The Australian dollar is threatening to break out of 2016 trading range. But it’s not threatening to fall, it’s threatening to rise. The daily, weekly and monthly charts all paint the same bullish ascending triangle pattern:

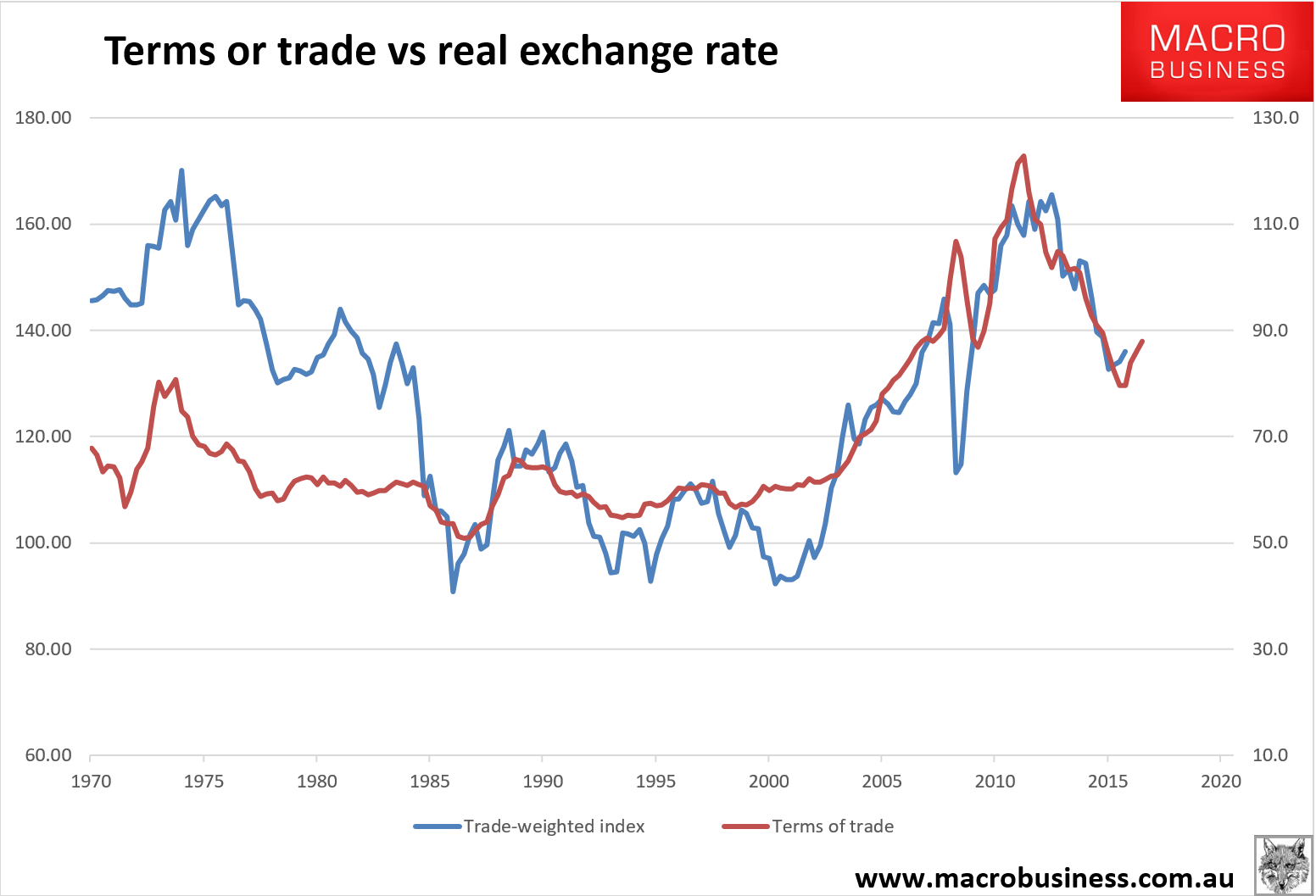

The two drivers are not hard to find. The first is the now pretty impressive bounce in the terms of trade:

And the second is Captain Phil and his balance sheets, from The Pascometer:

You should of course read the full speech yourself, but as you probably think life is too short, here’s my translation: low inflation is a worry and the RBA takes it very seriously, but there are some encouraging signs that the economy is starting to pick up and will pick up more over the next couple of years.

Specifically, Lowe said “our central forecast remains that inflation in Australia will gradually pick up over the next couple of years, although it is still likely to be closer to 2 per cent than 3 per cent”.

With interest rates already “very low”, that’s why the RBA left rates steady at the last board meeting. If you think we’re on the right track with the cash rate at 1.5 per cent, you’d need a good reason to cut it further.

Lowe reinforced that the RBA does indeed aim to have inflation – and the public’s expectations of inflation – average two to three per cent over time. However, he pointed out the mathematically obvious that it can do that by being both above and below the target zone for considerable periods. Combined with his House of Representatives economics committee chat, it seems the governor is not panicking about the present sub-target rate as long as he thinks we are heading in the right direction.

And he stressed the RBA wants to achieve the target in a way that best serves the public interest, balancing the needs of the labour market on one hand with the danger of people and businesses getting into too much debt on the other.

“Achieving the quickest return of inflation back to 2.5 per cent would be unlikely to be in the public interest if it came at the cost of a weakening of balance sheets and an unsustainable build-up of leverage in response to historically low interest rates,” he said. “Conversely, the case for moving more quickly would be strengthened in a world where the labour market was deteriorating and people were having increasing difficulty finding jobs.”

…I don’t think Philip Lowe wants to cut interest rates again. And I doubt if Scott Morrison would have stuck his head up to say he was opposed to further rate cuts if he thought the RBA was moving towards one. He has enough problems without looking silly by being wrong-footed by the RBA. And he does talk to the RBA often enough to get an idea of the bank’s thinking.

This is all short term thinking. The cycle is not at the bottom. Once the present tailwinds subside next year then we’ll see more easing. But, for now, Australia is enjoying a purple patch as the mining capex cliff slows, net exports boom, the dwelling construction boom lingers, fiscal policy is loose and the terms of trade are on a tear.

Markets are quite capable of rampaging into this short term narrative and bidding up the Aussie, especially as you have a mounting number of serious sell side analysts getting spooked at rebounding global inflation yet a Fed determined to ride it out by running its economy “hot”.

In fact, there is a plausible scenario in which the Aussie could blast higher short term:

- Chinese construction is going to come off but if it takes a quarter or two longer than I expect then iron ore could hold up for another six months;

- the coal boomlet might likewise linger a little longer;

- if we see the building La Nina deliver a good cyclone season then both markets could keep restocking without much pause right through Q1 2017 meaning more not less price pressure;

- the Q4 risk gantlet holding back markets has eased somewhat. If it keeps doing so then it’ll be risk on for emerging markets;

- and, if I’m right about the Fed not hiking in December then the monetary tailwind behind the Aussie is going to be spectacular.

That gives you Aussie dollar positives across MB’s five drivers fair value model in growth, interest rate differentials, sentiment, technicals and a softer US dollar.

This has a spike above 80 cents written all over it.

If it happens, it will not last long given all it will do is shock the economy and trigger more rate cuts, plus the bulk commodity price spikes will retrace soon enough and even the Fed can’t delay forever. Moreover, it would do nothing to alter my longer term view that the Aussie is heading much lower. But that does not mean it will not happen.