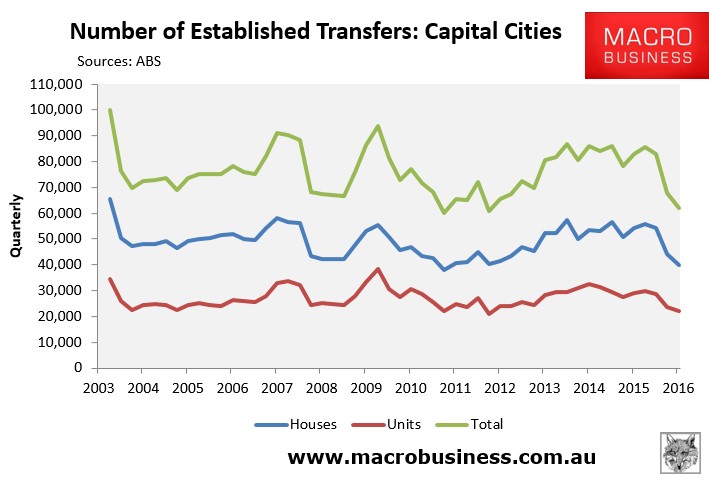

I had a fascinating conversation with a real estate agent today. In it he described the collapse of housing turnover since the introduction of macroprudential tightening, that MB has labelled “shrinkflation”:

He said that his data was indicating that both Sydney and Melbourne Spring season turnover was running at -40% versus last year.

He described building carnage across the real estate sector. Not only are volumes getting creamed, agents have lost pricing power as well. Even though higher prices should be boosting margins they are not because commission structures are collapsing amid increasingly cut-throat competition for market share.

Job losses have begun and will get worse. There are too many agents for the “shrinkflation” market and consolidation is looming.

The agent was convinced that this is a long term change. Unaffordability has reached such extreme levels that people are afraid to move and the transaction costs are so enormous that they can’t face it anyway.

This has a number of implications for certain segments of the economy and perhaps at the macro level as well.

For a start, directly associated sectors that traditionally benefit from a housing bull cycle are now effectively in an outright bust even though prices aren’t. Pretty much the entire value chain of house selling is a volume based business, from agents, to media, to legals, even banking.

Retail sales also have a large component of household goods that are under increasing downwards pressure:

At 20% of retail turnover this will not end the world but it is adding pressure at the margin, and all of the effected sectors are now contributing job losses and less capital expenditure in areas that have been a key contributor to the so-called post mining boom “rebalancing”. Moreover, pressure is likely to persist if not get worse for a while yet.

Shrinkflation may be of some benefit in the short term in increased renovation activity (and some narrowing wealth effect) but there is little evidence of it yet in the data and that uplift if it comes is going to be swamped by the downdraft emanating from the topping dwelling boom late next year.

The basic message is that “shrinkflation” is a quite poor cousin to yesteryear’s full-throated housing booms when it comes to economic spillovers and it will only contribute to more monetary easing in due course.

Given that that may only produce more increasingly narrow house price appreciation and thus even lower volumes, we do rather appear to be racing down the final furlong of the boom, waiting for something to push the whole top-heavy and unwieldy thing over.