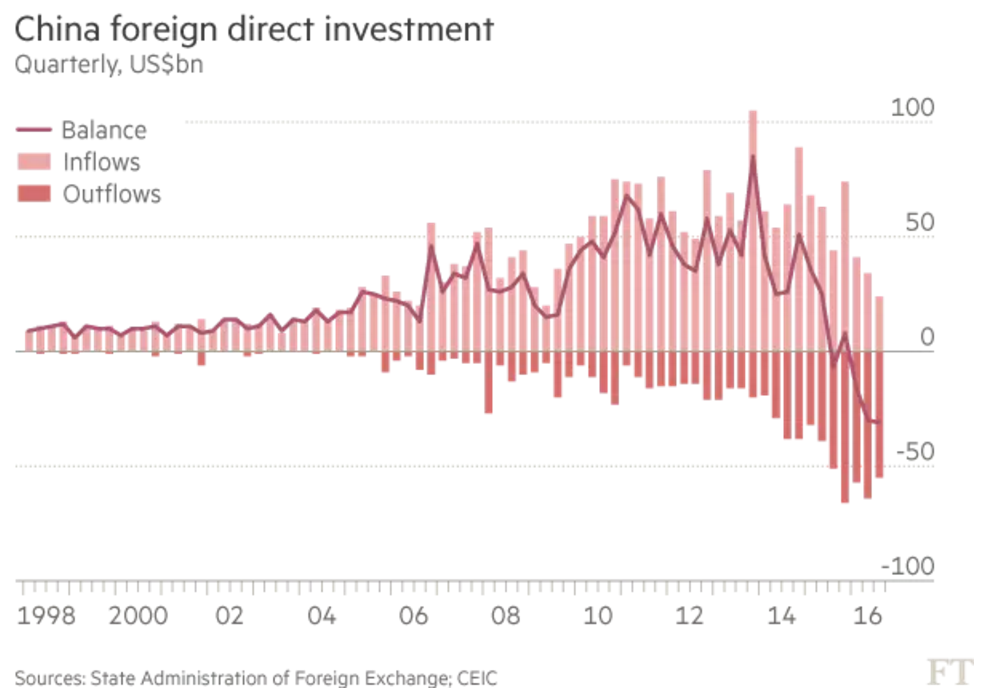

Beijing is embarking on a massive policy shift designed to stem capital flight by curbing outbound investment, sources say.

Tighter control of overseas investment is likely to put an end to a trophy-asset shopping spree by well-connected companies such as Anbang Insurance and Dalian Wanda, with Beijing ready to cut the supply of foreign exchange for such deals.

Shanghai’s municipal foreign exchange authority had told bank managers in the city that all overseas payments under the capital account of more than US$5 million would have to be submitted to Beijing for special clearance before proceeding, according to the sources.

They added that while the move did not necessarily mean all such deals would be vetoed, the regulatory procedures that would have to be navigated before completing them would take much longer.

A separate document seen by the South China Morning Post said to be the minutes of a central bank meeting on cross-border capital controls, said that from now until September of next year, Beijing would ban: deals involving investment of more than US$10 billion; mergers and acquisitions valued at more than US$1 billion outside a Chinese investor’s core business; and foreign real estate deals by state-owned enterprises involving more than US$1 billion.

“Under its World Trade Organisation commitments, China is supposed to have a more transparent legal framework,” said one frustrated Chinese lawyer, adding that the situation was “harmful”.

“The reversal of measures to liberalise capital outflows reflects China’s zig-zag approach to reforms,” said Eswar Prasad, a China finance expert at Cornell University. “This step signals the government’s conventional preference for stability and control rather than economic liberalisation and resulting volatility.”

“This is a big move,” said Wang Jun, an economist at China’s Center for International Economic Exchange. “The government has stepped up capital controls to prevent further depreciation of the renminbi.

“The trend of US dollar appreciation and renminbi depreciation is obvious,” Mr Wang added. “They are worried about capital flight.”

Advertisement

What I think of immediately is this:

The A-REITS bubble is already under pressure from rising global bond rates. Now you can add capital values as the marginal buyer disappears.

Chinese tightening is also accelerating, via Zero Hedge:

Advertisement

Quoted by Bloomberg, Wu Sijie, bond trader at China Merchants Bank said “tightening interbank liquidity and the expectation of even higher short-term borrowing costs are driving up swap costs and affecting sentiment on the cash bond market.”

Meanwhile, signalling no change at all in its posture, overnight the PBOC drained funds in open-market operations for the fourth consecutive day, bringing the total withdrawal to 130 billion yuan.

Why is all of the above relevant? Because while so far the global capital markets have been immune to the substantial tightening in financial conditions resulting from the sharp rise in the US Dollar and US interest rates, a similar tightening in China – which is now clearly taking place – will be far more difficult for global risk assets to ignore.

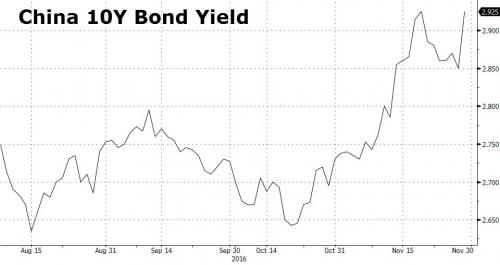

As we reported yesterday, “since Oct 21, yield of 10Y Chinese Government Bond (CGB) has risen by 20bps, from 2.65% to 2.85%, partly in response to the strong global rates and USD move since the US election.” Bank of America expects Chinese yields to rise further to 3.40% by the end of 2017. Furthermore, with credit spreads near all-time lows, the bank warns that there is a risk that the move can widen sharply in the near future.

Judging by the biggest jump in yields in over a year taking place the very next day, this appears to be playing out as expected.

As Cui wrote, the local equity market reacted progressively less favorably to rising rates the last four times as investors turned ever less optimistic about growth outlook. The bank believes that “the rising rates this time may put pressure on equities in general as it would occur in an environment of lackluster growth.”

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.