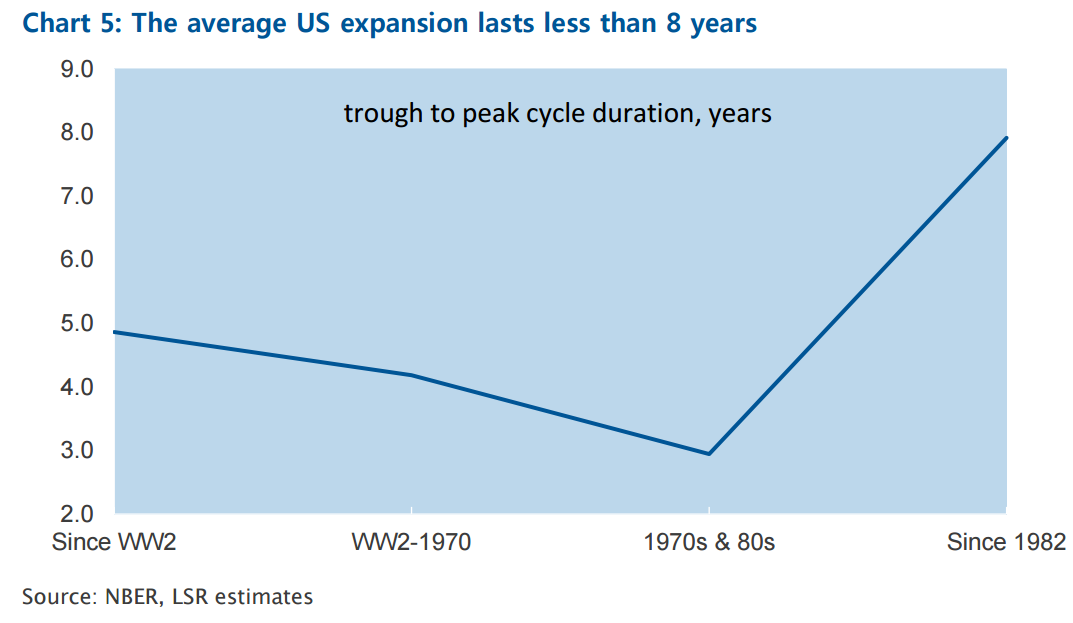

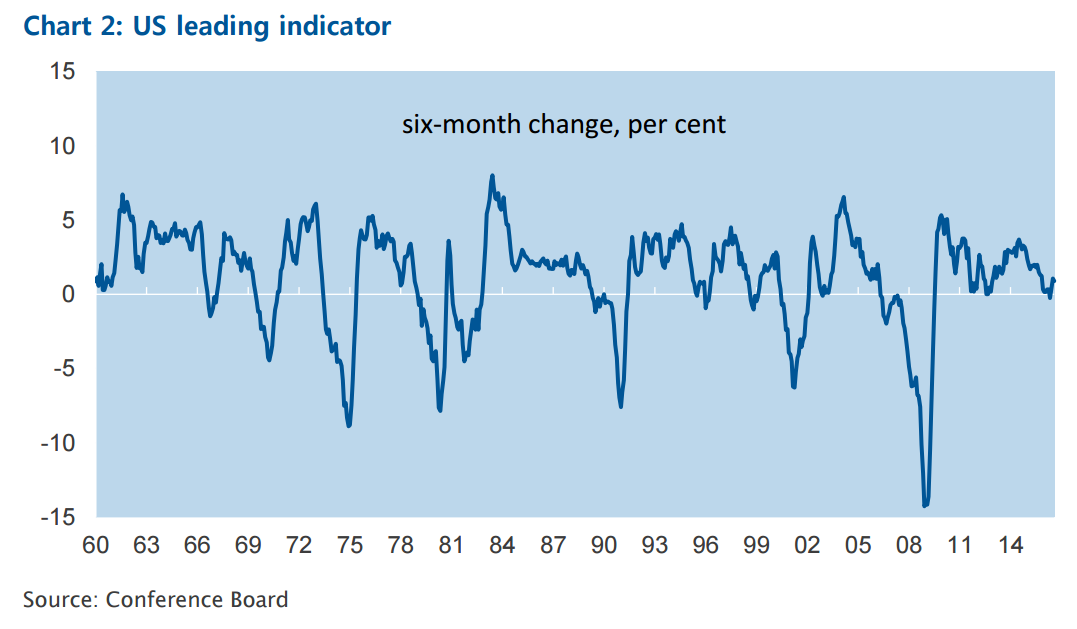

US recession fears were fairly widespread earlier in the year. With capex weak and manufacturing in decline, these concerns haven’t quite gone away. But leading indicators suggest short-term risks have diminished. This supports our view that the deceleration in the US economy over the past six months has been a ‘soft patch’, not the start of a major downswing. The combination of the collapse in energy prices and the surge in the dollar caused severe pain for the manufacturing sector but didn’t drag the rest of the economy down. Despite this resilience, many of our clients are worried about a US recession in 2017. After all, based on the average length of past cycles, the next downturn is already overdue.

