The MYEFO remain center-stage today as we wend our way through Australia’s grey-beard commentary responses. The tone is, as usual, soothing. Alan Kohler is a picture of nonchalance:

Standard & Poor’s was looking to the MYEFO for a reason not to downgrade Australia; Moody’s and Fitch were looking for a reason to do it.

It seems none of them were given an excuse to pull the trigger. The most eagerly anticipated MYEFO for years turned out to be a non-event: move along, nothing to see here.

S&P remains the most likely to downgrade and Moody’s and Fitch less so, at least for a while. In 1986, Moody’s went first, in September, and S&P followed in December, but the statements from all of them immediately after the MYEFO release rule out any move for the time being, at least until the May budget.

Even if S&P does downgrade next year, it won’t be a big deal. It would be unlikely to add to the government’s borrowing cost at all, and would add no more than 15 basis points to interests cost on the banks’ foreign borrowings, which represent a third of their funding needs.

So the great downgrade hoo-ha of 2016 has turned out to be a non-event, although of course there continue to be efforts by the opposition to whip it up.

Also, Ross Gittins is positively smug:

To tell you the truth, I’m sorry it didn’t fall this week. That’s not because I bear the government any ill will, but because the sooner we’re downgraded, the sooner the public will realise there’s little to fear from a downgrade. The ratings agencies are toothless tigers.

In any case, there is no good reason any sovereign Australian government – federal or state – should allow a few American for-profit businesses to dictate how much it should or shouldn’t borrow (nor engage in hugely expensive ways of disguising the true extent of its liabilities).

The ratings agencies’ credibility has been destroyed by their part in the global financial crisis. Not only did these all-wise experts fail to see it coming, they contributed to the conflagration by awarding AAA ratings to the promoters of “collateralised debt obligations” – for the small fee – that soon turned into “toxic debt”.

