From the FT:

The late Thomas Bernhard, a mordant Austrian author, once likened the mentality of his compatriots to punch cake, a rum-soaked national dessert. On the outside it is red, like the left; inside it is brown, like Nazism; and it is always a bit drunk.

Austria’s December 4 presidential election re-run pits Alexander Van der Bellen, a Greens-backed independent, against Norbert Hofer, the far-right Freedom party’s candidate. Thankfully, the campaign is not some murderous 1930s-style bloodbath between red and brown.

Nonetheless, as Bernhard would have been the first to recognise, much is at stake for Austria, its central European neighbours, the EU and western democracies in general. Mr Hofer has a narrow lead in opinion polls. For the first time since the second world war, voters in a European democracy are poised to elect a far-right head of state.

If Austria elects Mr Hofer, what is to stop France electing Marine Le Pen as president next May? What is to stop the advance of anti-establishment forces in Italy and the Netherlands? The politics of Hungary, Poland and Slovakia are already polluted with illiberalism, Islamophobia and anti-immigrant nationalism. Against the backdrop of Britain’s vote to leave the EU, and doubts over America’s commitment to European security after Donald Trump’s victory, it is tempting to paint the outlook for Europe in grim colours.

…If disillusion with an out-of-touch establishment explains part of Mr Hofer’s appeal, so do his artful efforts to portray himself as a “centre-right politician with a big social conscience”. To the extent that Austrians buy into his reassuring slogans, the chances increase that the Freedom party will win the next parliamentary elections, due by 2018, and become the senior partner in a new coalition government. This, too, would be a first for the far right in Europe.

Yet there are excellent reasons to question whether the telegenic Mr Hofer’s soft-spoken serenity is the true face of the Freedom party. In a fiery speech last month, Heinz-Christian Strache, the party’s leader, labelled German chancellor Angela Merkel not only the most powerful but “unfortunately also the most dangerous woman in Europe” on account of her “criminal” refugee policies.

For good measure, Mr Strache denounced the “uncontrolled influx of migrants, alien to our culture, who seep into our social welfare system … making civil war in the medium term not unlikely”. As for Mr Hofer, he has by his own account sometimes carried a semi-automatic Glock pistol in public.

Nowadays the party plays down the anti-Semitism for which it was notorious under Jörg Haider, its former leader, who died in 2008. However, the party is saturated with pan-Germanic cultural nostalgia, a cause long dear to the far right. Its European Parliament website states it is “a social and patriotic movement and an ideological representative of the political camp of German national and national-liberal voters”.

That is going to shock the world but largely in terms of spirit not markets.

On the same day is the Italian referendum:

Silvio Berlusconi thrust himself back into the frontline of Italian politics with an emphatic rejection of Matteo Renzi’s constitutional reforms, trying to position himself as a key power broker if Italians reject the prime minister’s plans and his government collapses.

Polls suggest Italians will reject the reforms — a mix of measures to address legislative and administrative gridlock — in a referendum in December, potentially triggering Mr Renzi’s resignation and ushering in a period of political turmoil.

The public intervention by the media tycoon and three-time former prime minister will add to Mr Renzi’s difficulty in winning the December 4 vote. The outcome is being closely watched across Europe because of the possibility that it could dent investor confidence in the eurozone’s third-largest economy.

