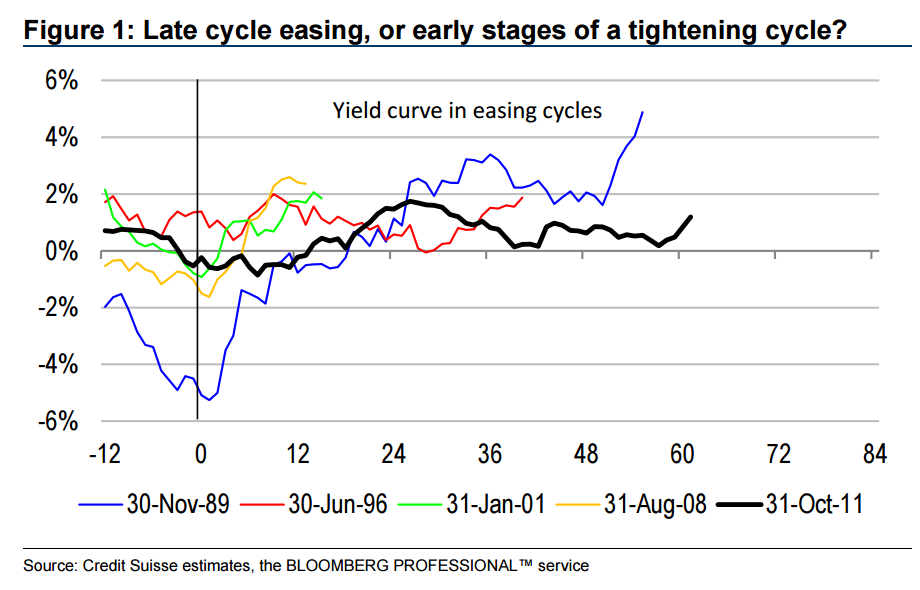

If historical cycles are anything to go by, the recent curve steepening may mean that RBA tightening is just around the corner. But we do not think so. We believe that we are seeing the bond market tantrum of 2012–13 all over again. On that occasion, US term risk premia rose sharply from extremely negative and unsustainable levels. For a little while, Australian bonds and bond proxies underperformed. The RBA left rates unchanged for a very long time, despite various suggestions at the time that it should tighten. But eventually, the Bank resumed rate cuts. Bonds, and bond proxies outperformed, and even set new historical highs in price. To date, this cycle looks very similar to 2012–13. US term risk premia have normalised from extremely negative, and unsustainable levels. Australian bonds and bond proxies have underperformed in this process. The market is pricing in an extended RBA pause, despite some suggestions that inflation may be bottoming, and that the next move in rates should be up. Apparent differences between now and then include:

1. Commodity prices on an upward trend, rather than volatile around a flat, or weakening trend.

2. Central banks globally realising the perverse negative effects of ultra-low rates.

3. A less exuberant domestic housing cycle.

We do not think that these differences will ultimately change the downward trajectory of the RBA cash rate. After all:

1. Two-way volatility in commodity prices could return if the USD strengthens materially. And in any case, even with the recent bounce in commodity prices, mining capex is unlikely to recover.

2. The RBA has room to cut rates further, in contrast with its peers who have hit the zero bound. To be sure, the bank does not want to venture too far down the path trodden by its peers – but this is not to say that rate cuts are currently ineffective. The Bank is also adamant that rate cuts work by boosting household cash flow.

3. As for housing, the less exuberant cycle means that the contribution of the sector to domestic demand (both directly and indirectly) will be smaller than it was before.

Macro-prudential pressures are unlikely to unwind either. If anything, banks could tighten their lending standards even further, this late in the cycle. If for various reasons, we are not on the cusp of a tightening cycle, then we are certainly on a very long, and unusual easing cycle.

That’s spot on in my view. But, will bonds sell further first? The key to that will be commodity prices for both the globe and Australia but for different reasons. If OPEC can underpin oil then bonds are likely to fall further as inflation expectations firm up. For Australia, bulk commodities will fall all the way back to the lows (and more for iron ore) and that will guarantee more rate cuts. I expect both outcomes.

However, recall that both will very likely be fighting a rampaging USD bull market and commodities can’t get very far under those circumstances so oil is not going to the moon and neither are bond yields.

Therefore, the bond play in Australia remains buy the dips at the short end (when you’re comfortable that there is enough value) and avoid the long.

Advertisement

CS also examines the equities fallout:

■ Eruption: Australian 10-year bond yields have risen 80 basis points since August. What started as a smoldering flow out of the asset class has tuned into a small eruption since the US election. While there may be a near-term retracement of bond yields, given the sharp rise, we expect the mediumterm trend to be higher from here.

