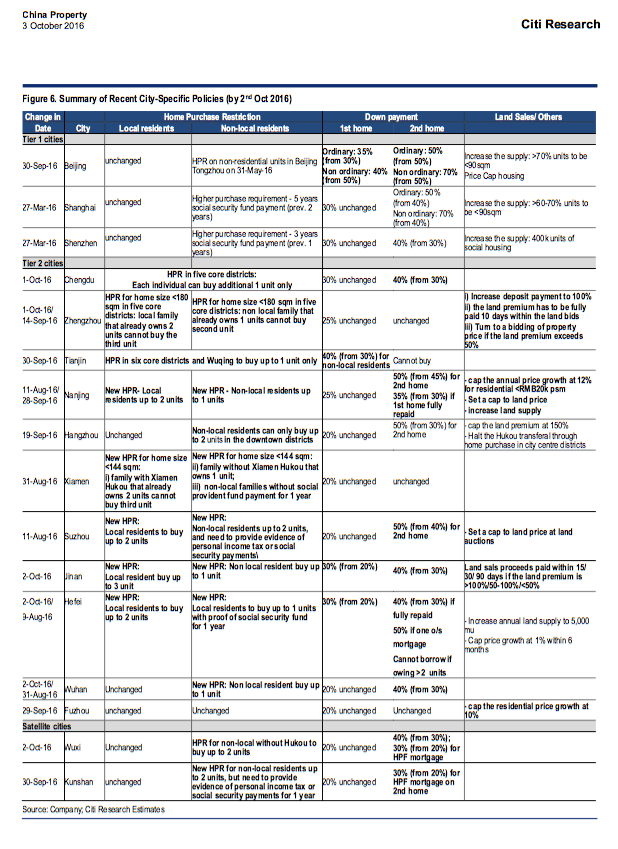

Prudential property curbs have intensified in the Chinese cities of Shenzhen and Souzhou. Here is Citi’s full list of recent tightening:

The air is going to come out here. How bad will be the fallout? Manageable in my view. HSBC agrees:

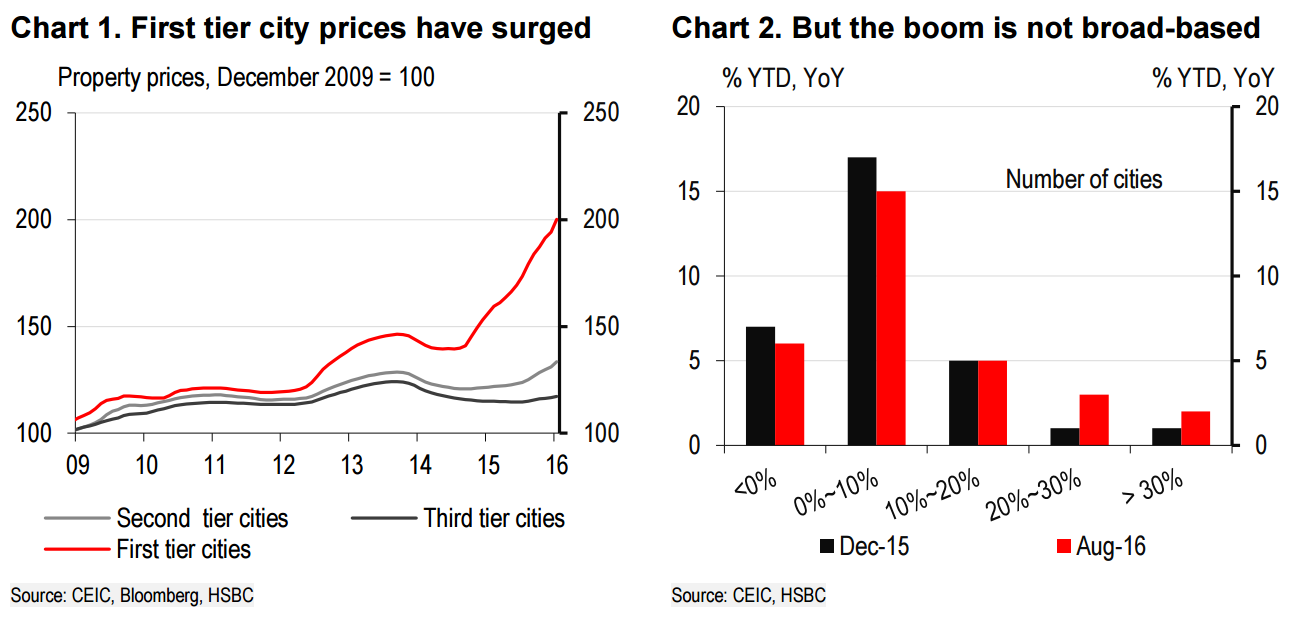

Lately, fast-rising property prices have been generating many headlines. Property prices rose 28% y-o-y in the four Tier 1 cities (Beijing, Shanghai, Guangzhou and Shenzhen) in August, continuing a year of double-digit gainsand fuelling talks of a‘propertyprice bubble’. But the national picture is far more uneven, or even divergent. Outside of Tier 1 and Tier 2 cities (the top 35 cities account for only a fifth of the national market), prices are at best flat amidst high levels of inventory. Outside of the top four cities, average levels of affordability in urban area are reasonable and still better compared with a decade ago. And, while mortgage loans have grown faster in 2016, overall household debt levels are still low. Therefore, selective macro-prudential policies, appropriate for local conditions, are better solutions than broad-based monetary tightening.

