S&P: Straya is Spain with “extreme” foreign debt

The truth today from S&P, via the Australian:

John Chambers, the chairman of the firm’s sovereign ratings committee, suggested the federal government risked losing the AAA rating if it continued to miss its fiscal targets.

“The government will point out that its fiscal position is strong — but it’s not quite as strong as it used to be,” Mr Chambers told The Australian, just days after he heard Scott Morrison emphasise Australia’s economic strength at a gathering in New York.

“And you don’t want to have your fiscal situation adding fuel to the fire on the external side.

“Australia would have one of the weakest external positions of the 130 sovereigns that we rate.”

…“You’ve already hit an extreme measure of (foreign liabilities) so in terms of a trigger (for a downgrade), it would be more on the fiscal side,” he said.

Mr Chambers said the rapid increase in Australian house prices and property investment was similar, though not as pronounced as the surge in unproductive property investment in Spain more than a decade ago, before that nation’s credit troubles.

“For Spain to have patted itself on the back before the crisis is a little bit missing the point,” he said, noting that Spain’s public debt surged from about zero to 80 per cent of economic output in the wake of the global financial crisis.

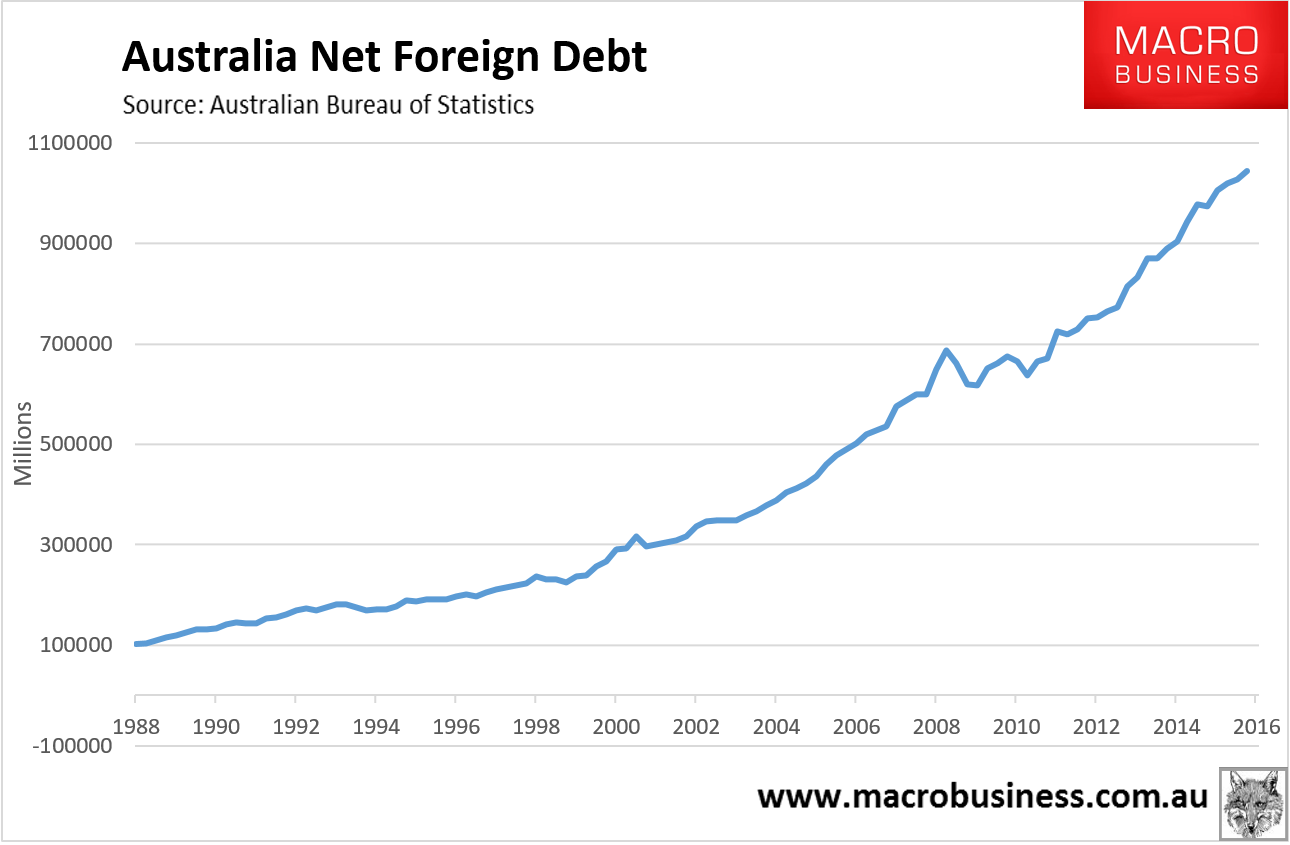

Here is said debt:

S&P should get on with the downgrade. There’s no budget repair coming for the simple reason that if the Budget were to be repaired then net foreign debt would stop growing and the economy grind to halt. Net foreign debt growth is our only source of domestic demand given it funds the shrinking housing boom and the fiscal stimulus that is all we have left.

