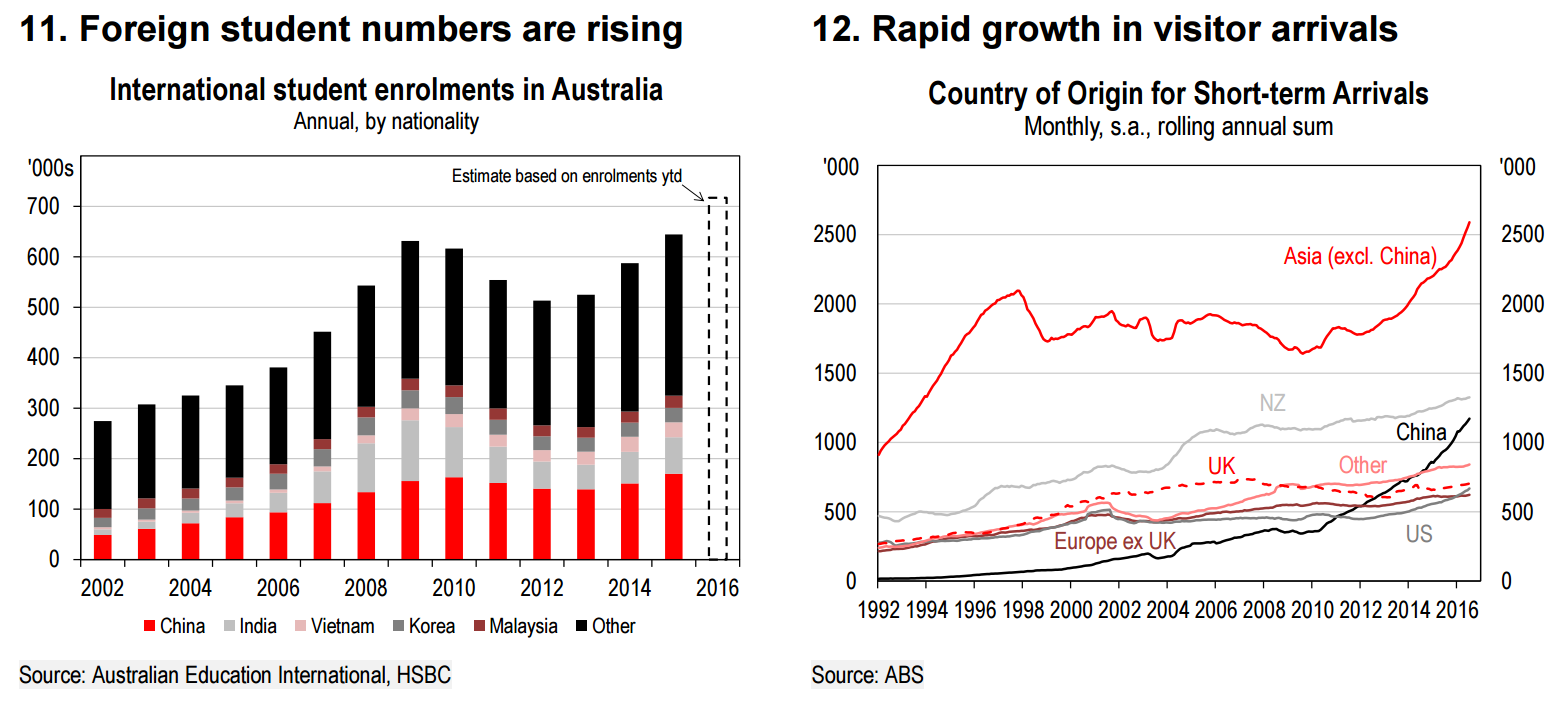

Bloxo offers some nice charts today on Australia’s ongoing net exports boom:

