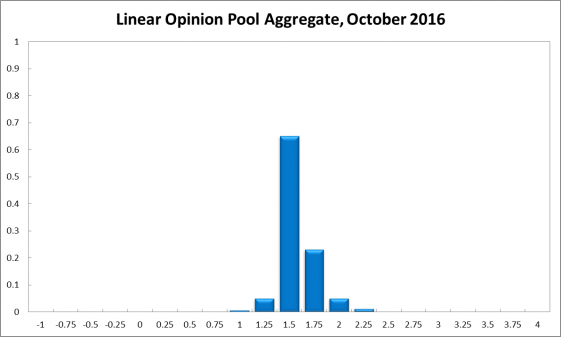

There is little economic news, not even OPEC’s decision to cut oil output, to justify a change in the current cash rate. Unemployment fell yet again, albeit slightly, and consumer price inflation, at 1.0% year-on-year, remains well below the RBA’s 2-3% target band. The CAMA RBA Shadow Board clearly believes that the cash rate should remain at its current level. The Shadow Board attaches a 65% probability to a rate hold being the appropriate policy setting. The confidence attached to a required rate cut equals 6%, while the confidence in a required rate hike equals 29%.

Australia’s unemployment rate fell another 0.1 percentage points, to 5.6%, according to the Australian Bureau of Statistics. The participation rate, too, fell slightly; it now stands at 64.7%. The labour market was pretty calm this month: full time employment increased by 11,500 and part-time employment decreased by 15,400. There is no new data for the seasonally adjusted wage price index.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.