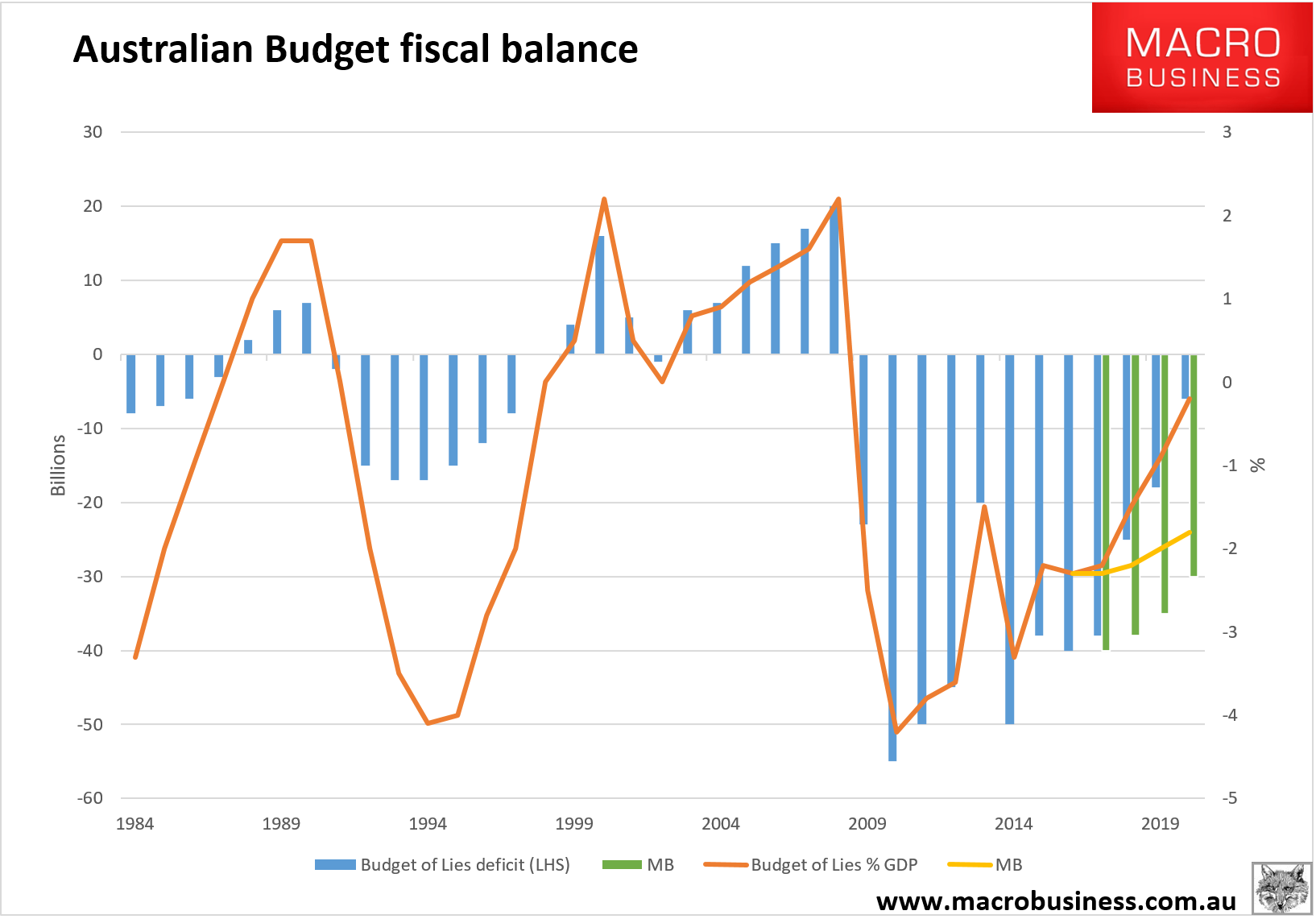

We’ll be able to pretend that there is some budget repair until the terms of trade roll over again in the next quarter or two but from there it is all deficits as far as the eye can see:

The way out is to repair competitiveness and productivity to grow via tradables and and income growth and Scott Morrison sort of knows it, from the AFR:

Treasurer Scott Morrison has emphatically signalled he opposes more interest rate cuts by the Reserve Bank of Australia, arguing monetary policy has “exhausted its effectiveness”.

“Its ability to impact and influence is diminishing,” Mr Morrison told The Australian Financial Review in Washington on the weekend.

In a rare intervention, the Treasurer said instead of RBA rate cuts, the Turnbull government’s policies needed to do the heavy lifting to “boost incomes and lift living standards”.