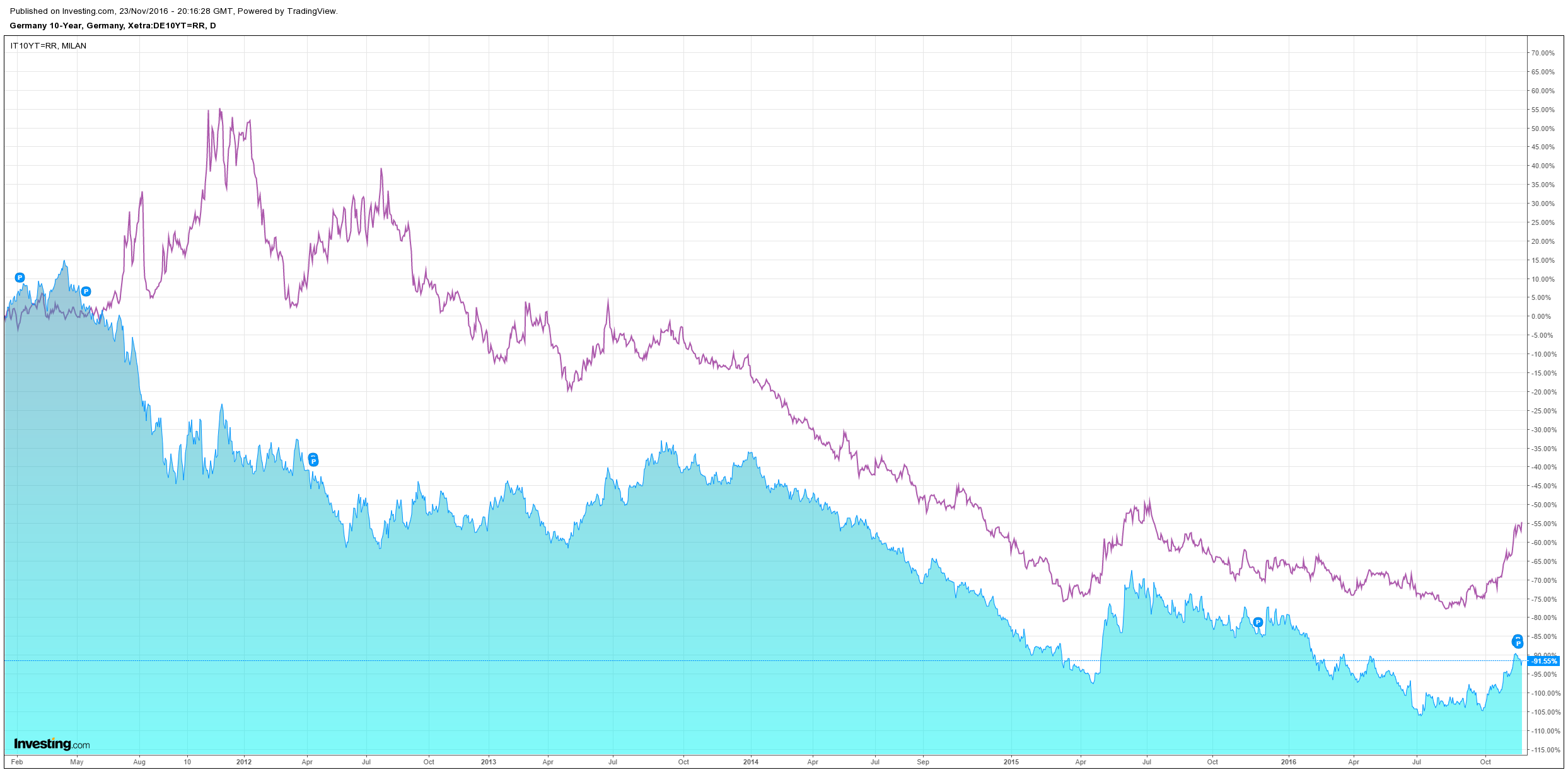

Italian bond spreads continue to widen over German:

As usual, trying to figure out Italian politics is like sticking your head in a blender:

Under the current electoral system it is unlikely Five Star Movimiento (FSM) would wnn an outright majority, however, to complicate matters, the electoral rules changed in July 2016.

The changes are embodied in what is called the Italicum, and were brought in to help increase the power of the party with the largest share of the vote.

Under the new rules, if a party wins over 40% of the share of the vote, it is awarded 340 extra seats, majorly increasing its parliamentary majority.

On this basis, it is possible that a scenario could evolve in which the referendum could lead, via a sequence of steps, to Italy exiting the Euro.

For example, if the referendum returns a “No” vote (which it probably will do) and Renzi resigns (which he probably will do) and no replacement can be agreed on (odds not known), and there is a snap election in two months’ time, Five Star could win 40% of the vote (which they may do) and then according to the Italicum get the bonus seats for being the largest party.

