More orgasmic coverage of the commodity boomlet today at the AFR:

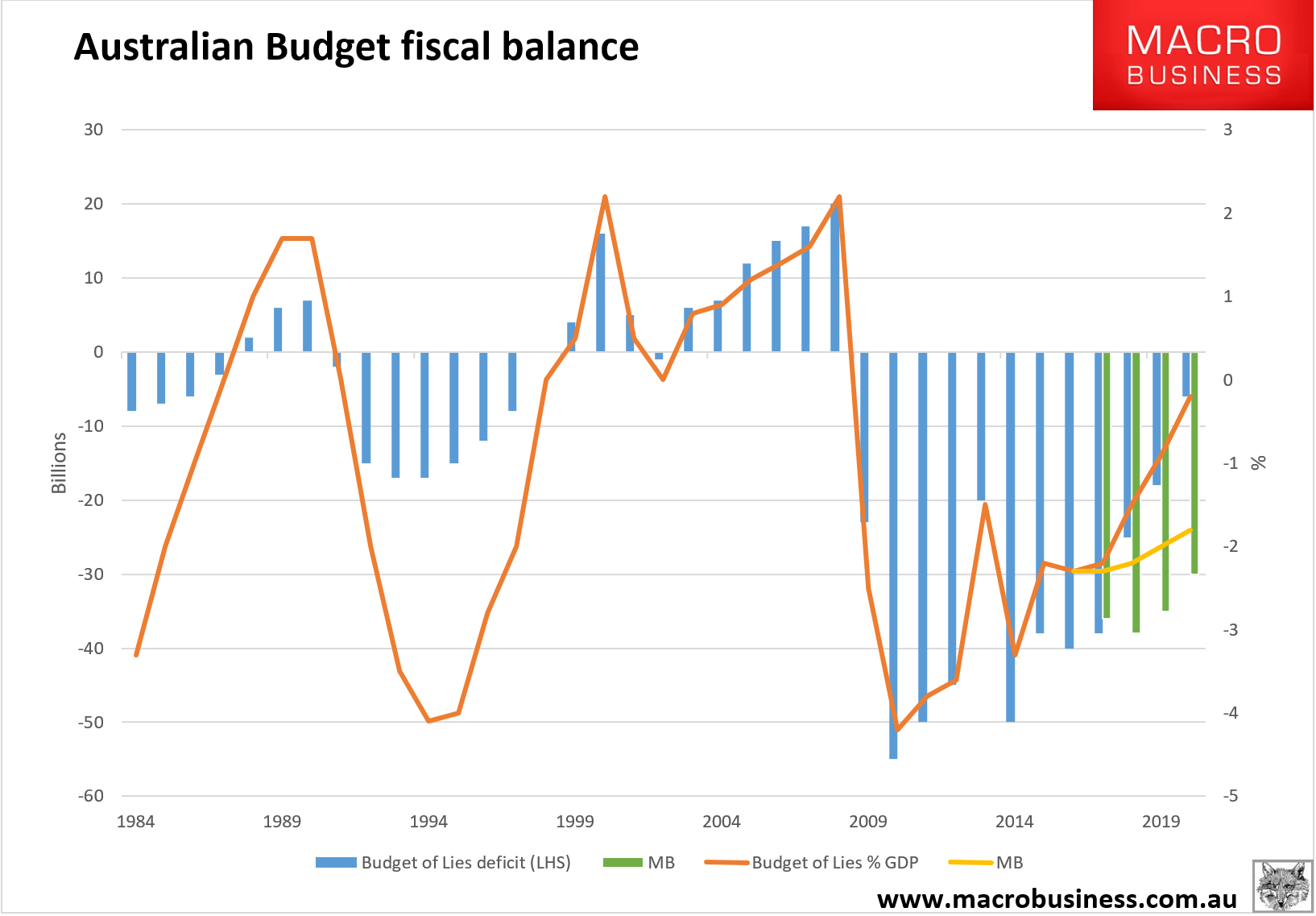

An indicative estimate by The Australian Financial Review based on research by Commonwealth Bank and Treasury suggests a surge in income from exports could cut as much as $23 billion off the $63.2 billion budget deficit for 2016-17 and 2017-18.

While at first glance the latest bounce in commodity prices is heartening, it also underscores that the Coalition government still has a massive task ahead of it in reducing the total $84.6 billion in deficits over four years and pulling back a debt load it has claimed could reach $1 trillion.

