From Bank of Tokyo Mitsubishi:

The Australian dollar has been the best performing currency in the Asian trading session following last night RBA policy meeting. The RBA left their policy rate unchanged as expected and more importantly left the final paragraph of their accompanying statement unchanged as well maintaining a neutral bias. The statement acknowledged that China’s economy has steadied, employment growth has slowed, and house prices were described as having risen briskly in some markets. The RBA signalled that their outlook for the economy was largely unchanged still expecting it to grow at close to its potential rate over the next year before gradually strengthening. Inflation is expected to pick up gradually over the next two years from the current “quite low” rate.

The November statement released on Friday will reveal the latest RBA forecasts. With the RBA signalling that it is unlikely to lower rates further in the near-term without a negative surprise, the Aussie should continue to trade on a firm footing heading into year-end potentially testing this year’s peak for the AUD/USD rate at the 0.7835-level.

The release overnight of the latest PMI surveys from China will help to support the Aussie as well providing a further positive signal that growth momentum is improving. The manufacturing and non-manufacturing PMI surveys both increased to 51.2 and 54.0 respectively in October. It was the highest manufacturing PMI reading since July 2014. The improving growth momentum has coincided with renewed upward momentum in the price of iron ore in the second half of this year.

The Aussie is unquestionably (and understandably) strong right now, but so are other commodity currencies:

The chart still has a bullish set up too with an ascending triangle pattern:

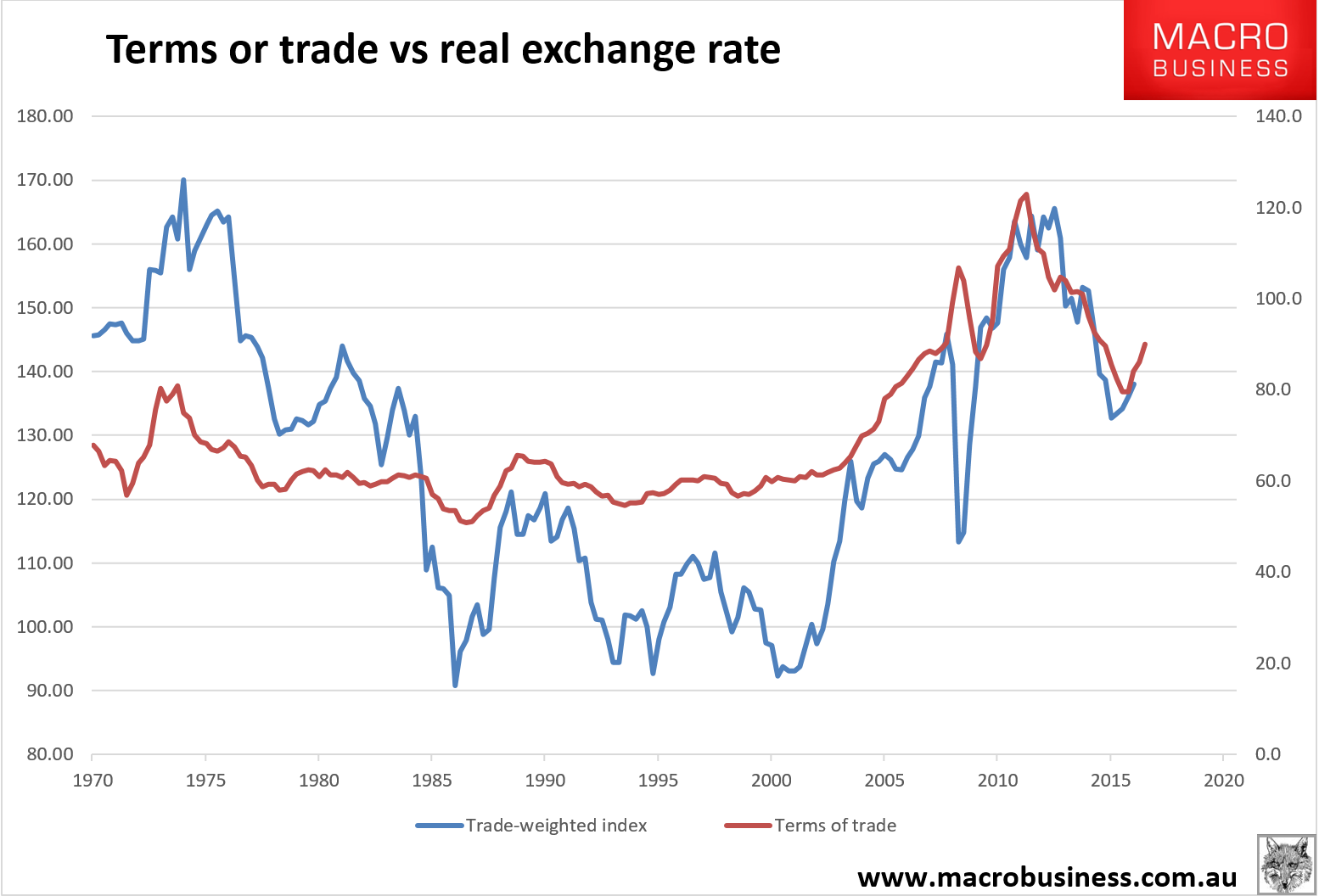

The drivers are not hard to find. The first is the now pretty impressive bounce in the terms of trade:

The second is an RBA that is on hold for now as the economy runs OK.

Still, I am a little less concerned than I was a few weeks ago that we might see a short term spike in the currency. Back then I wrote that the following could do it:

- Chinese construction is going to come off but if it takes a quarter or two longer than I expect then iron ore could hold up for another six months;

- the coal boomlet might likewise linger a little longer;

- if we see the building La Nina deliver a good cyclone season then both markets could keep restocking without much pause right through Q1 2017 meaning more not less price pressure;

- the Q4 risk gantlet holding back markets has eased somewhat. If it keeps doing so then it’ll be risk on for emerging markets;

- and, if I’m right about the Fed not hiking in December then the monetary tailwind behind the Aussie is going to be spectacular.

Since then, points one and two have played out but point three has eased off. Point four is suddenly growing in intensity. If we see a Trump presidency the I’d expect a sizeable “risk off” move and the Aussie to fall even though it would probably pause the Fed. If we see a Clinton presidency then the Fed is more likely to hike and the firmness in points one and two makes it more likely too.

It is also now likely that the Italian referendum will vote “no” and trigger another round of zombieuro hand-wringing.

Thus the mix of drivers for the currency is less bullish than it was.

An 80 cents spike is still plausible, though, especially if we saw a Clinton win and no Fed hike. If it happens, I’d take the chance to take out hedges or get offshore. It will not last long given all it will do is shock the economy and trigger more rate cuts, plus the bulk commodity price spikes will retrace soon enough and even the Fed can’t delay forever. Moreover, it would do nothing to alter my longer term view that the Aussie is heading much lower.