This would result in a Five Star government, which has said in its manifesto it would call for a referendum on membership of the EU.

Given the majority of Italians are against remaining in the EU, such a referendum might very well result in an ‘Italexit’.

“A French or Italian exit from the euro would bring about the biggest default in history.

“Foreign holders of Italian or French euro-denominated debt would be paid in the equivalents of lira or French francs. Both would devalue.

“Since banks do not have to hold capital against their holdings of government bonds, the losses would force many continental banks into immediate bankruptcy,” writes Munchau.

If the effect of the electoral changes embodied in the Italicum were a certainty then the above scenario would present a major threat, however, many analysts are more sanguine about the risks of the Italian referendum because the Italicum has had its legitimacy challenged in the Italian courts, and is currently under review.

“Early this year a Court in Messina sent the Italicum law for review to the Italian Constitutional Court under the suspicion it will breach the Italian Constitution,” says Henriksson.

The outcome of the case will not be known until after the referendum, but if the Italicum is okayed by the Constitutional Court that will also potentially see scope for a Five Star majority.

Indeed it is not entirely clear the extent of the Italicum’s current legitimcay and whether it could hold sway in a snap election or not.

The greatest risk to the Euro is from Italy leaving the EU but this would require FSM winning a clear majority in a general election, a majority they could only gain with the premium seat add-on enshrined in the Italicum.

“If your obsession is fear of populism (in Italy in the most likely form of the Five Star Movement), then the huge number of bonus seats assigned for the biggest party under the Italicum should be your number one concern, and you should, therefore, hope for the outcome that maximises the probability of the Italicum being significantly changed to sharply reduce, if not eliminate the premium seats before the next election,” says Erik Nielsen, Global Chief Economist at Unicredit.

In short, Nielsen sees the referendum result as majorly influencing the outcome of the Italicum.

A win for the “Yes” camp would paradoxically lead to a higher chance of the Italicum being ratified with its premium seat clause intact, whilst a win for the

“No” camp and the resignation of Renzi would probably see the Italicum heavily watered down.

If the “No” vote succeeds, and the threat of early elections looms then there is a strong possibility the powers at B will want the Italicum changed before the election to ensure FSM do not sweep to power.

“A no-vote scenario …will immediately involve the president and a discussion with the key political leaders, all of whom will want the Italicum changed,” says Nielsen.

He sees this as a lesser risk than a win for the “Yes” vote which is ostensibly the less risky outcome.

It seems the probability is that MS5 will have to wait to gain power so the Italian shock should be limited as well for the time being, though a further widening of Italian spreads seems certain.

The big one remains France. From the Express:

In an interview with RT, the Professor of Political Economy at St. Mary’s College claimed the French people want a leader who is going to bring change.

Professor Rasmus said: “They don’t really care how extreme some of their positions may be – we saw that with Trump.

“Nobody is going to vote for the Socialists. It’s really going to be Le Pen’s election to lose, I think.”

Speaking about the political situation in France, Rasmus said: “What you’ve got is a lot of working class and small business folks who are just fed up with the policies of the last decade, which have emphasised trade and tax benefits for the rich, the concentration of income and the loss of jobs with which people can sustain themselves.

He added: “I think Le Pen is in a very strong position here because people are just rejecting the old parties associated with the old policies.

Eurosceptic Le Pen has vowed to launch a referendum on France’s continued EU membership if she wins the election next year and claimed she is “fighting in the name of the people”.

Mr Rasmus likened Le Pen’s campaign to the success of Trump as well as the influence of Ukip in forcing a referendum onto the agenda and managing to convince Britons to vote to leave the EU.

He said: “When someone comes along like Le Pen, or Trump or the UKIP Party in Britain and says, ‘Look, we’re going to change’, here is someone that will give us something different.”