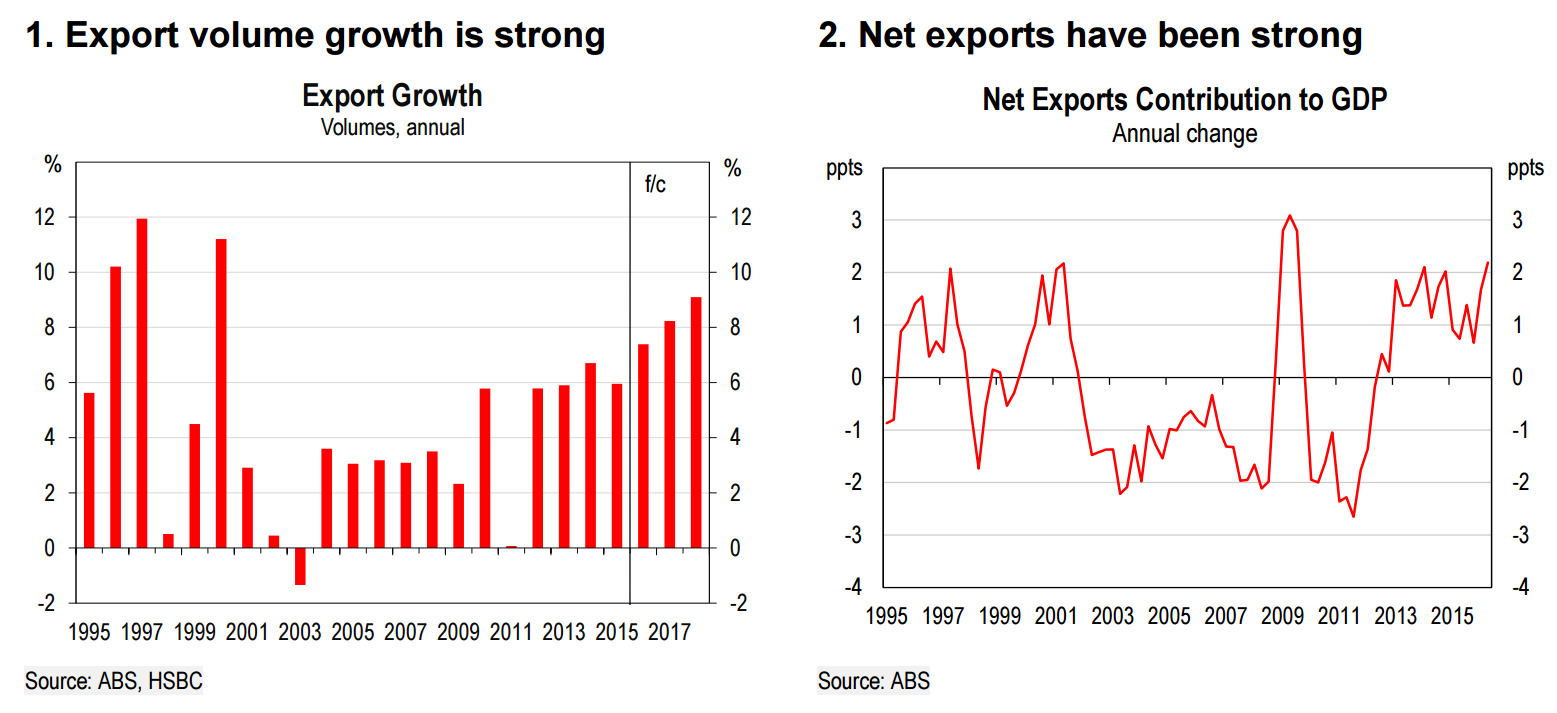

Global trade has been weak and policymakers in most economies are keenly seeking export-led growth. In volume terms, Australia already has it. Export volumes rose almost 10% y-o-y in Q2 2016 and have averaged around 6% growth each year for the past three years.

