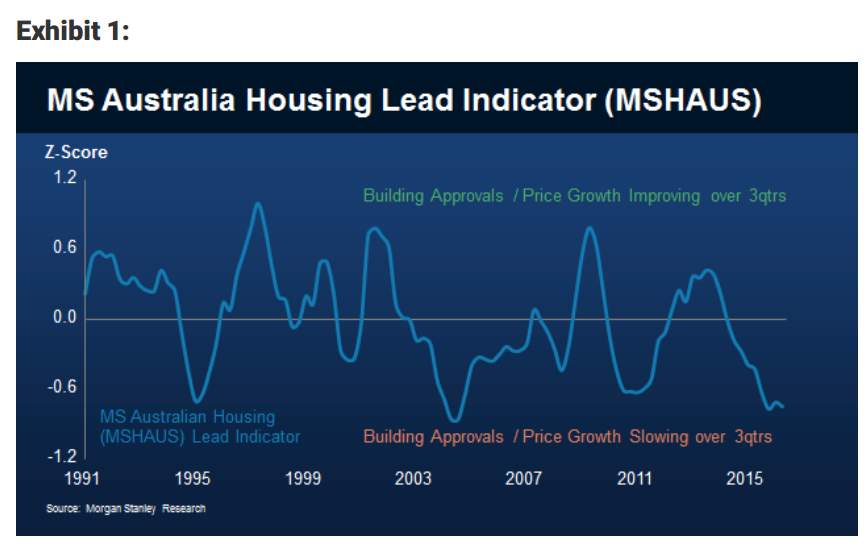

Morgan Stanley has produced a new housing leading indicator, MSHAUS, which seeks to identify turning points in the cycle for prices and construction. The news is poor:

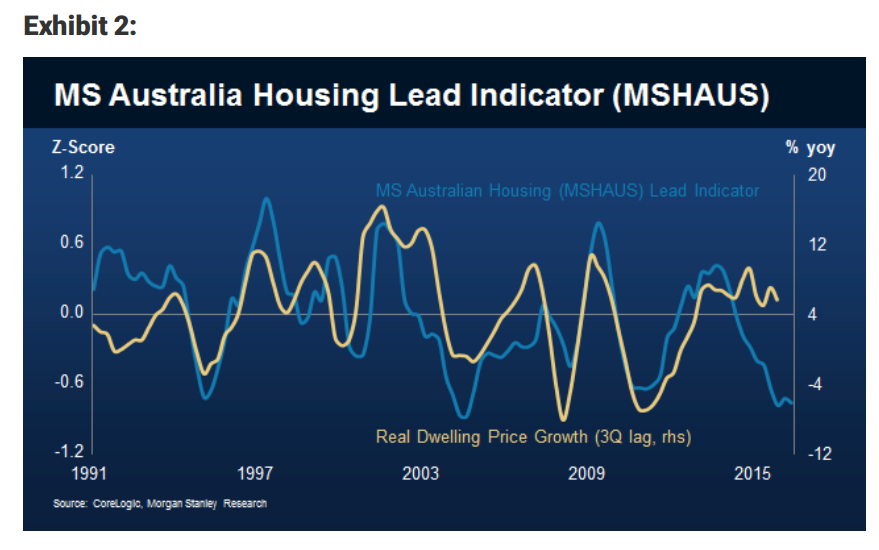

The index has reasonable history of leading house prices:

