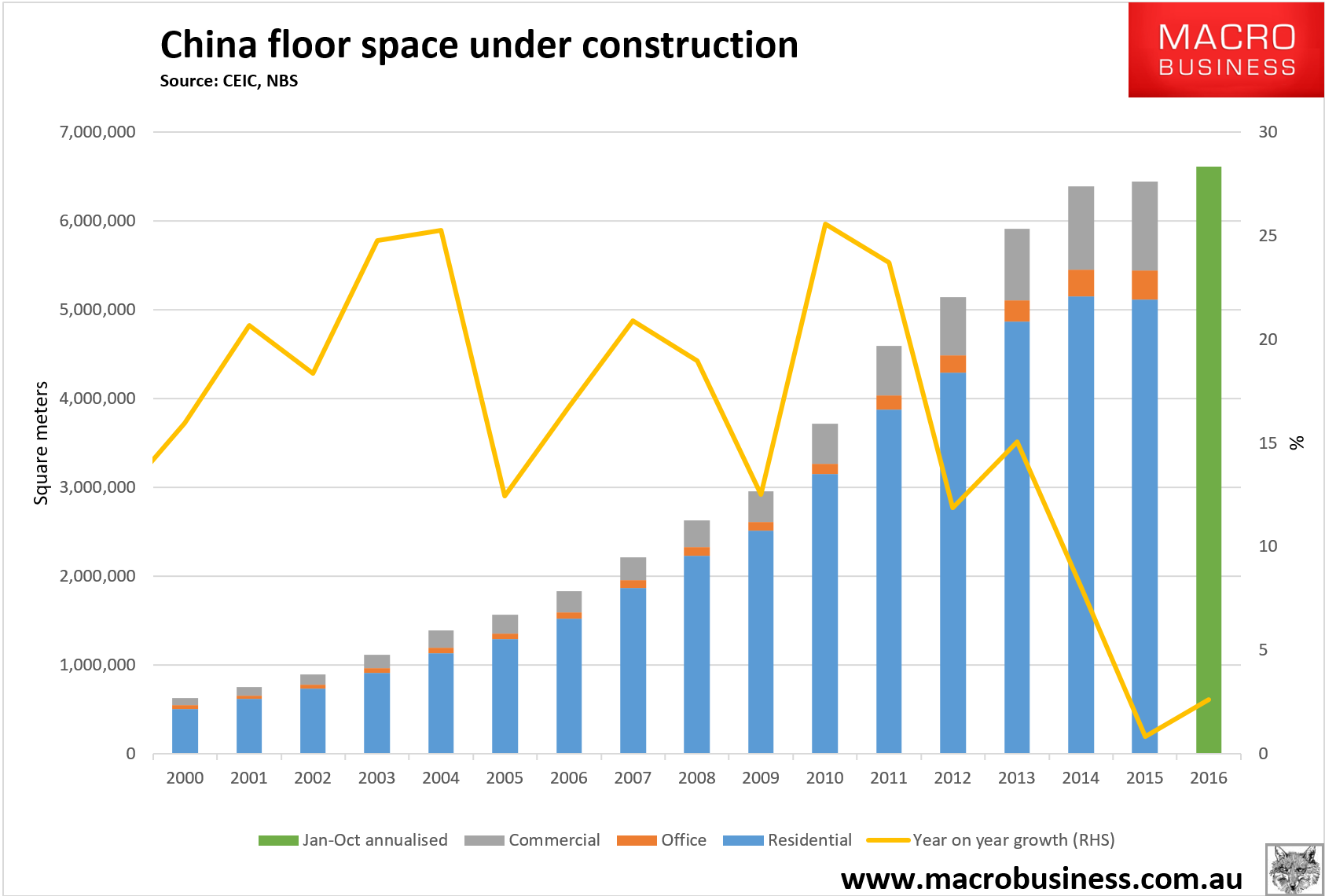

The stock of Chinese floor space now under construction is up 2.6% year to date:

Again, we’re going to finish the year with a little growth.