While expansions don’t usually die of old age, long cycles can cause the build-up of macro imbalances that must eventually unwind, bringing recession. This means monitoring vulnerabilities, particularly in sectoral balance sheets, can provide a valuable insight. To illustrate, the 2001 recession was caused by over-investment and too much borrowing in the corporate sector, as businesses over-extrapolated the benefits of the New Economy. Profits peaked in 1997 but investment and stock prices continued to boom until 2000, the start of the dotcom crash. After that, US imbalances migrated to the household sector, as easy financial conditions inflated a bubble in housing, encouraged rapid increases in household debt and an unsustainable plunge in saving. Cue the subprime crash.

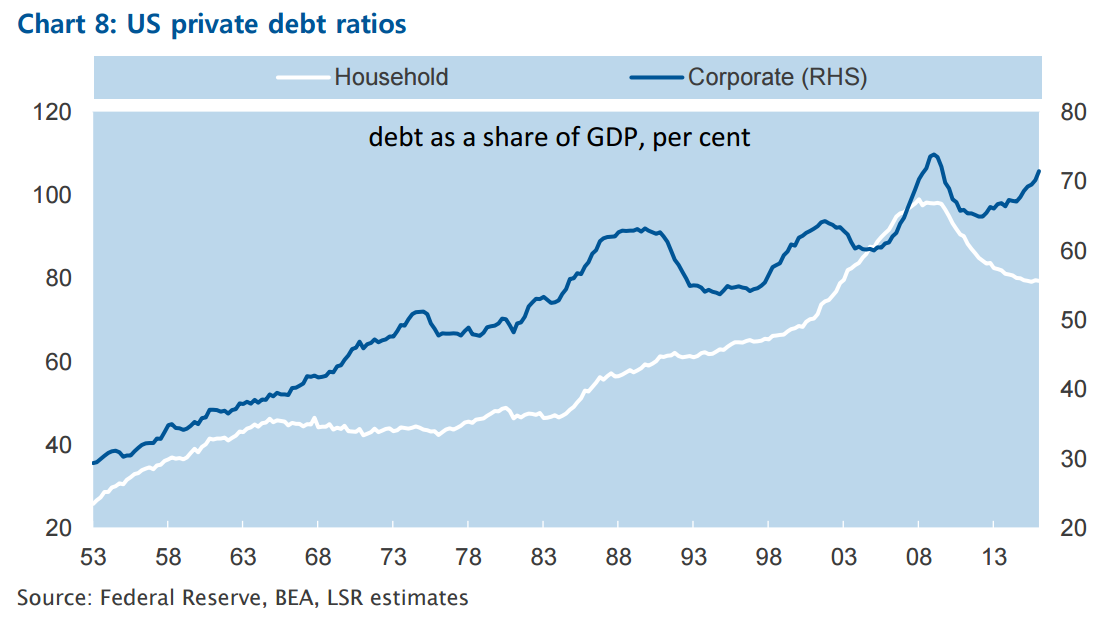

Households have deleveraged aggressively since 2008 and now, with relatively high saving rates, the sector doesn’t seem to present any obvious macro imbalances. The state of the corporate sector is somewhat shakier. US companies have been borrowing at a rapid pace in recent years, so on some measures (e.g. debt relative to their income or overall GDP), leverage now looks dangerously high. Profits have also deteriorated recently, albeit from very strong levels. Yet according to other metrics, the corporate sector is still in reasonable shape. Leverage is manageable when compared to net worth, the maturity of this debt is longer than in the past, companies have ample liquidity, and the business sector is running only a small financing gap, far below historical standards.