Meanwhile, the real economy still faces strong headwinds, such as slowing private investment and a prolonged weakness in exports. This calls for continued policy easing. The focus of policy easing continues to shift from monetary to fiscal. We have recently pared back our monetary easing calls for 2016 and 2017, while increasing our fiscal deficit assumptions. Faster fiscal expansion is more effective at supporting growth and will also help to address concerns over ‘asset price bubbles’ by channelling more liquidity into the real economy.

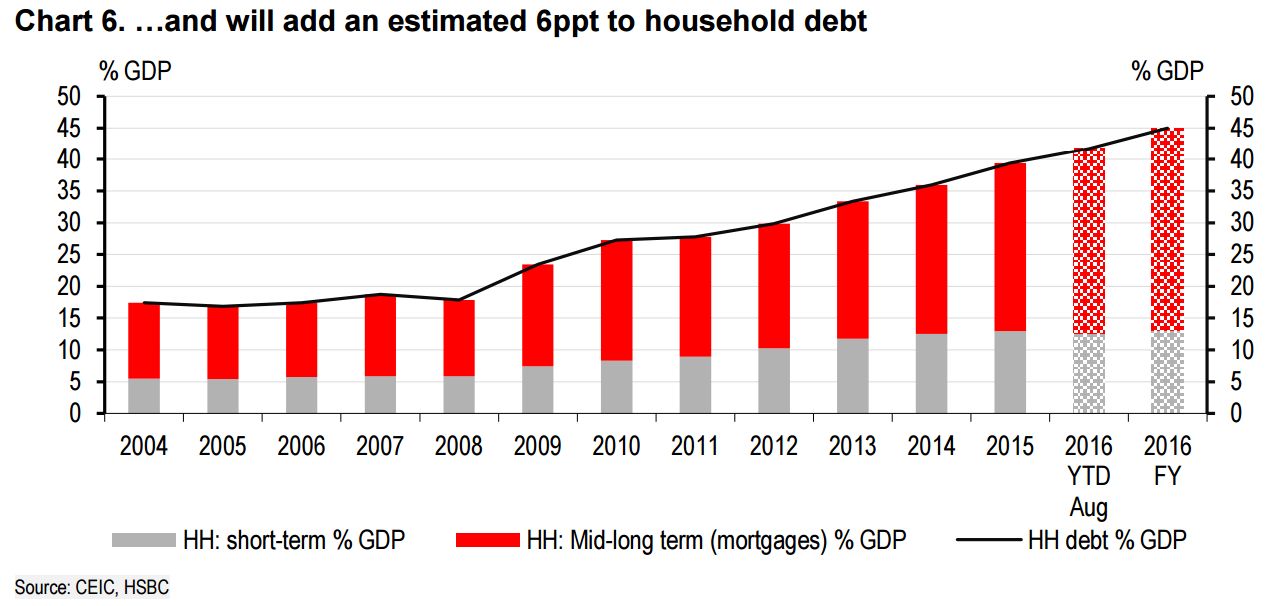

…Although fast price increases in Tier 1 cities do pose a policy challenge in terms of managing these relatively more mature markets, the risks they pose to growth and financial stability are not large at the present stage. From a growth perspective, the downside risks to growth are, in fact, smaller now than during the downturn in 2015. Back then, property investment growth was coming down from six years of uninterrupted double-digit growth. According to our estimates, in 2015, the 10ppt slowdown in property investment growth shaved close to 1ppt off nominal GDP growth. Fast forward to September 2016, we believe the picture does not look as dire. Despite several months of strong sales growth, the rebound in property investment has been far more muted. After having dipped briefly into negative territory, property investment growth rebounded in 2016 but to a modest degree (Chart 4). In the first eight months of 2016, property investment grew 6.2% y-o-y. We think the more muted response in investment growth in the upturn means a potentially smaller drag on growth should the above macro-prudential measures more materially impact sales growth. This is also consistent with anecdotal evidences that property developers have generally been more cautious with land purchases over the past year, preferring to limit themselves to premium slots in Tier 1 cities where record-breaking deals invariably attract many headlines.