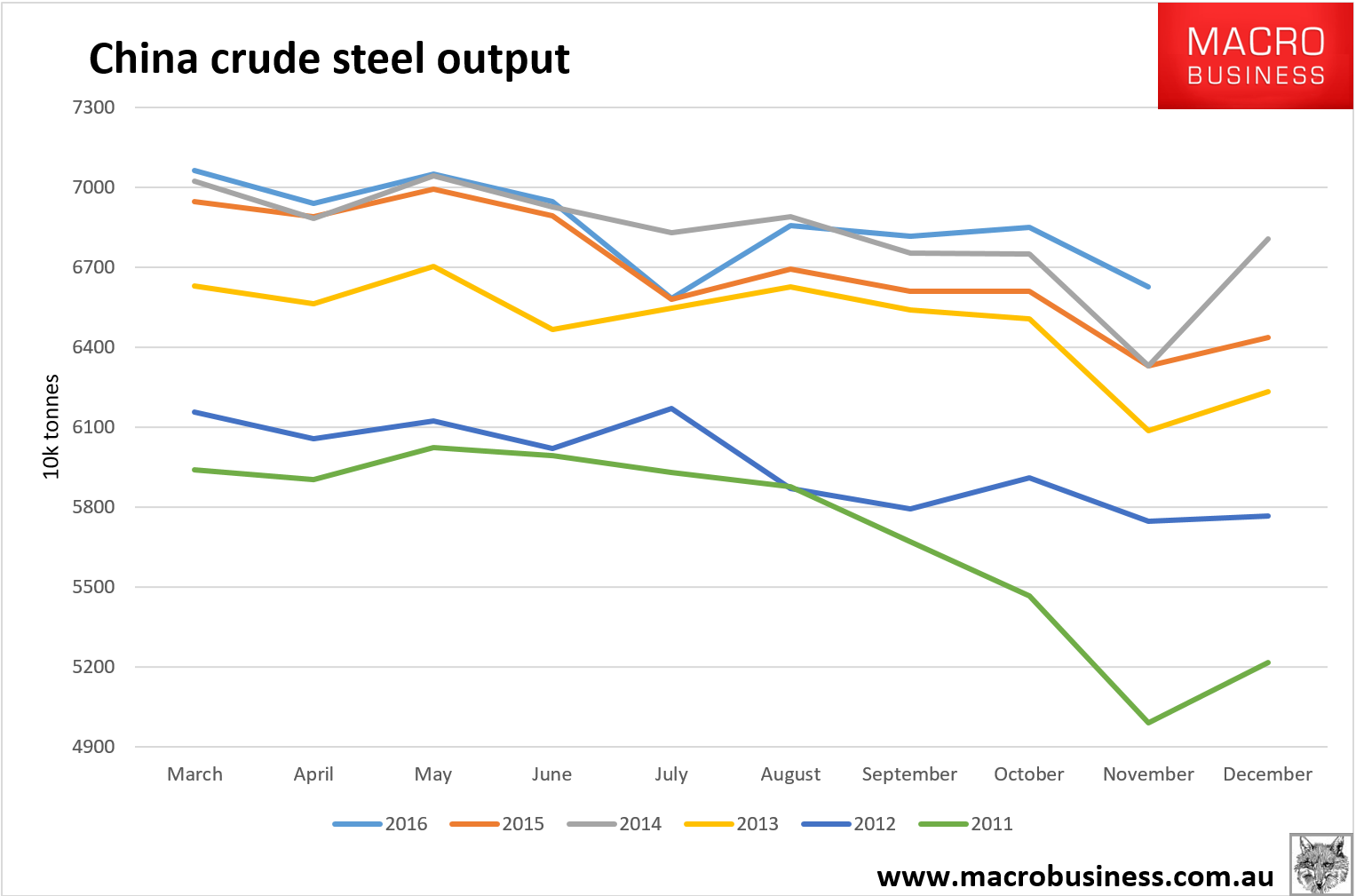

Turning to industry, steel production is still thumping along at 66.3mt, up 5% year on year for another record month but a more subdued 1.1% year to date:

Looks like we’re going to end the year with roughly 10mt growth. Nowhere near enough to justify the current iron ore price.