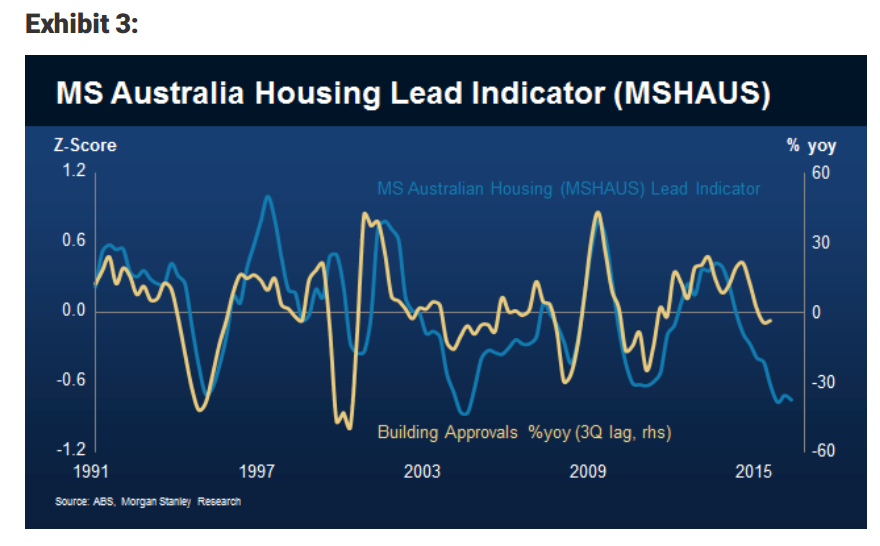

And even better for starts:

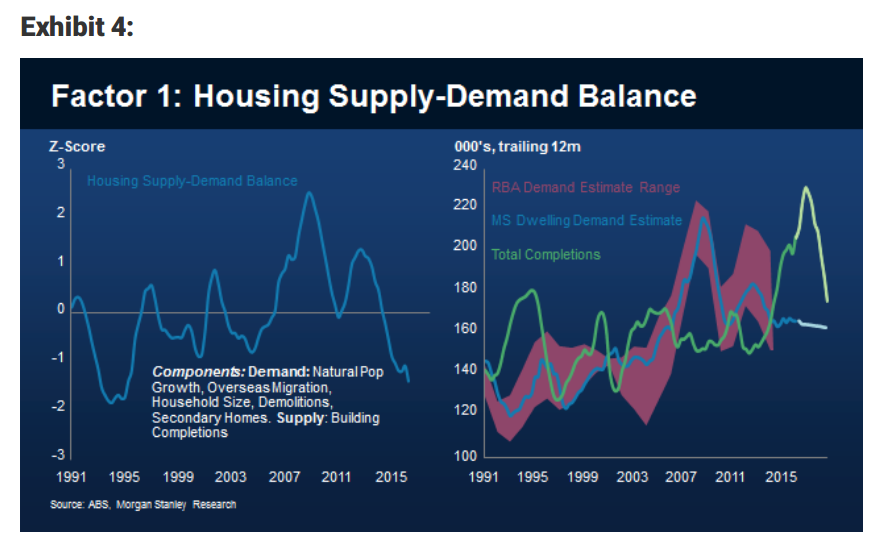

One the inputs to the index is MS’s assessment of housing market balance which shows the biggest glut in twenty years and heading for worse still:

MS expects an apartment hard landing and detached market soft landing. Given the centrality of housing construction to economic activity these days it is my view that, if anything, that is being conservative on the fallout. They recommend the following for building materials stocks:

Key themes for residential exposed stocks (recommendations unchanged):

FBU – OW: NZ residential cycle remains strong & commercial is also robust. We continue to see upside to FY17 consensus & guidance,although we have adjusted our forecast mix of divisional earnings.

JHX – EW: Although we see volume growth in the US as likely to remain strong in the near term, our analysis of margins suggest downside risk to company FY17 guidance. US housing has slowed in recent months with single family starts flat over the past 3 months YoY.

BLD – UW: Concrete volumes are more exposed to residential (~45%) than the market assumes. WA exposure will continue to affect the outlook. US improvement likely slower than market expects.

CSR – UW: Current price implies ~13.2x P/E on building products division which, given the point in the cycle,appears high. Knauf risks for CY18 remain. Aluminium division likely to report declining earnings given roll-off of ingot premium ahead of the step up in electricity prices 1 Nov 2017.

DLX – UW: Despite upside risk to consensus, we remain cautious given slowing housing turnover. Consolidation in retailer base is also likely to affect DLX either through volume or price. Ex-Alesco assets performance remains poor.

ABC – UW: Geographic exposure negatively affects the company. Competition in NSW cement market also caps pricing somewhat despite robust volumes. Strong balance sheet & yield,however, does provide some support.

The other obvious implications are further rate cuts and a lower dollar.