We have updated our economic, currency and interest rate outlook for Australia following the US election as part of our November Global Macro Outlook. Outlook

GDP outlook: We have downgraded our Australia GDP outlook in concert with our US economists; downgrade to the US growth trajectory. The key impact channel domestically is a further delay to the upswing in business investment we had anticipated in FY18, stemming from the shock to confidence – globally and domestically – and anticipated ripple effects of uncertainty given the number of significant elections through 2017 (e.g. Europe).

We are reducing our Australian GDP growth forecasts to 2.1% in 2017 (previously 2.3%), 2.6% in 2018 (3.2% prior) and 2.7% in 2019 (2.8% prior). Much will depend on the evolution of markets’ response to the surprise outcome, and the extent to which questions of “what now” and “who’s next” dampen confidence and induce a risk premium into decision-making by businesses and consumers. Risks remain tilted to the downside, particularly on the inflation front, with the avoidance of downside risks dependent on the response of the A$, and of policy makers (monetary, but especially fiscally).

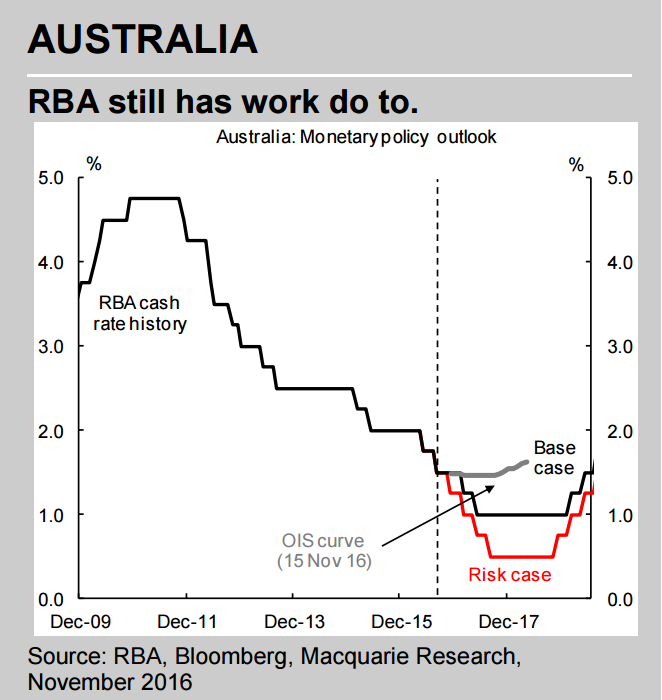

Rates: The unexpected election outcome has strengthened the case for further RBA easing in 1H17. Market pricing had moved away from the prospect of additional RBA rate cuts post election. We reiterate our base case for 25bp rate cuts in February and May 2017, taking the RBA cash rate down to 1.00%. Our US economist has retained a December Fed Funds hike on the basis that market volatility subsides in the near term. Should this fail to emerge, Fed timing could be pushed out. That delay would be expected to result in further discomfort for the RBA from a higher A$.

Bonds & FX: Along with the growth outlook we have also adjusted our exchange rate and bond forecasts. The upgrade to our US bond trajectory has seen us lift our Australian bond floor to 2.30%, with Australian yields dragged higher by rising US yields through 2018. Our expectation for domestic easing over coming months weights on yields in the short run.

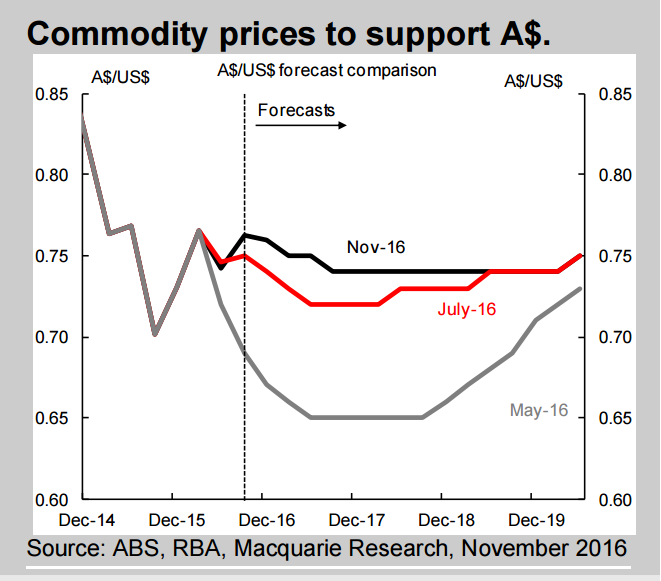

Confidence in the outlook for China, and commodity prices are likely to support the A$ despite additional RBA easing. Our global team’s currency forecasts imply limited upside for the US dollar. As such, currency containment, in order to avoid a tightening of financial conditions, remains a key focus for the RBA. Unwelcome A$ strength is self-limiting, given the RBA’s already weak inflation backdrop.

Outcomes in the labour market, and inflation, are the key domestic variables for the policy trajectory over the year ahead. With both sluggish, the RBA will be keen to avoid unwanted currency strength. An A$ persisting below the US$0.74 mark could be enough to keep the RBA sidelined, depending on the evolution of commodity prices and internal conditions. We would add conviction to our RBA call should the A$ push up to, or beyond, US$0.78.

The main differences between the MB and Mac Bank outlooks is that we see Australian terms of trade falling right back to their lows by Q3 next year and the USD as higher, in part because of the European elections. Thus we see the Aussie at risk of big falls through mid next year.

We don’t bother with a rate cut forecast given it’s all too variable but we certainly agree that more are coming, even if the dollar falls materially. By this time next year Australia will be struggling to grow at all as the dwelling boom cycles down, immigration comes under intense political pressure, the mining capex cliff continues and the car industry shutters.

Backbone Phil may not want to cut but what else do central banks do with a weak economy?

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.