“What’s more important for our economy is getting on with our fiscal consolidation and bringing forward productivity-enhancing reforms,” Mr Morrison said.

On budget policy, Mr Morrison said there was a recognition about the importance of the composition of fiscal policy, not just the level of government spending.

In other words, indebted governments can consolidate their budgets over the medium term by focusing more on productive spending and investment, and cutting wasteful recurrent expenditure.

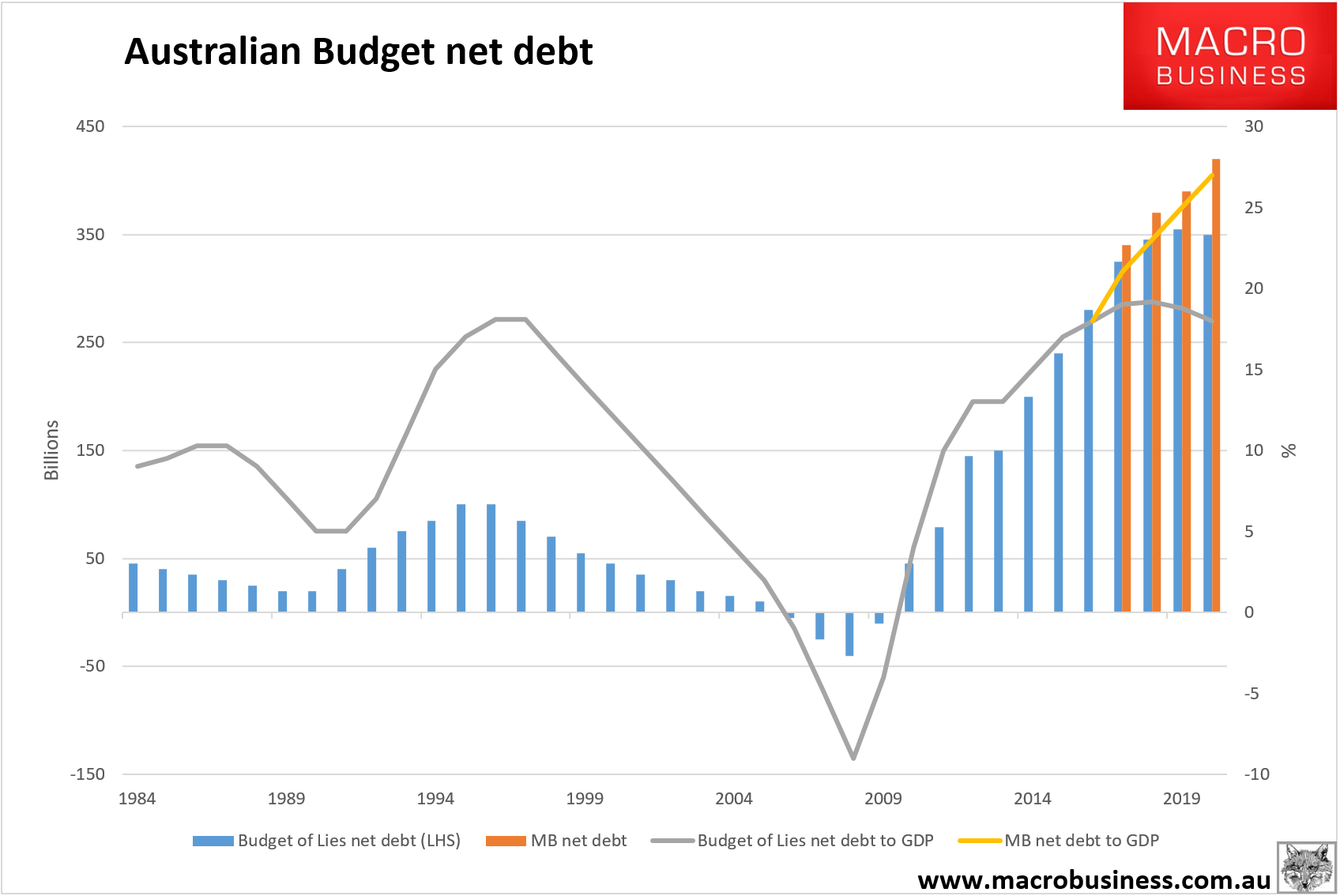

Sigh. The corporate tax cut is not structural reform, it is an income giveaway to foreign shareholders and is thus dead man walking in the parliament. Nor is there much push to lower recurrent expenditure. Do-nothing Malcolm knows what will happen if he cuts the middle class welfare. Net foreign debt will stop growing as households retrench on the income shock:

And Do-nothing will lose his job.

There is no budget repair coming. There is no stopping net foreign debt, either. What is coming is a AAA downgrade and, very likely when the next global shock arrives, some kind of Spanish-style reckoning to the twin deficits to recalibrate the model.