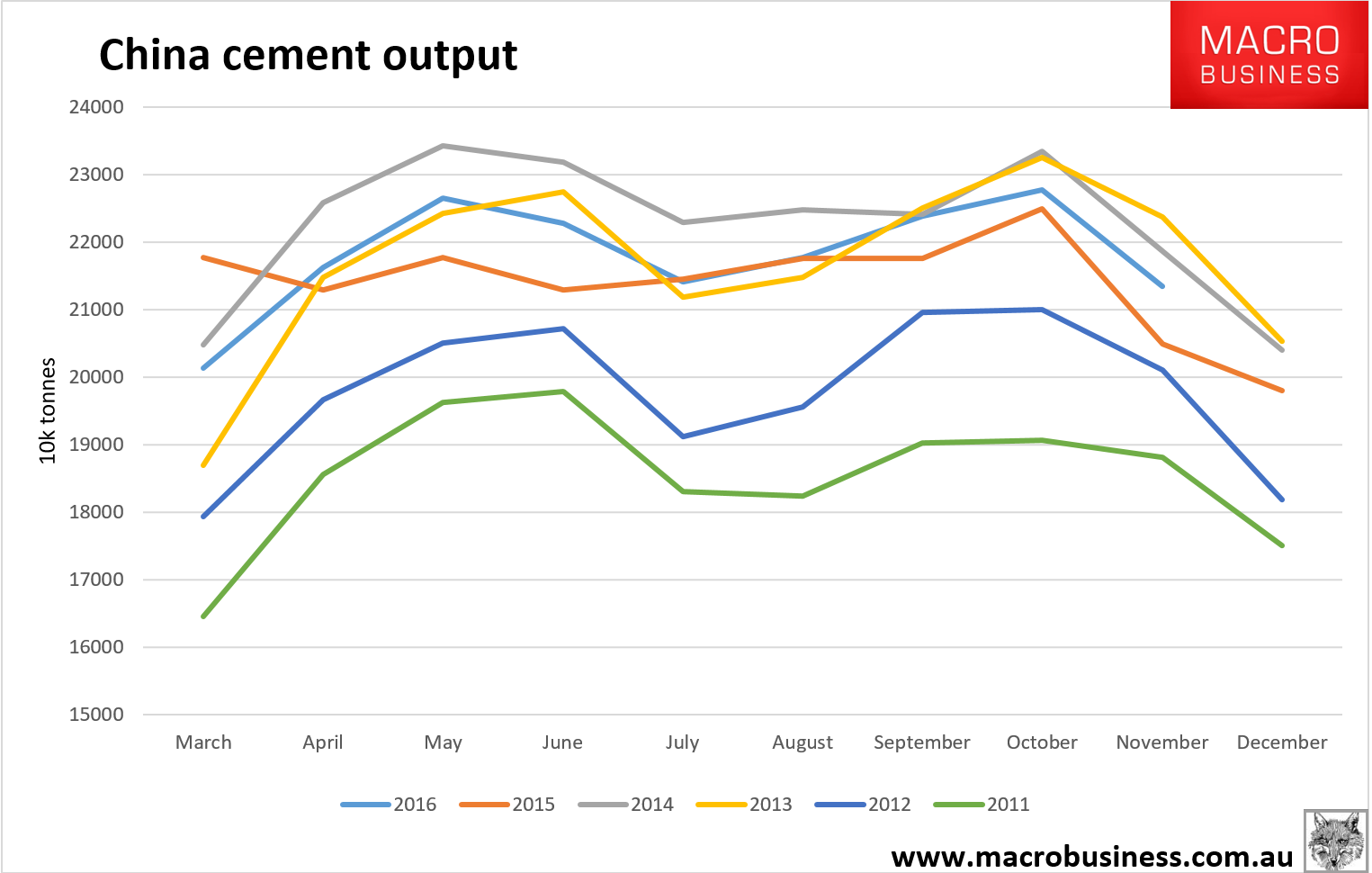

Cement is demonstrating a strong but less bullish picture:

The difference between the two is still high steel exports.

So, in sum, China is thumping along just fine. The seeds of slowing in the construction economy are there but green shoots only (if you’ll pardon the inversion).