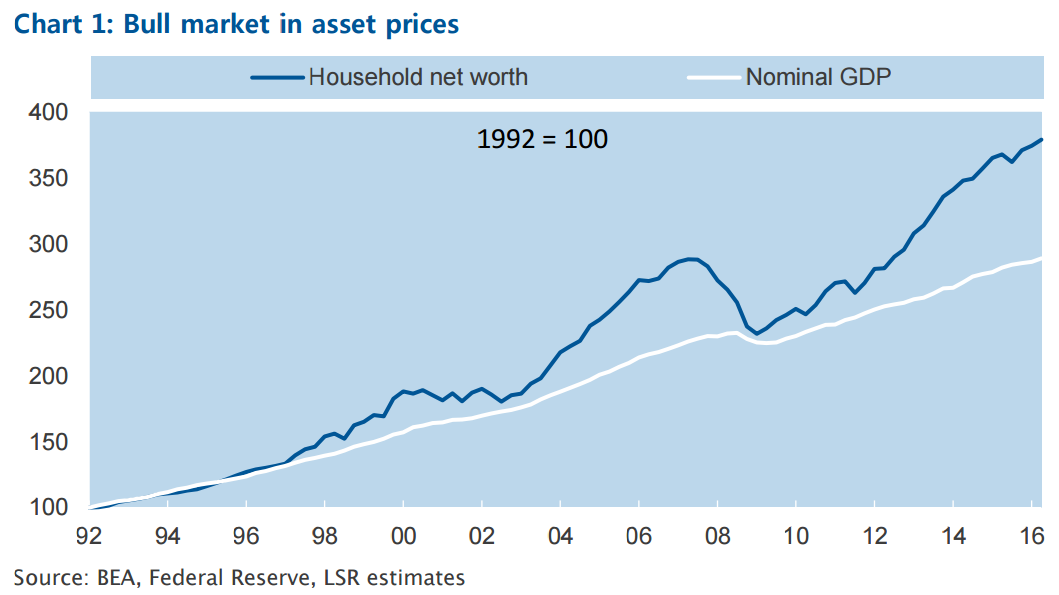

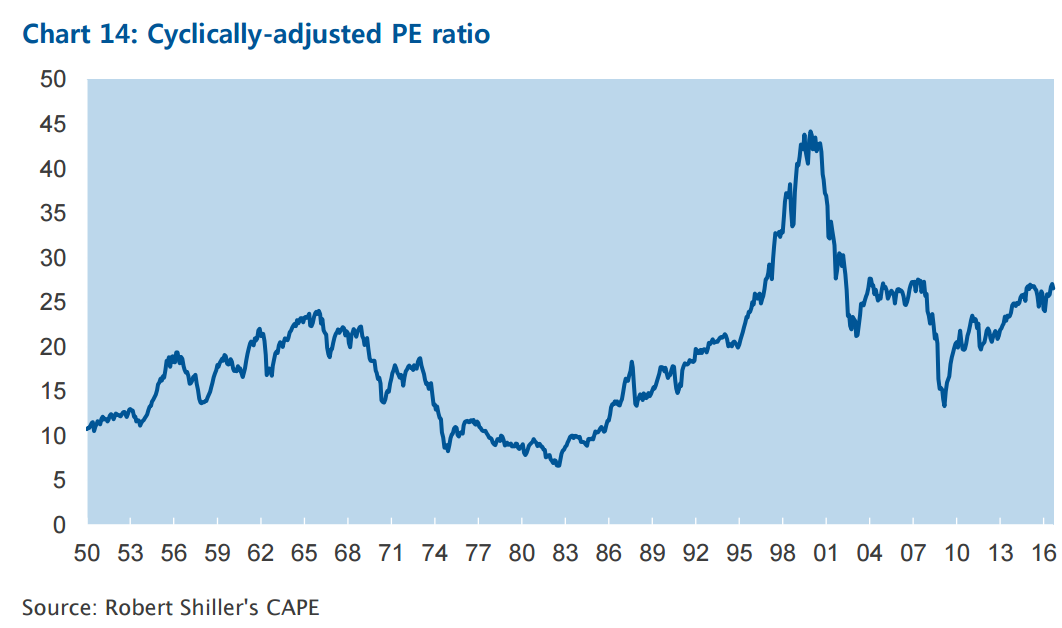

This economic cycle has also brought a rapid rise in asset prices. If unsustainable, this means balance sheets may not be as healthy as they seem. For example, a sharp decline in equity prices might force both households and businesses to retrench. Like the dotcom crash, this could be particularly painful for the corporate sector given higher debt levels. While it is too strong to claim the stock market is in a ‘bubble’, current valuations do seem vulnerable to a sudden rise in bond yields. Higher yields in 2017 might undermine equity prices and, if there were a large correction in stock prices, might also bring damage to the wider economy. But a severe downturn is unlikely, especially a repeat of 2008.

Statistically speaking, we are ‘overdue’ a US recession, but the slow recovery from 2008 has not generated the kind of macro imbalances typically associated with a major economic slowdown. Household balance sheets are in good shape, having deleveraged aggressively since the subprime crisis. The corporate sector is arguably in a shakier position, since companies have taken on significantly more debt in recent years. This leaves them exposed to a sharp decline in asset values and/or a further deterioration in profits. While we do not think the stock market is currently in a ‘bubble’, a sharp rise in bond yields poses a clear risk for 2017.

I think that that is right. ‘Policy error’ is the major US risk next year.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.