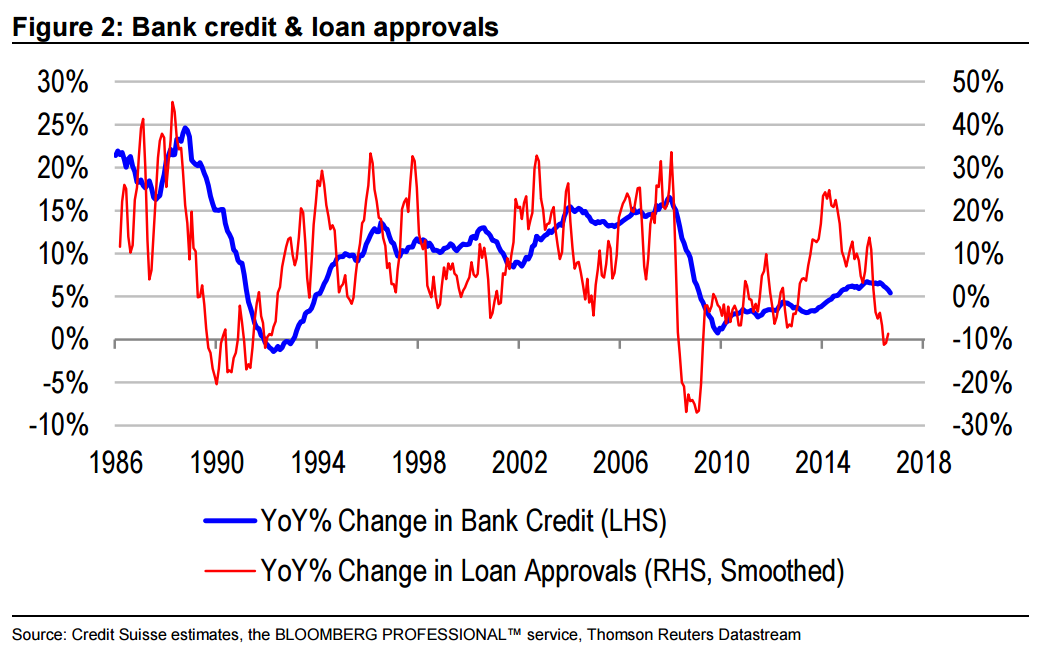

It is well documented that the RBA is closely monitoring core inflation, as well as the health of housing and labour markets. But Governor Lowe has also revealed that the Bank cut rates earlier in the year because it could see credit growth slowing. In this context, a further material slowing in credit growth could also be a trigger for the RBA to ease. Recent credit data do not give the Bank much cause for concern: 1. System credit growth has decelerated to a comfortable 5.4% in the year-toSeptember. 2. Business credit growth has experienced a moderate recovery after the Federal election. 3. Investor housing credit growth appears to be recovering as well. Banks have become a little more willing to lend, having undershot the macro-prudential cap on investor housing credit growth of 10% per annum. Also, non-bank lenders have helped some investors to overcome tighter credit standards in the wake of macroprudential regulation. At face value, recent trends in credit growth support a less dovish stance on policy, and perhaps even normalization of policy settings longer-term. However, we have reason to believe that the worst of the slowdown in credit growth could still be ahead of us, and that the RBA will do well to maintain credit growth at current rates over the next year. In the first place, we note that new loan approvals are shrinking. Historically, growth in new loan approvals (flows) has been a useful leading indicator of growth in credit (the stock). As the back book of loans rolls off (e.g., through repayment or refinancing), the marginal borrower has a larger influence on the direction of the stock of loans outstanding. Over the past year, loan approvals have fallen by almost 10%, consistent with much slower rates of credit growth than we are seeing at present. Previous occasions when loan approvals fell this sharply include the European financial crisis, the global financial crisis, and the early 1990s recession.

