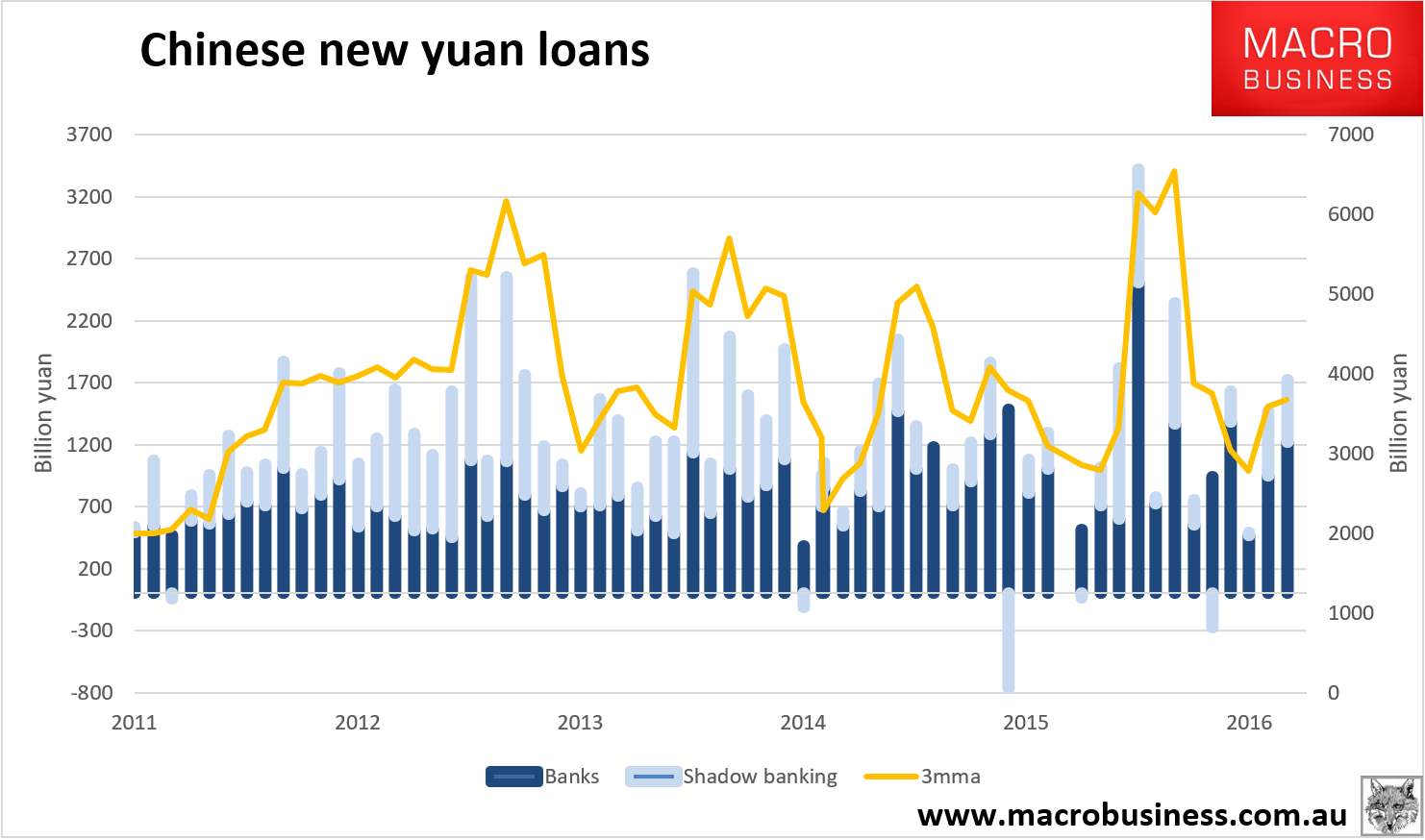

Chinese credit numbers for September are out and it’s clear why the they’ve hit the prudential brakes. Total Social Financing was strong at 1.72tr yuan and bank loans were 1.2tr yuan. Both were well above consensus:

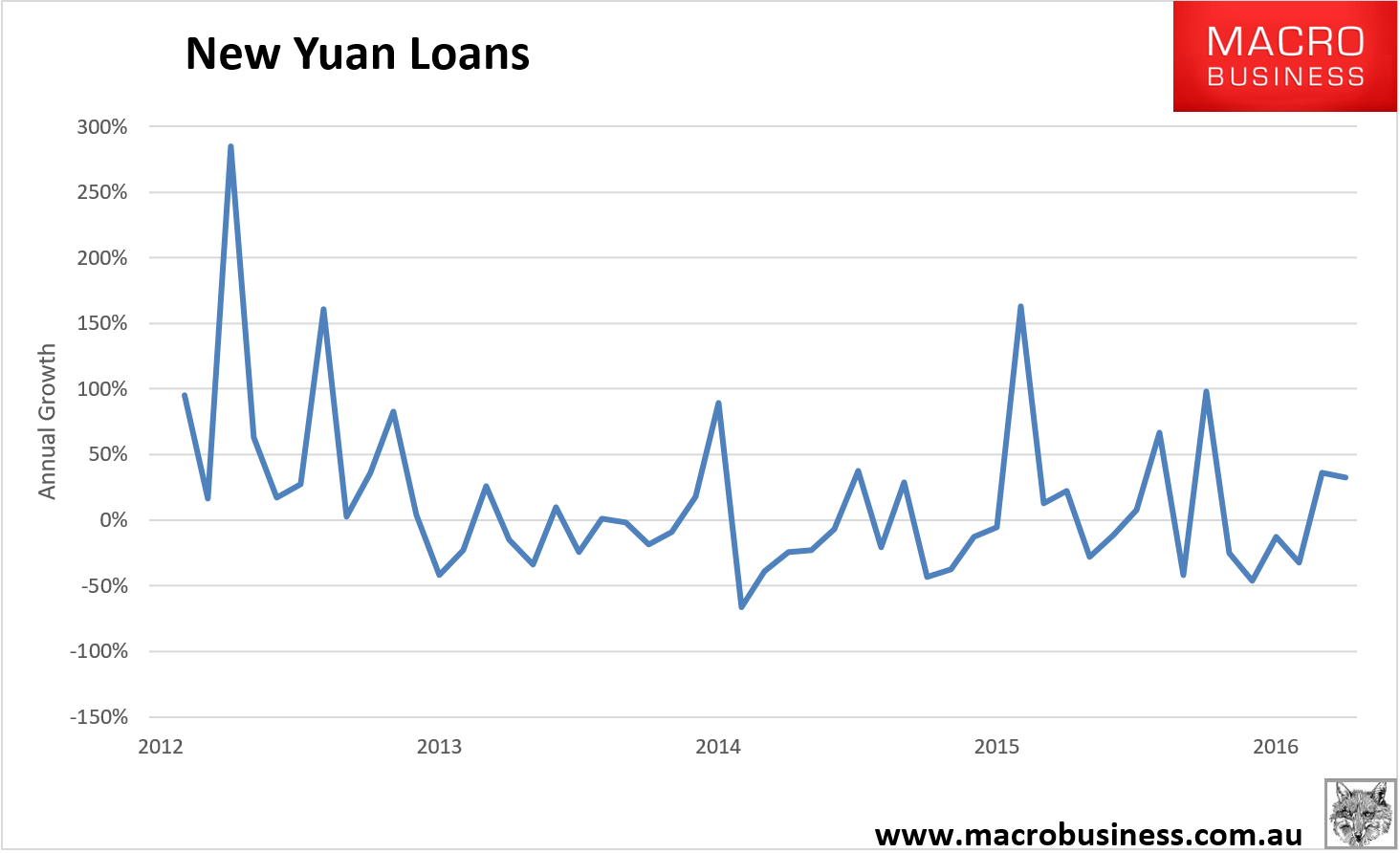

Year on year growth is still running hot at 32%:

Advertisement

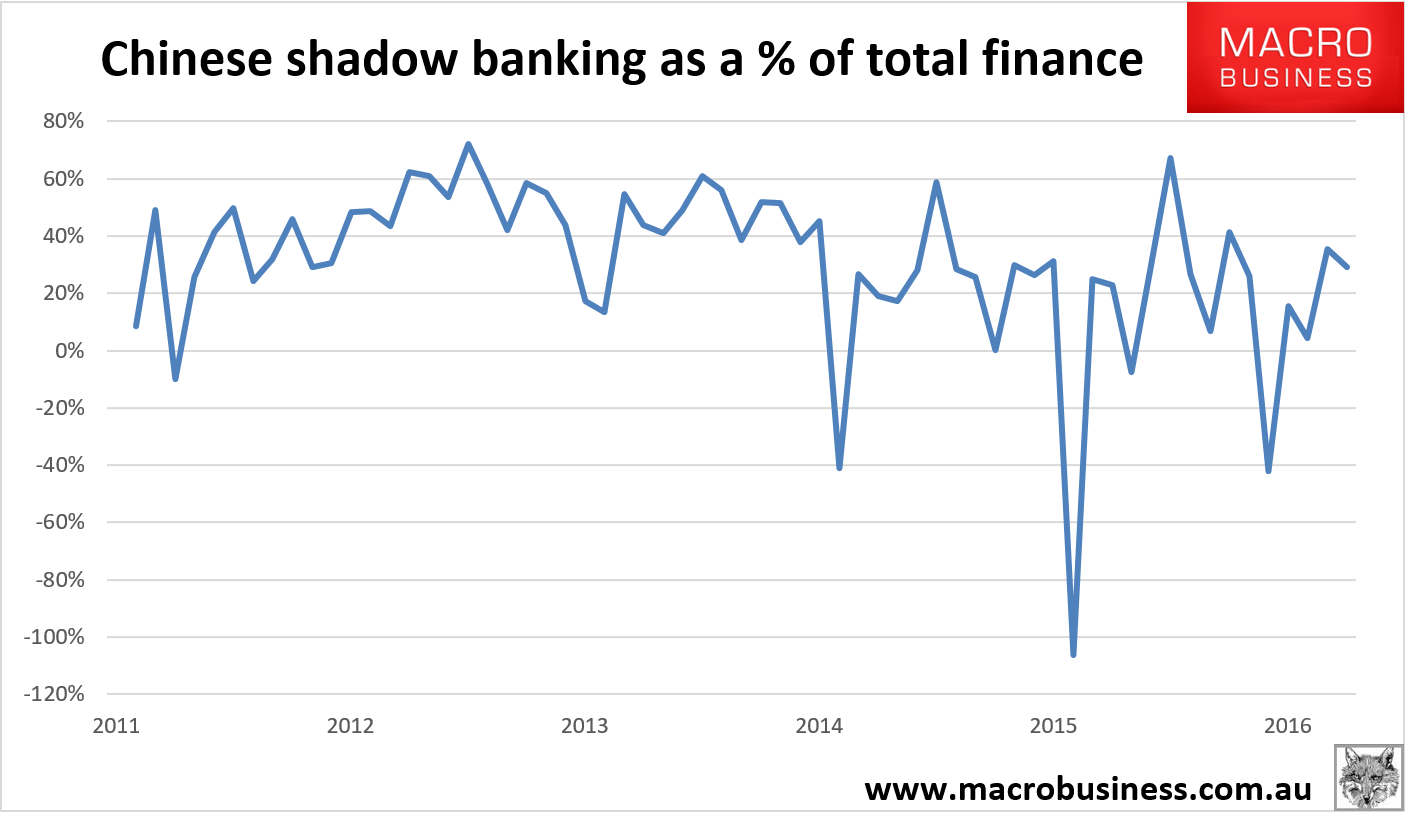

Shadow banking is not really shrinking so convincingly any more:

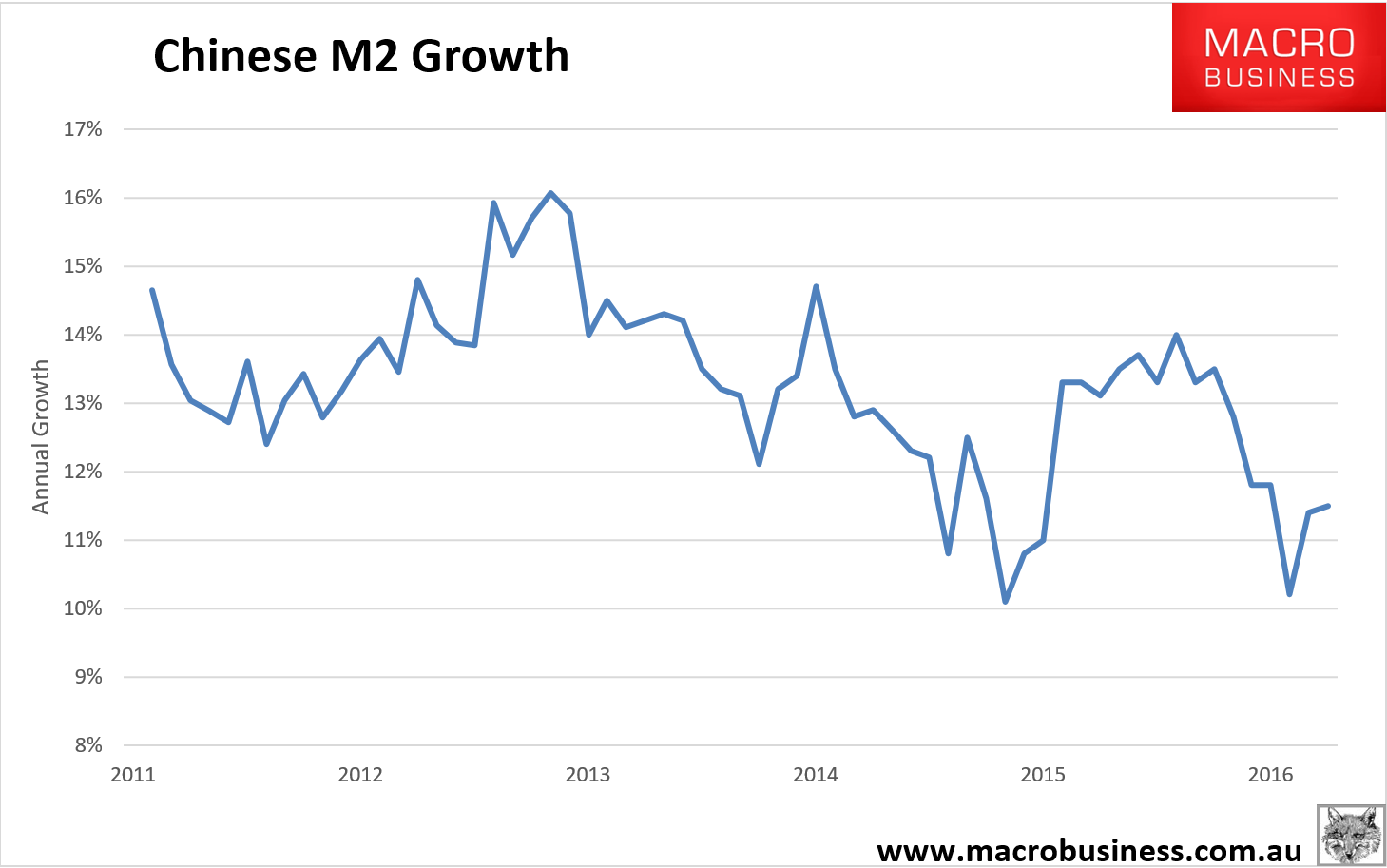

M2 is 11.5%:

Advertisement

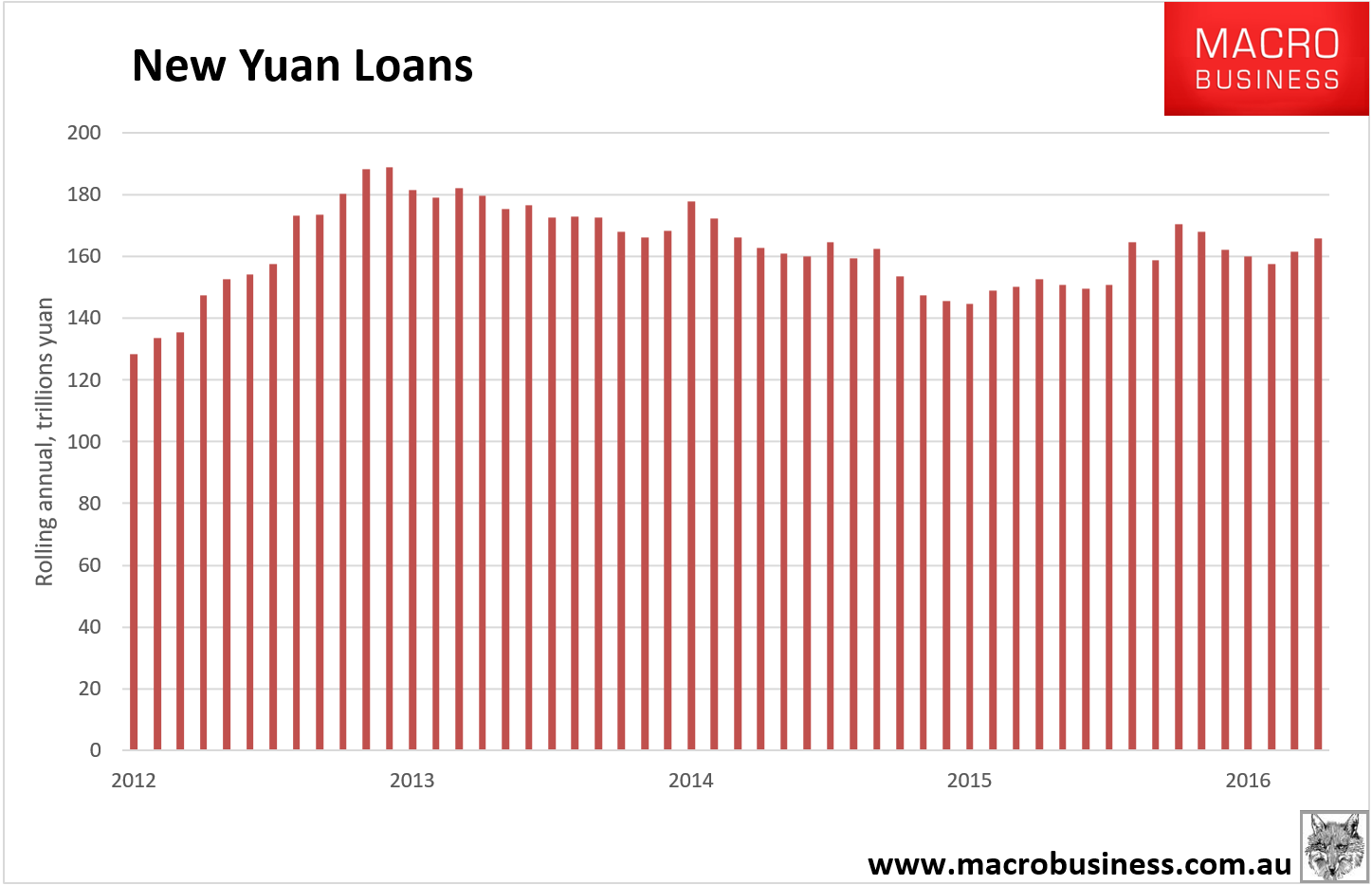

And the rolling annual has reformed an uptrend:

This was before authorities pulled the prudential handbrake in October. And things may be much hotter than they appear, from Barclays:

In early 2011, the PBoC launched a new data series, total social financing (TSF), as a comprehensive indicator to monitor the economy’s total fundraising. Its development was in response to the rapidly growing shadow banking and direct financing amid increasing financial disintermediation and regulatory arbitrage. As a result of these changes in China’s financial landscape, it was thought that traditional indicators such as bank loans or deposits no longer captured the full picture of financing/investment and money supply/demand.