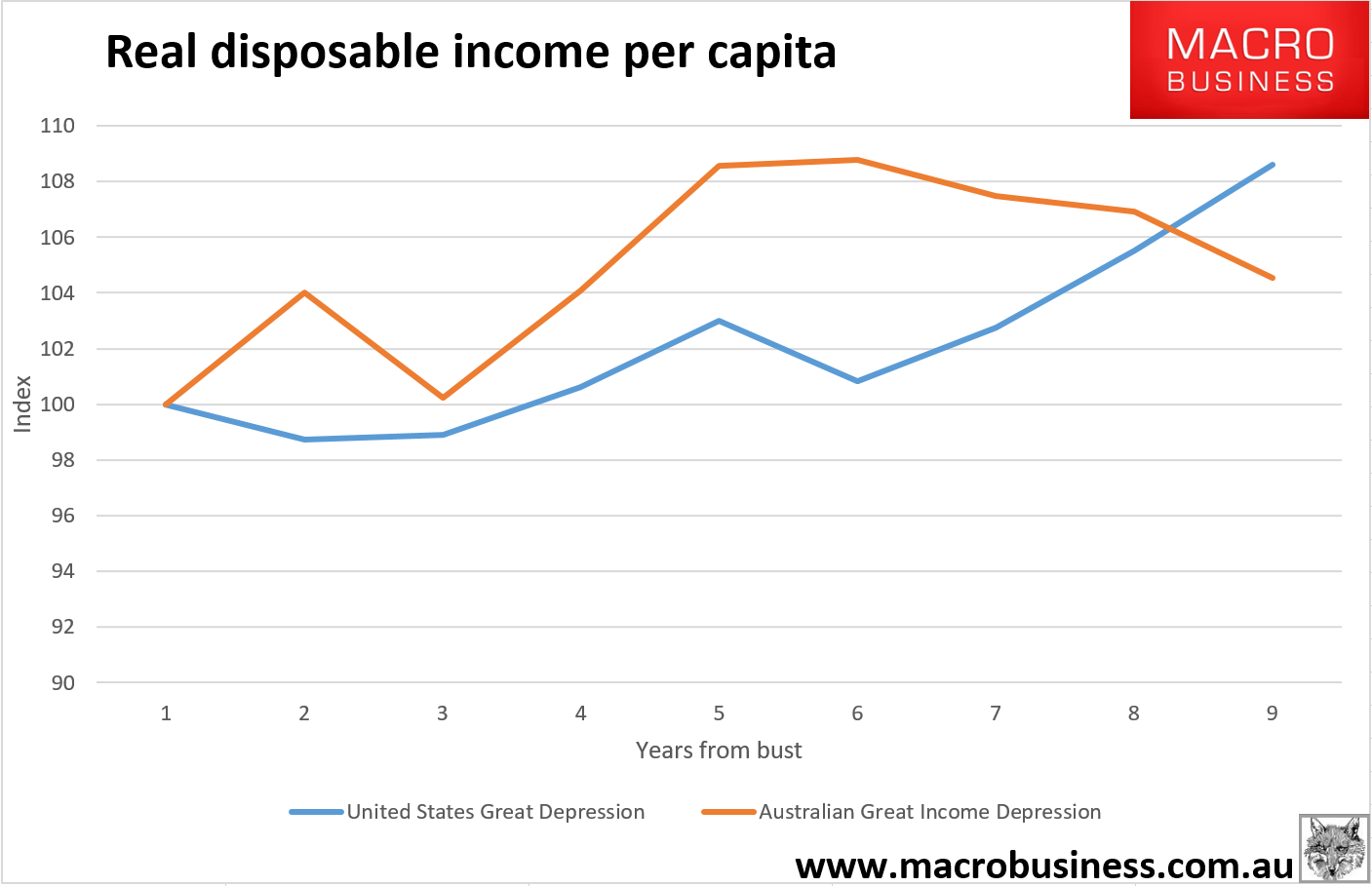

So when is Australian deterioration a problem, grey beards? We’ve been chronicling this story for nearly decade now, warning repeatedly about the structure of the economy leading inexorably to the decline of Australian standards of living, an exemplar of which is the deteriorating national balance sheet. We’ve been right the entire time as Australian standards of living passes through a period with an end result worse than the US Great Depression yet here we are, plodding past milestone after milestone in a relentless national decline, with the same soporific drivel spouted from our ostensibly leading voices:

When does it become urgent, grey-beards? If it’s not the first downgrade, is it the second? Is it the third or fourth? Is it when we wake one morning and Alan Kohler declares from his prosperous tower with righteous indignation and goldish-like unmemory that Australia is the new Argentina?

The truth is, these commentators long ago abandoned any ethos that can ever tell you where we are at or going. Alan Kohler comes and goes between Baby Boomer servicing investment businesses that do not respond well to the truth of fading prospects. Ross Gittins is the titular head of Domainfax, the former liberal titan of Australian press turned bald-faced real estate spruiker. Like so many of their generation, both are so busy feathering their nests that the public good long since ceased to matter.

At least one old man today offers some urgency to address the great Australian fade out. Paul Kelly responds to recent MB prodding with a better effort:

This is not what real victory looks like. The mid-year economic and fiscal outlook is about survival but that does not constitute victory. The Turnbull government, courtesy of diligent housekeeping, now goes to Christmas having escaped the threatened AAA credit rating downgrade, earning a reprieve until the May budget.

The idea that Scott Morrison can perform another escape next May, with more of the same, is remote. The government faces the exhaustion of the incremental budget strategy it has pursued since the 2014 Abbott-Hockey budget. The comment from S&P Global Ratings rang the bell: “We remain pessimistic about the government’s ability to close existing budget deficits and return a balanced budget by the year ending June 30, 2021.”

…The government needs to move beyond responsible housekeeping and ongoing restraint. It needs to be ambitious and articulate the values that define the Turnbull government. That will be neither easy nor risk-free. But that’s the entire point. The strategy of mere survival or fiscal incrementalism has reached its limits. If this is all Turnbull and Morrison represent, they are likely to fade away this term in a long journey of credit downgrades, declining economic confidence and public disappointment.

UBS economist Scott Haslem says while the government has held “the status quo until the budget, there remains no room for slippage”. Industry Super Australia chief economist Stephen Anthony says: “This is kicking the can down the road for another six months. We have seen this before. It represents another lost opportunity. We are left with the impression of fiscal adjustment rather than fiscal reality. We are expected to achieve the surplus but with a weaker economy. We are not actually tackling the reform task. The question is why?

“Everybody senses the government should do more and the ratings agencies want us to tackle the task. The people are aware of the problem — they sense the structural foundations of the economy are tenuous. We have had an incomes slowdown and this is now the lived experience of people.”

The crisis in Australia’s political and governing system is set to deepen. Economic growth is at risk. The intractable nature of the budget problem remains. The AAA credit rating is in jeopardy.

Quite right.