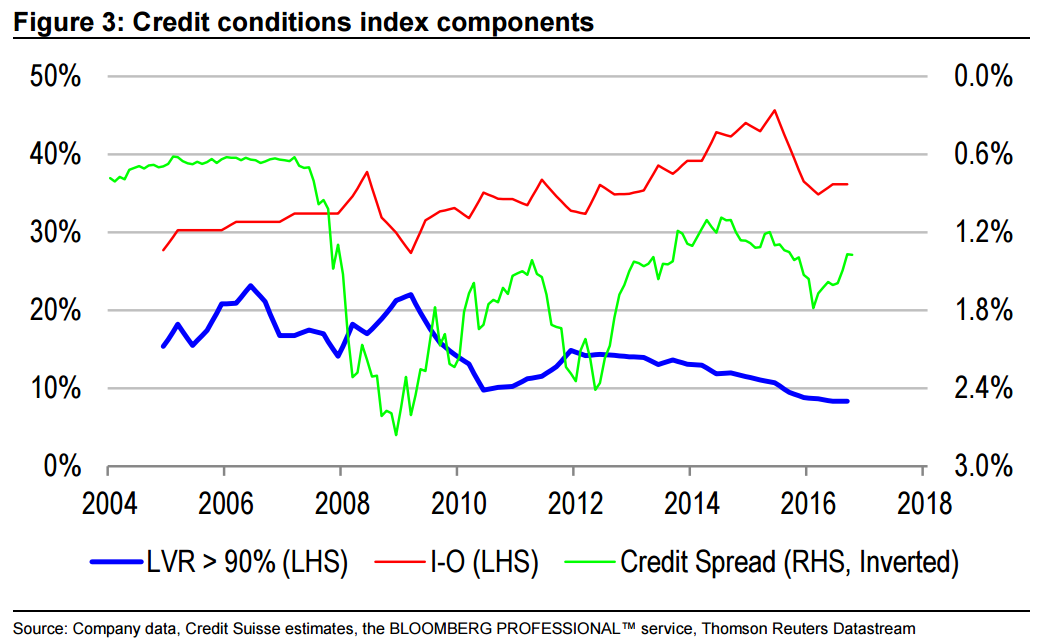

That said, loan approvals are volatile, and at best a noisy leading indicator of credit growth. Therefore, we have constructed a more reliable leading indicator using available data on mortgage lending standards and corporate credit availability. Our proprietary credit conditions index is an equally-weighted (geometric) average of: 1. Banks’ willingness to lend to high loan-to-value ratio (LVR) borrowers. From 2008 onwards, APRA provides data on the breakdown of new mortgage approvals by LVR buckets. We use the share of new loans extended to borrowers with LVRs greater than 90%. Prior to 2008, we use proxy LVR data from AFG. 2. Banks’ willingness to lend on interest-only terms. Since the early 2000s, APRA and the RBA publish data on the share of new mortgages extended to borrowers on interest-only terms. 3. Inverted credit spreads. We use an average of three-year AA- and BBB-rated corporate spreads to government bonds to proxy the tightness of credit to businesses. Global historical experience suggests that banks’ willingness to make commercial loans is extremely negatively correlated with credit spreads. We presume that the same relationship works out in Australia too, allowing us to use credit spreads as an inverse proxy for banks willingness to lend to corporates.