■ Bonds and Aussie equities: The increase in real bond yields has so far been a headwind for Aussie equities. But history suggests the drag should begin to diminish soon. Also, supporting higher stock indices is the coming end of the profit recession. We forecast Aussie equities to grind higher.

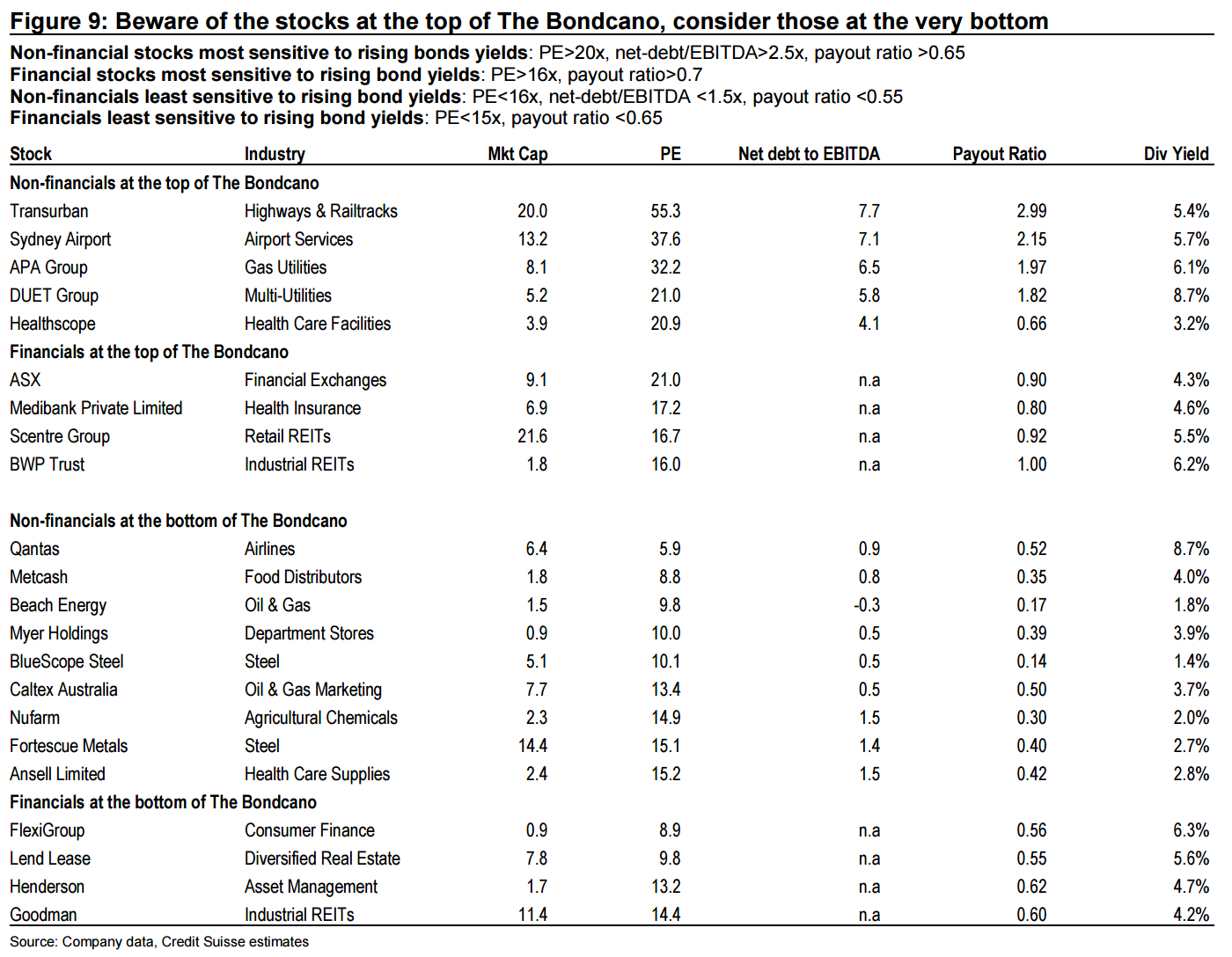

■ Beware of The Bondcano: We continue to be wary of stocks at the very top of The Bondcano. They include companies with high PEs, high financial leverage and high payout ratios. They are most vulnerable to higher bond yields and include Sydney Airport, APA, Healthscope, ASX and BWP Trust. Stocks at the very bottom include Qantas, Myer, Nufarm, Fortescue and Lend Lease. We add ASX to the short portfolio.

I see no upside in buying local equities yet but if someone put a gun top my head and made me then I’d still be buying dollar-exposed industrials so the only two firms on that list that makes sense to me are Qantas and Ansell.

As US rates and its dollar rise, and Australia’s bulks fall, the Aussie dollar will crater.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.