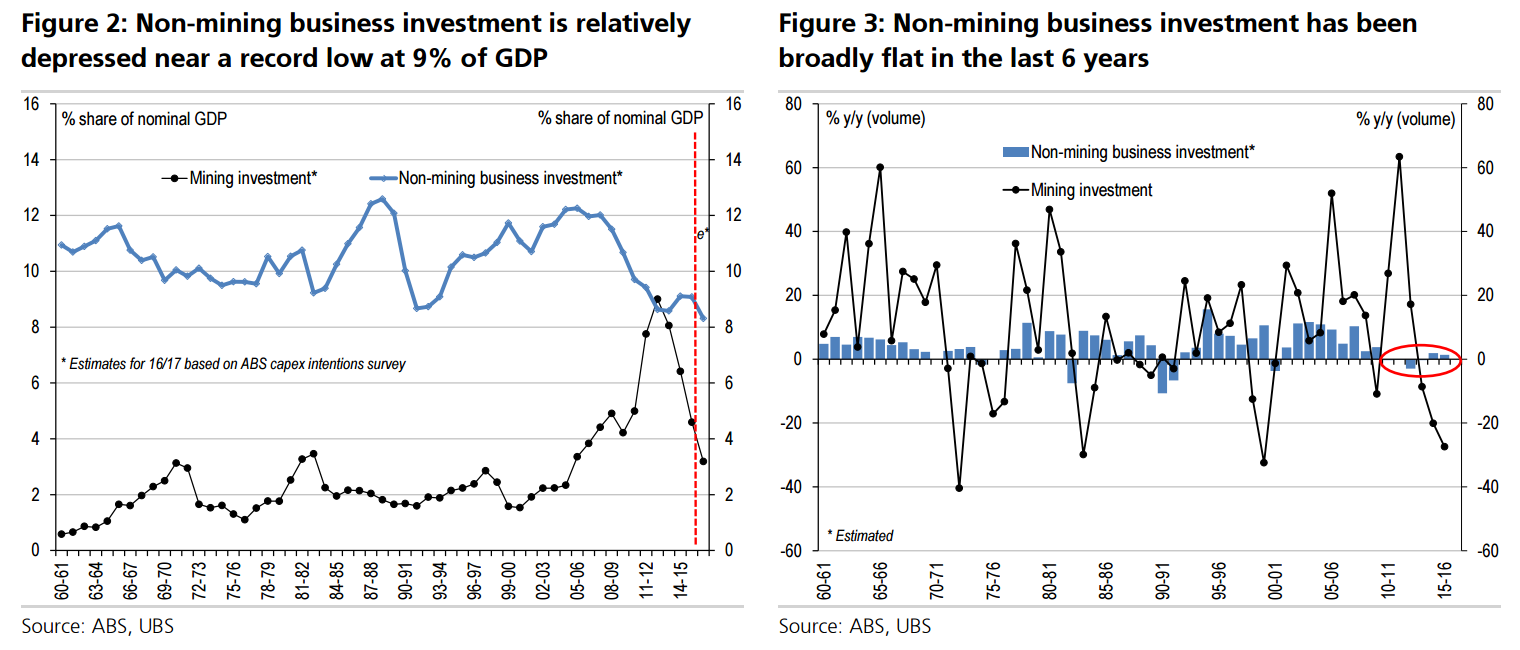

Non-mining business investment has been relatively weak since the GFC, with its current 9% share of nominal GDP near the lowest on record (Figure 2), and real activity showing no (net) growth in the last 6 years (Figure 3). Indeed, construction and capex ‘partial data’ showed a (largely unexpected) sharp drop in Q3-16.

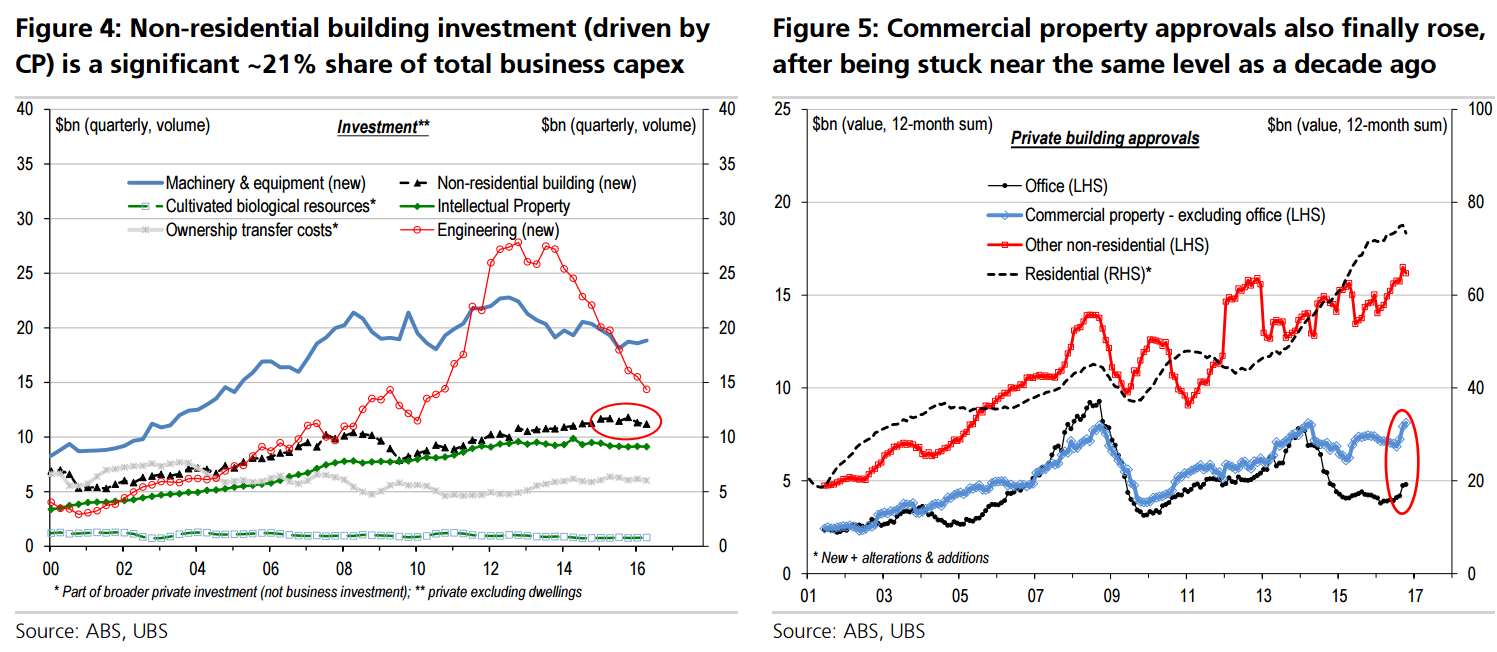

However, the key leading indicator of private non-residential building approvals spiked in recent months to a record high (albeit still only ~1% of GDP, vs dwelling investment near ~6% of GDP), its best uptrend since the GFC (Figure 1). Given its strong causality to non-residential building investment – a significant 21% of total capex, but still the ~same level as its pre-GFC peak (Figure 4) – this suggests activity should rebound sharply in coming quarters (post a likely drop in Q3-16). Within non-residential approvals, there is broad improvement over recent months. Notably, commercial property (the largest sub-category) also finally rose, after being stuck near the same value as a decade ago (Figure 5). Indeed, even offices edged up, albeit still only ~half the pre-GFC peak. (In contrast, residential approvals peaked.) By State, approvals lifted most in NSW & Victoria (Figure 6).

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.