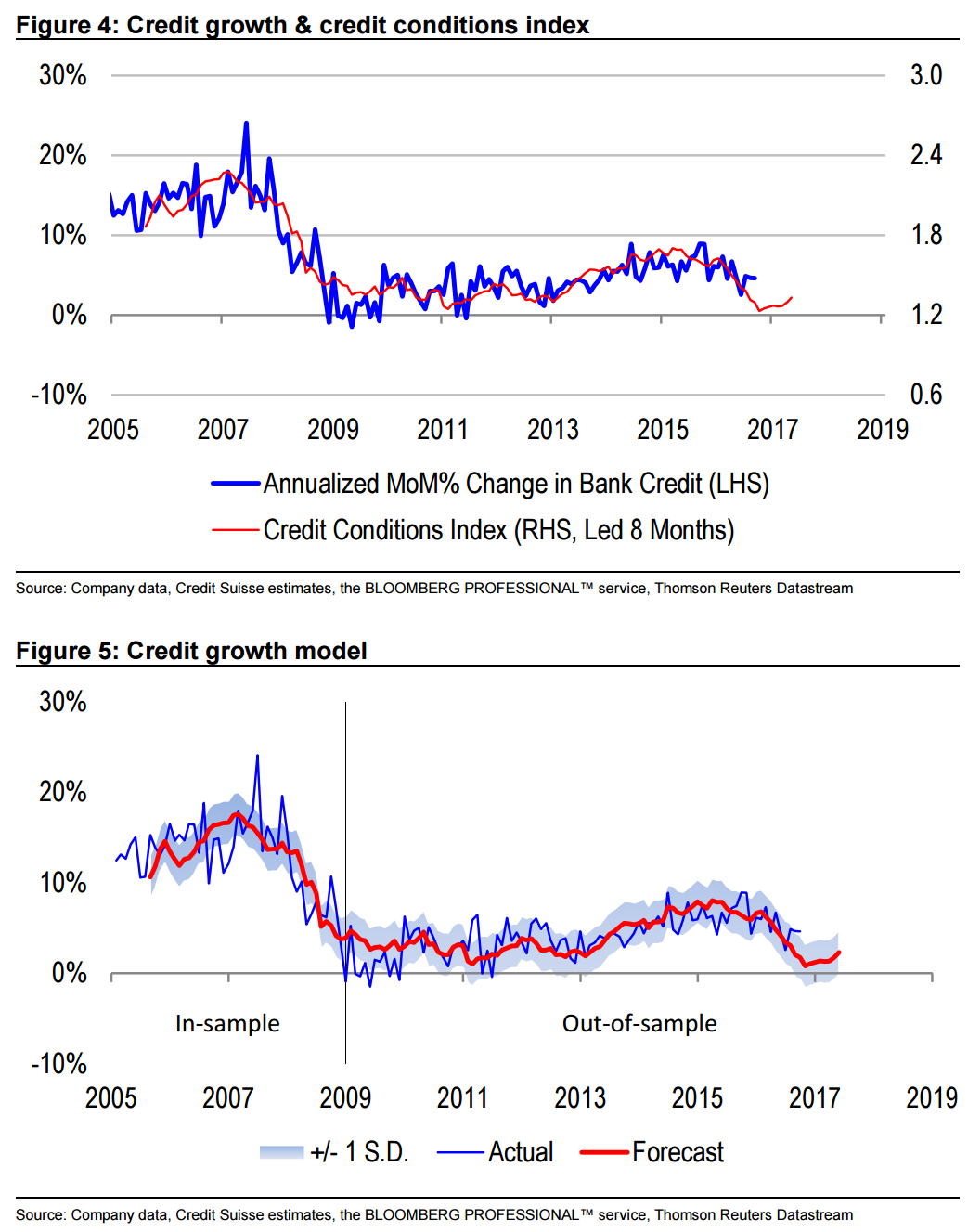

Effectively, mortgage variables have two-thirds weighting in our index, while business credit variables only have a one-third weight. In our view, this weighting regime is consistent with the composition of banks’ loan books. Historically, our credit conditions index is highly correlated with monthly bank credit growth, up to eight months forward. Indeed, the correlation is so tight, that we can build a robust regression model of credit growth using only our credit conditions index. The model points to credit growth stalling towards the back end of 2016, before recovering modestly in early 2017. But even when credit growth recovers, it is unlikely to return to its current pace.

The reason why credit growth is likely to slow is because banks’ willingness to lend on interest-only terms has declined significantly in the wake of macro-prudential regulation. Also, maximum LVRs on mortgages have continued to drift lower. These changes have been in the system for some time – but yet the data suggests that they take a very long time to completely flow through to actual credit growth. More recently, we have seen credit spreads narrow, signalling slightly better corporate credit availability. But offsetting this, banks have also announced some further tightening of mortgage lending standards to particular regions and customer segments. Accounting for forecasting errors, we note that current monthly credit growth of 0.4% (4.6% annualized) is currently more than one standard deviation above the mean forecast of 0.1-0.2% (1-2% annualized). Historically, whenever we have seen this sort of overshooting, we have also tended to see undershooting shortly afterwards, reflecting the 0.6 1.2 1.8 2.4 3.0 -10% 0% 10% 20% 30% 2005 2007 2009 2011 2013 2015 2017 2019 Annualized MoM% Change in Bank Credit (LHS) Credit Conditions Index (RHS, Led 8 Months) -10% 0% 10% 20% 30% 2005 2007 2009 2011 2013 2015 2017 2019 +/- 1 S.D. Actual Forecast In-sample Out-of-sample 31 October 2016 Australian Economics 5 strong mean reversion properties of our model. In lieu of this, the RBA will be doing very well over the next few quarters to maintain current rates of credit growth. Policy implications When the RBA cut rates earlier in the year, it did so ahead of an actual slowdown in credit growth, because it could sense downside risk from macro-prudential regulation. A slowdown has indeed materialized – but it appears with hindsight to have been quite orderly. Recent credit growth, and its composition are probably quite acceptable to the Bank. As such, there is no catalyst yet in the credit data to support an RBA rate cut. However longer-term, there are still downside risks to credit growth, as loan approvals are still falling, and the delayed effects of past credit tightening are yet to fully manifest. And should credit growth slow as we expect, the Bank would need to respond to the disinflationary impulse by lowering rates.

Certainly consistent with the CoreLogic leading index of mortgage creation…

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.