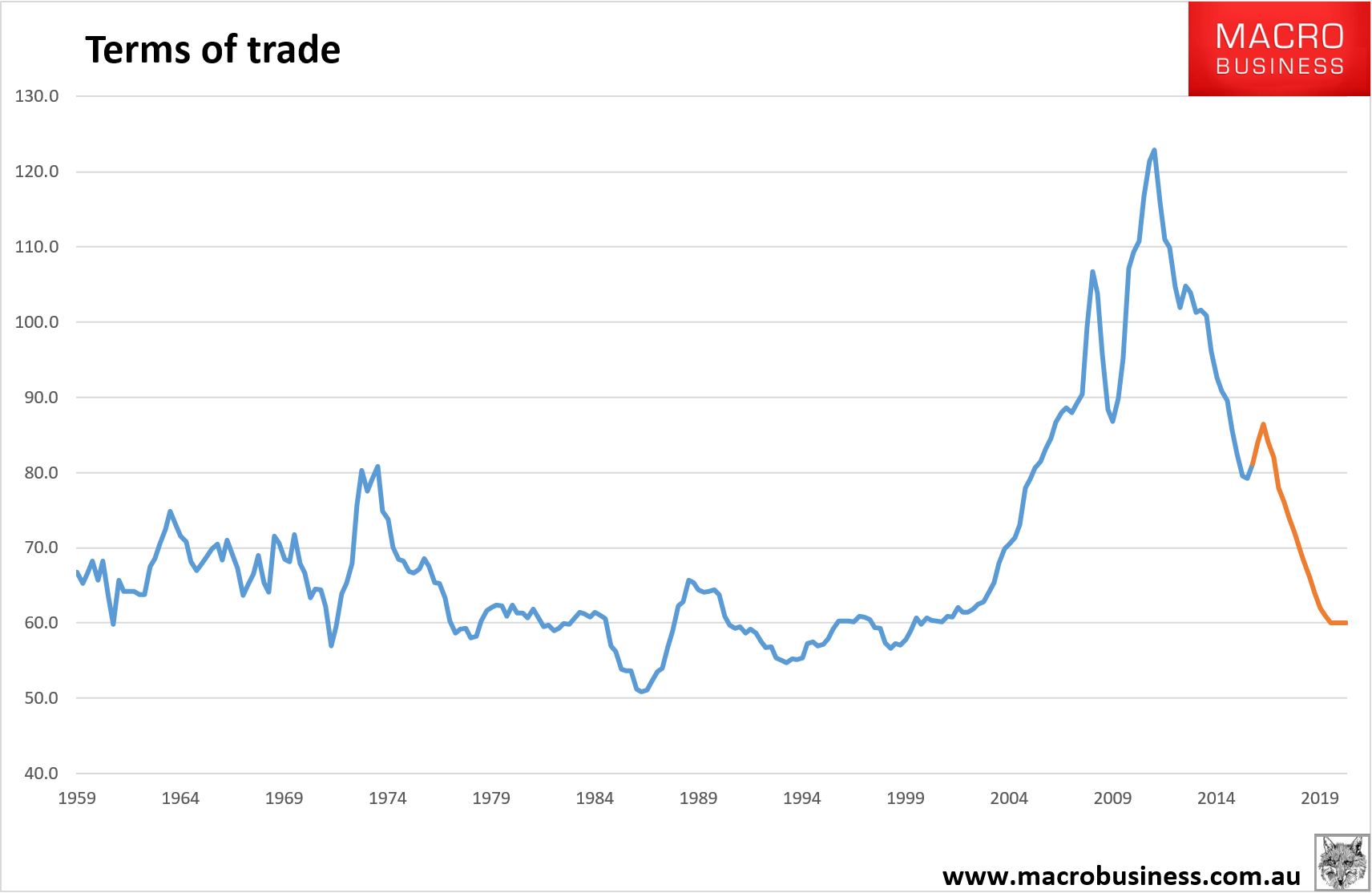

…Iron ore, the largest export, has also jumped by more than 30 per cent. Taken together, the three exports generate 50 per cent of total exports, so any gains will produce a major jump in the terms of trade and nominal gross domestic product, which measures what the nation is effectively paid from its shipments.

That’s right. And the 50% breaks down as 35% for iron ore and 15% for coal (5% thermal) or it did before the price rocket. Prices are not going to hold where they are so let’s look at what the impacts will actually be:

- thermal coal will be back at its lows by mid next year so it will see a three average quarter rise of 30% over three quarters adding 1.7% to the terms of trade;

- coking coal will halve by mid-next year so it will see a three average quarter rise of 100% over three quarters adding 10% to the terms of trade;

- iron ore is going to keep falling from here so it will be detracting from the terms of trade. It is currently sitting right on its six month average at $57. I see it averaging $10 less from here over the next three quarters so that will withdraw 5% from the terms of trade.

The net result is a 6.7% lift in the terms of trade peaking in Q4 (from an already rebounding level):

This is most certainly of benefit. It will boost income though I question by how much given how soft labour market conditions are. A similar if less large rebound in the 2013 Chinese stimulus registered a little rise:

It will also help deliver the Budget of Lies result though its outlook was so aggressive that I don’t think the upside will be material:

More to the point, none of it will last.

Depending upon how quickly the dwelling boom begins to decline, the combined impact may be enough to hold up further rate cuts until H2 2017. The Australian dollar has already largely priced the boomlet but it too may need to see further decent falls in the term so trade to hit the MB target of 60 cents next year.

As I say, most welcome but not a game changer.