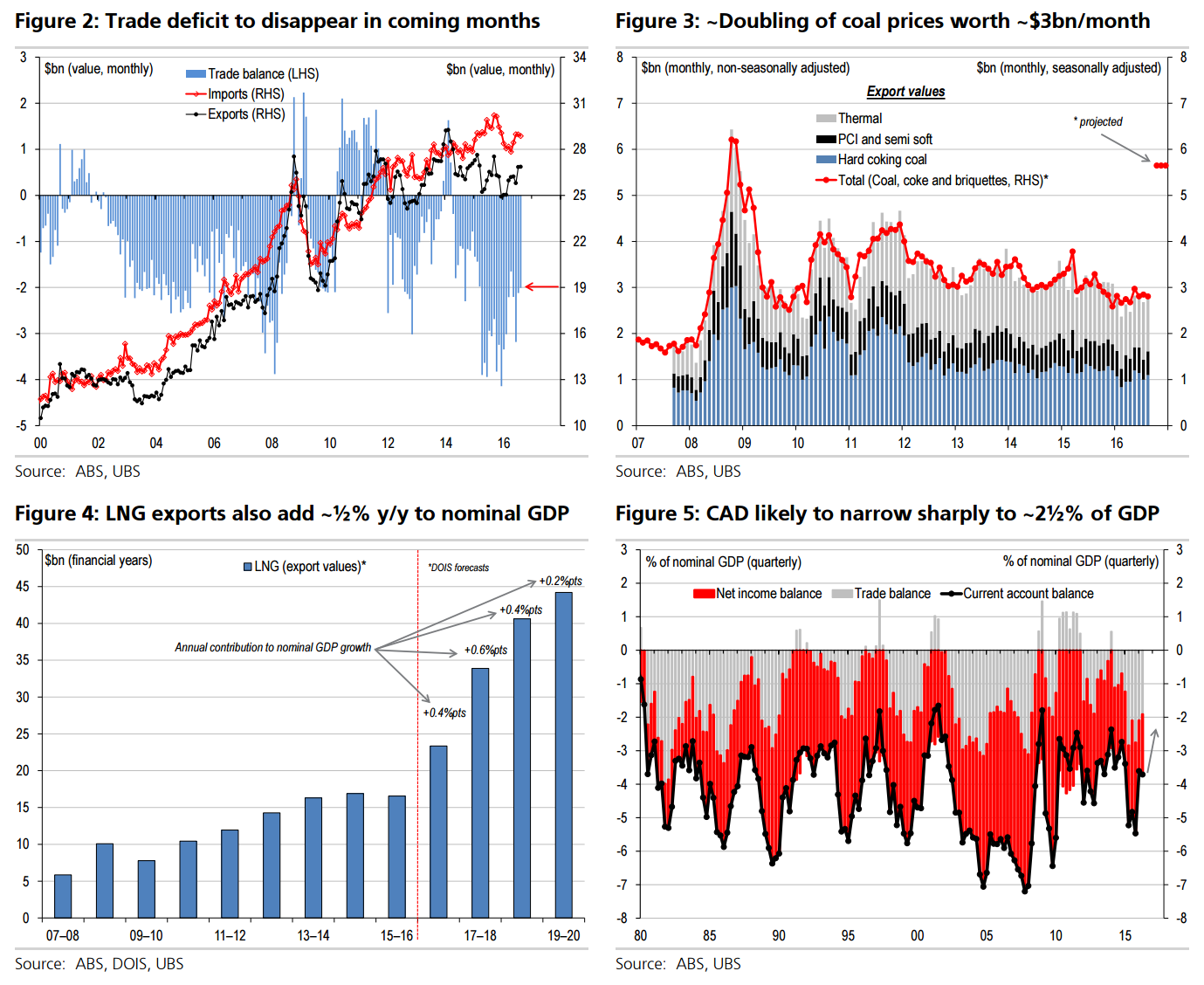

Chinese supply cuts saw coal prices unexpectedly surge recently. Initial contracts for hard coking coal prices spiked by 116% q/q in Q4-16 to ~US$200, with more recent spot prices another ~20% higher at ~US$240 (Figure 1). Thermal spot and semi-soft contract prices also rebounded ~50% in the last quarter. Together, coal prices – weighted by Australia’s export share of each type of coal – have more than doubled (with only a very small offset from the recent AUD/USD appreciation). The impact of higher coal prices is largely yet to be evident in the data.

While the monthly trade deficit already halved this year to $2bn in August (Figure 2), most of the coal price spike was after this. With coal exports ~$2.8bn/month (~10% of total exports), the recent >doubling of prices will lift exports ~$3bn/month (Figure 3). Hence, it seems likely the trade deficit will disappear in coming months, & could even be a surplus. That said, given significant foreign ownership of coal companies, a deteriorating net income deficit (as higher profits flow to foreign owners) will partly offset the trade improvement. However, when combined with strong LNG-driven exports also adding ~½%pt y/y to nominal GDP (Figure 4), the current account deficit (CAD) will still narrow sharply towards 2½% of GDP in 2017, around the smallest trend in decades (Figure 5).

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.