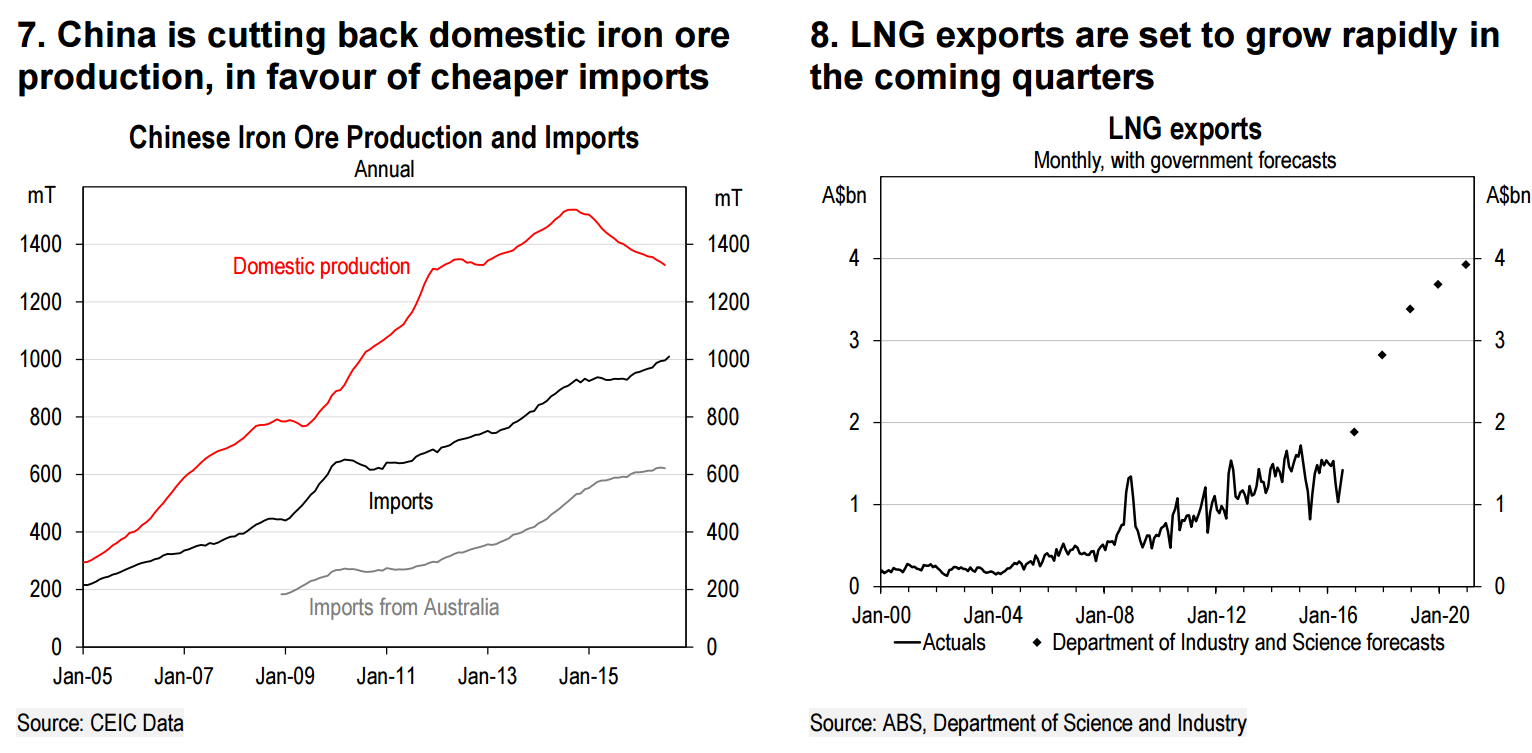

Export volume growth has been supported by continued Asian demand for Australia’s high-quality resources, such iron ore, coal, liquefied natural gas and base metals, as new capacity has come on-line in Australia’s resources industry.