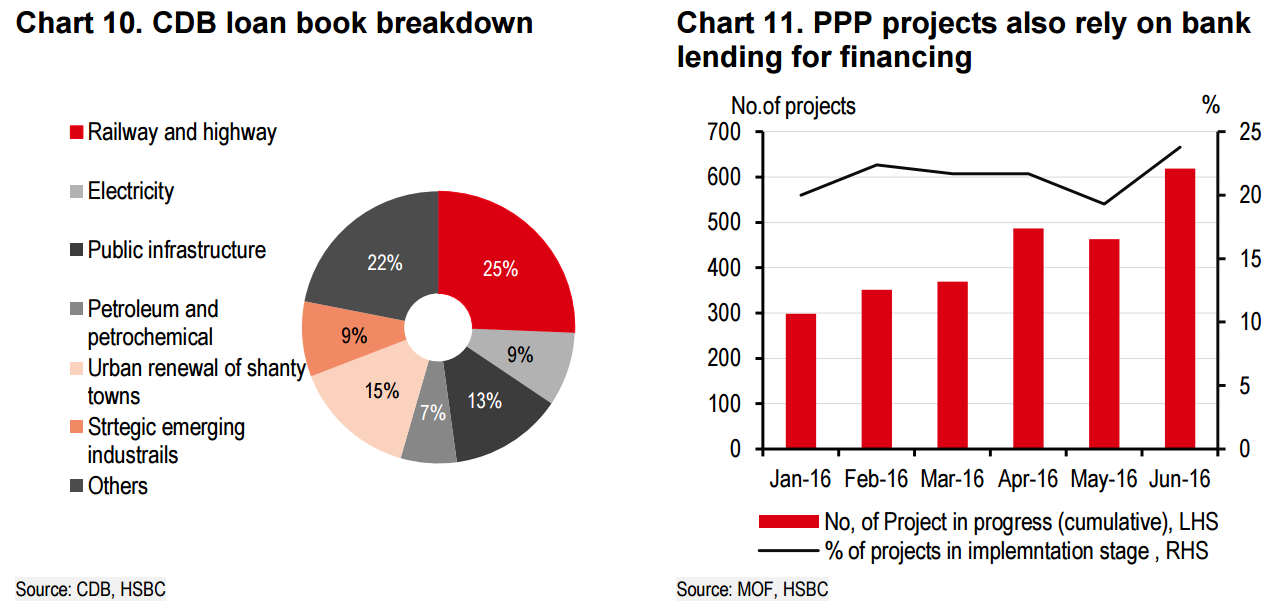

However, fiscal expansion need not entail monetary tightening. In fact, successful fiscal expansion requires some degree of monetary accommodation. This is because the infrastructure-centric nature of fiscal expansion requires support from market liquidity, policy banks and commercial bank lending. China Development Bank (CDB) alone has issued (so far this year) over RMB1.4trn worth of policy bank bonds, an estimated RMB1trn of Special Financial Bonds, and will likely provide over RMB2trn of loans in 2016. Some of these are used as seed capital, which means the rest of the funding will come from commercial banks. Private Public Partnership (PPP) projects, of which RMB1trn are in progress, also count commercial bank lending as the main source of financing. Our base line case for 2017 is for the general budget deficit target to be raised to 4% of GDP. However, unless the deficit target turns out to be significantly higher, monetary policy will likely need to remain accommodative throughout 2017 as well.

Advertisement

HSBC are always China bullish and I usually ignore them. However this is more or less right. This is another of the rolling bubbles we’ve seen in China’s glide slope management – bonds, shares, property – and it is not broad enough to represent a systemic risk to banks. As well, prudential tightening has a strong history of slowing markets not popping them.

What it does represent is a major developing headwind for Chinese construction commodities. Not as severe as 2015 but strong nonetheless given the centrality of Chinese housing construction to iron ore, coking coal and copper demand, despite strong ongoing fiscal support.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.

Meanwhile, the real economy still faces strong headwinds, such as slowing private investment and a prolonged weakness in exports. This calls for continued policy easing. The focus of policy easing continues to shift from monetary to fiscal. We have recently pared back our monetary easing calls for 2016 and 2017, while increasing our fiscal deficit assumptions. Faster fiscal expansion is more effective at supporting growth and will also help to address concerns over ‘asset price bubbles’ by channelling more liquidity into the real economy.

However, fiscal expansion need not entail monetary tightening. In fact, successful fiscal expansion requires some degree of monetary accommodation. This is because the infrastructure-centric nature of fiscal expansion requires support from market liquidity, policy banks and commercial bank lending. China Development Bank (CDB) alone has issued (so far this year) over RMB1.4trn worth of policy bank bonds, an estimated RMB1trn of Special Financial Bonds, and will likely provide over RMB2trn of loans in 2016. Some of these are used as seed capital, which means the rest of the funding will come from commercial banks. Private Public Partnership (PPP) projects, of which RMB1trn are in progress, also count commercial bank lending as the main source of financing. Our base line case for 2017 is for the general budget deficit target to be raised to 4% of GDP. However, unless the deficit target turns out to be significantly higher, monetary policy will likely need to remain accommodative throughout 2017 as well.