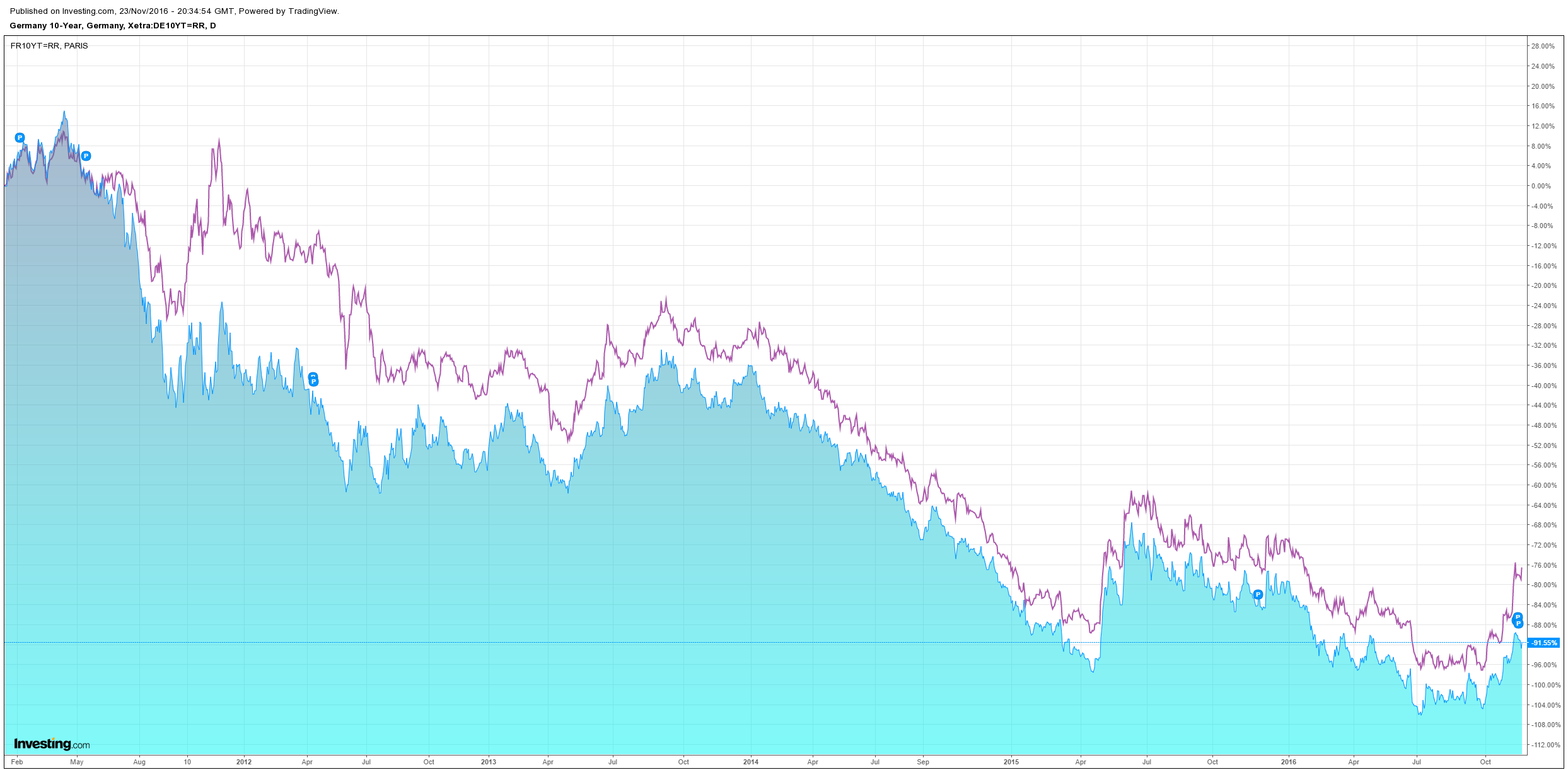

French spreads are also widening:

The major investment implication for now remains upwards pressure on the US dollar as the zombieuro lurches towards disintegration. If France’s National Front comes to power then you need to be positioned for the economic shock of a lifetime.