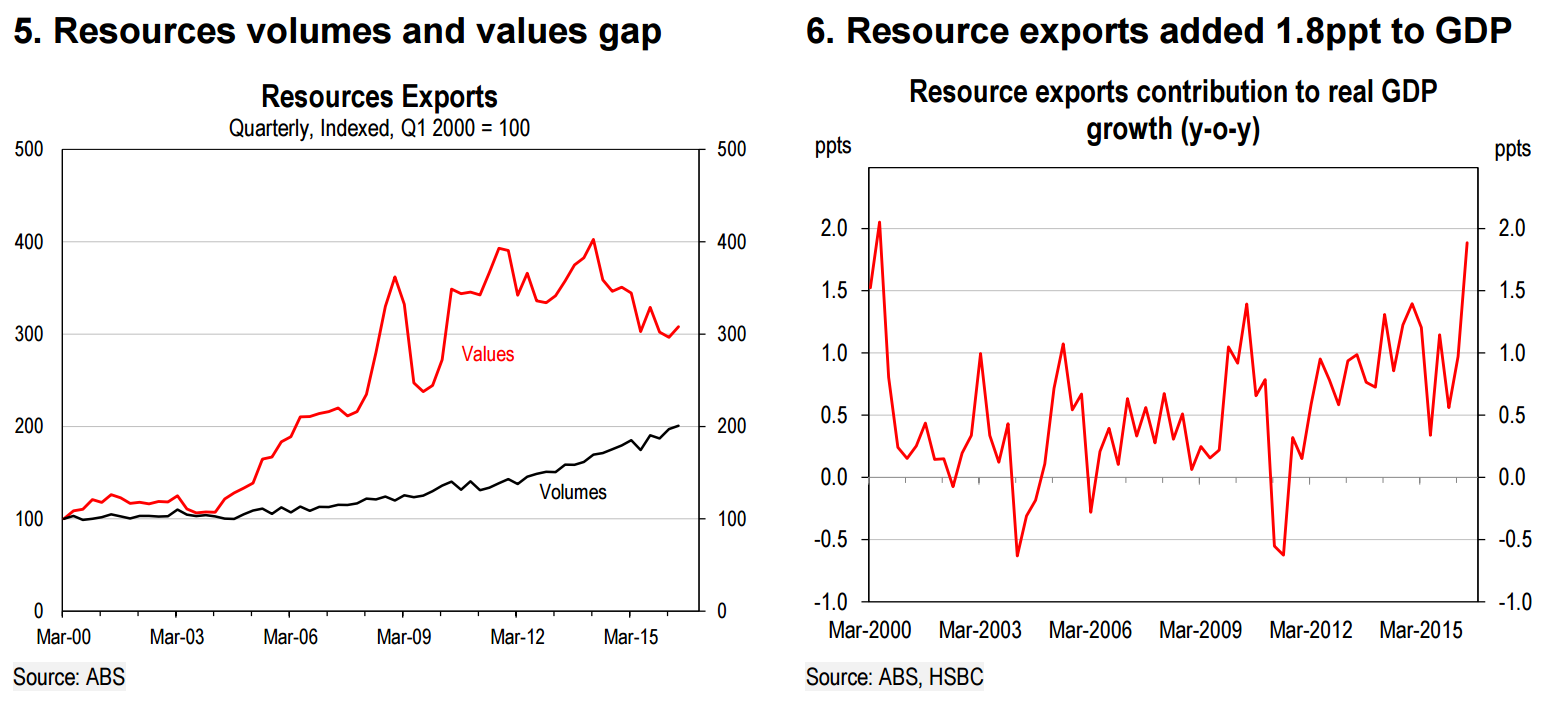

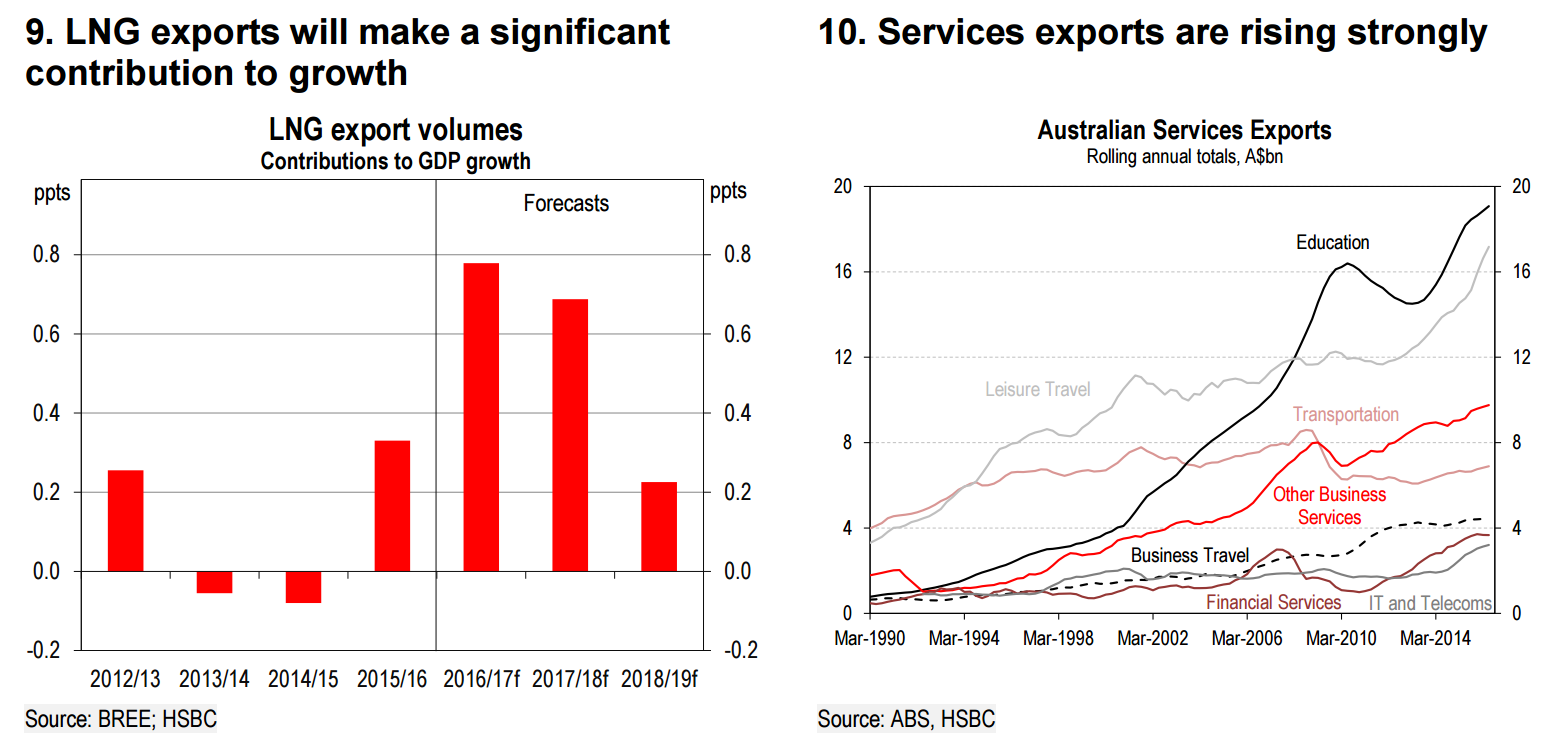

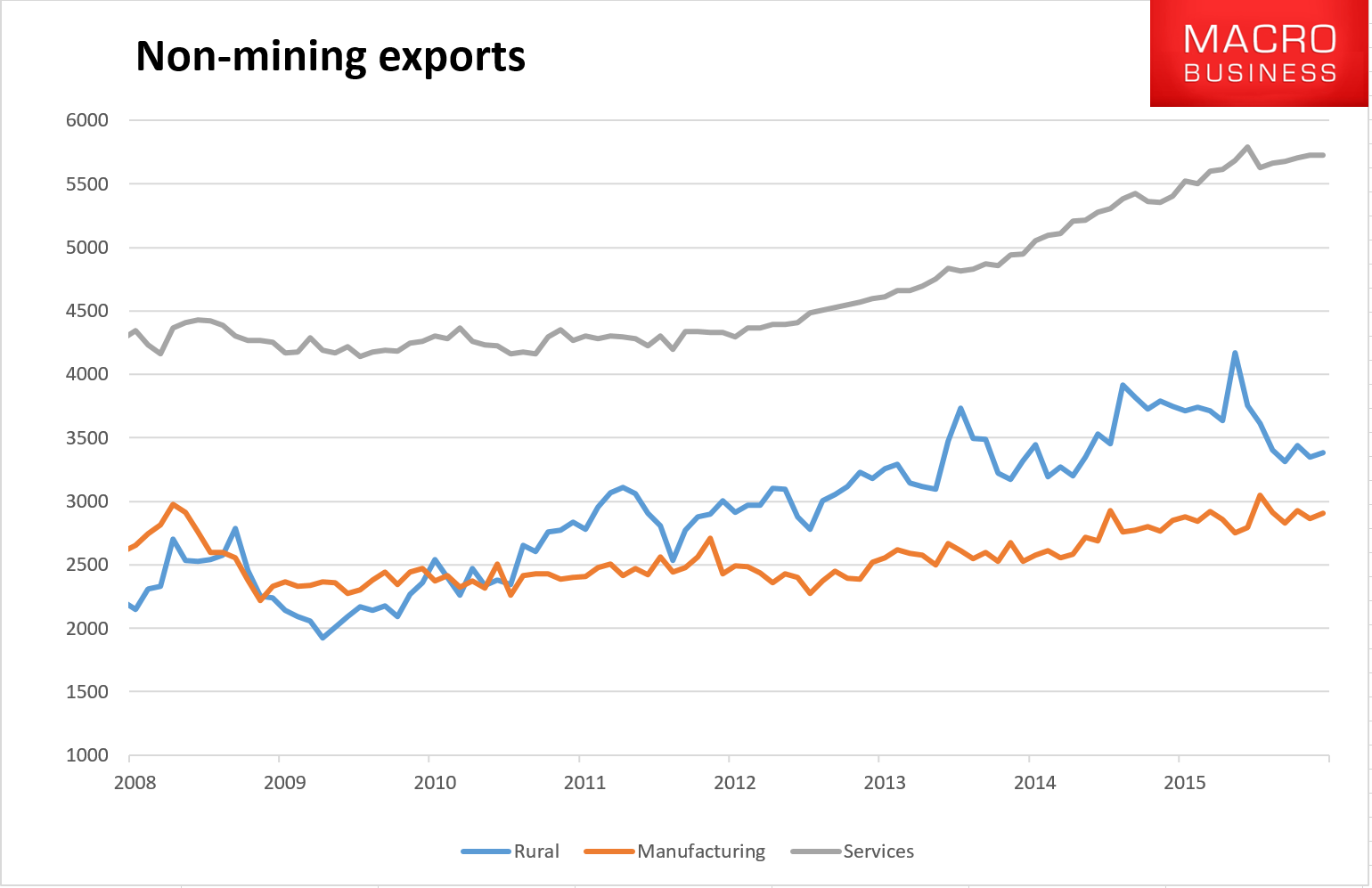

A fall in the AUD and rising middle class incomes in Asia have also supported a significant pick-up in exports of services, including tourism, education, and business services. But there is a rub. At the same time that export volumes have risen, commodity prices have fallen. At the low point, in early 2016, they were down 63% in USD terms. This has weighed on Australia’s exports values, which have averaged growth of just 1.7% a year over the past three years. This has weakened mining company profitability, wages growth, tax revenue, and nominal GDP growth.

However, we think the future looks brighter. We see commodity prices as likely to be past the trough . Given that there is still further capacity to come on-line in the Australian resources sector, including for LNG and iron ore, and we see continued solid growth in services and rural exports, we expect Australian export volume growth of 8.2% in 2017 and 9.1% in 2018.

As we expect commodity prices to be past the trough, this should translate into rising export values, supporting incomes. Australia’s so called ‘income recession’ (to the extent that it had one) should now be in the past. A key risk to this forecast is the outlook for the AUD. The recent lift in the currency has been broadly in line with commodity prices. However, a further lift, or one that saw a larger rise in the AUD than commodity prices, could start to weigh on incomes from USD denominated resource exports or impinge on the competitiveness of Australia’s tourism, education, and business service exports.

