The PBOC this morning fixed the yuan at its lowest since 2010:

The market has since pulled back but I’d expect it to continue. Capital outflow has not stopped, from Investing in Chinese Stocks:

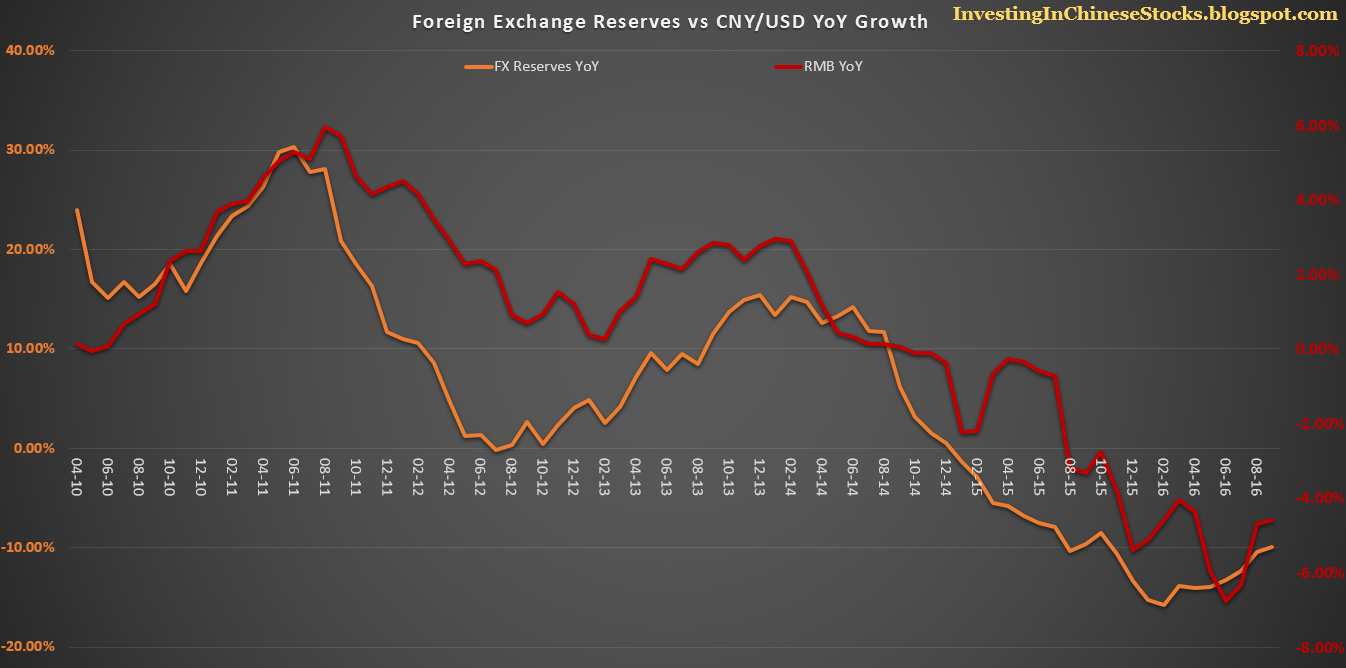

M2 figures come out next week, but unless M2 growth was brought to a standstill in September, reserve coverage of M2 will slide below 14 percent at current exchange rates. Based on credit growth things will only get worse, and as Balding points out in Some Brief Thoughts on Outflows, the dip may only be due to temporary success in the PBoC’s game of whack a mole.

SCMP: China’s forex reserves fall more than expected in September, by US$18.8b

China’s foreign exchange reserves have dropped for the third month in a row, with September’s data showing the latest fall has exceeded market expectations as the central bank continues its ongoing efforts to defend the yuan’s exchange rate.

The nation’s forex reserves, the world’s largest, shrank to about US$3.166 trillion last month – down from US$3.185 trillion in August, according to data from the state administration of foreign exchange.

And with what is now a full force prudential tightening around property, China needs to find more ways to grow if it is to reach its targets.

It ain’t rebalancing but who cares!