Over time, TSF developed into a macro control tool, together with broad money (M2). “To maintain a reasonable growth in the money credit and TSF” is now a phrase written in the annual government work report since 2011. In March 2016, the government for the first time set an explicit target for TSF growth of 13%, slightly higher than actual growth of 12.4% in 2015, in addition to its 13% M2 growth target (up from a target of 12% in 2015).

Defined by the PBoC to measure the domestic financial sector’s (non-government) support to the real economy, the TSF statistics include bank loans, corporate bonds, three traditional shadow banking activities, as well as equity financing since its release in 2011(Appendix). The shadow credit includes loans by trust companies, inter-corporate entrusted loans, and undiscounted bankers’ acceptance bills. The TSF by design excluded: 1) government bonds, but has included the local government financing vehicle (LGFV) loans and bonds; and 2) external debt, such as foreign direct investment and other foreign borrowings.

Advertisement

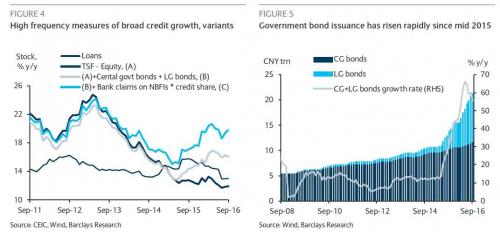

Recall that this year much of the bond financing for infrastructure shifted out of the TSF numbers. So the reality even stronger growth:

From a stock perspective, broad credit is 20-30% higher than what is counted in the official TSF data. Relative to GDP, our five measures put China’s credit-to-GDP ratio currently in a range from 260% to 275% of GDP as of September 2016.

From a growth rate perspective, the speed of credit expansion is alarming. Our methods put the current pace of credit growth in China in a range between 19% and 20%, well above the reported official TSF growth of 12.4% and new loan growth of 13.0% in September.

Using a bottom-up approach, we made ballpark estimations of the size of “shadow credit” based on the above discussions, which reached around CNY63trn as of September 2016. This is calculated by adding the ultimate forms of credit, ie, trust loans (September: CNY5.9trn), entrusted loans (CNY12.5trn), bankers’ acceptances (CNY3.8trn), corporate bonds (CNY17.3trn), and other non-standard credit assets5 (CNY23.5trn).

China’s debt crisis does not appear to be imminent. China’s debt is largely domestically owned. Hence,unless there is bank run or capital flight by local residents, the typical EM-style financial crisis, like the Asia Financial Crisis, is less likely. The heavy state involvement, with the majority of loans coming from state-controlled banks to state-owned enterprises, the strengthening state control and sizable state assets suggest that the Chinese government still has the capacity to manage the pace of NPL recognition and debt restructuring in the banking system.

On the other hand, the current pace of credit expansion, more than twice the rate of nominal GDP growth, is clearly unsustainable (Figure 13).

The interconnectedness between the corporate sector and the banks points to systemic risks in the economy, especially as the economy is forecast to slow further. Such perceived “implicit guarantees” by the state have resulted in excessive risk-taking across asset classes (equity, bond and property), across economic agents (corporate, local governments and households), and across financial intermediaries. With rising central government’s contingent liability, the sovereign risks are increasing. Moody’s downgraded its outlook on Chinese government debt to negative from stable in March 2016, questioning China’s surging debt burden and the government’s ability to enact reforms.

I still think the prudential handbrake is going to work but there is enough going to here to anticipate a decent tail of construction activity into H1 2017.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.