It’s all very exciting, I know, except for the facts:

Advertisement

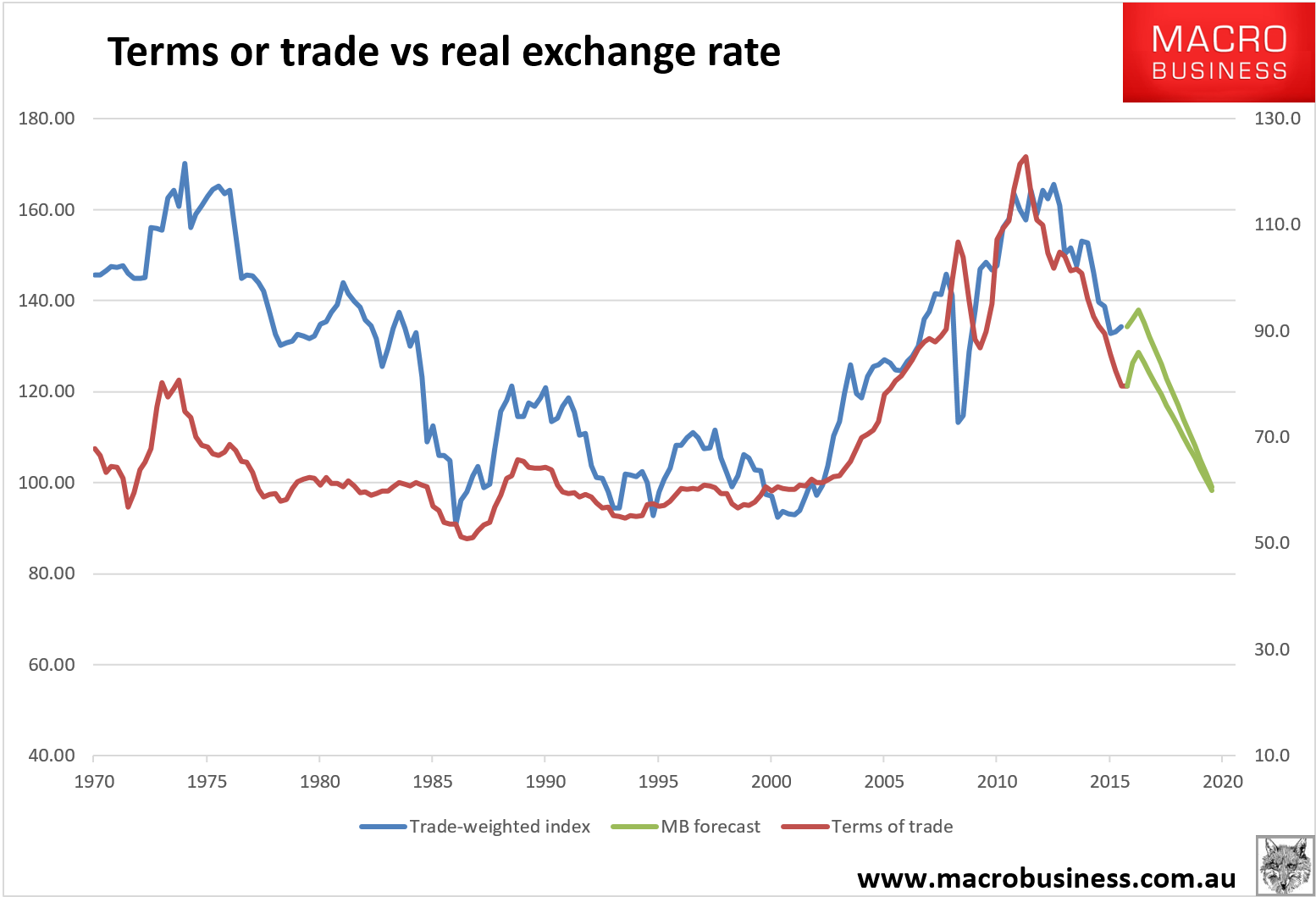

Non-mining export revenues hit a brick wall in the higher dollar in 2016. At best, growth from here is going to be subdued until the currency begins to fall again. The better news is that because the resources rebound will run its course over Q4, the terms of trade will roll over again in H1 ’16 and the Aussie should again come under pressure.

We’ve seen this movie before. Rising volumes result in falling prices and that’s what’s coming in iron ore and the two coals (half of the ToT) and LNG spot prices (though oil and related is basically ToT neutral):

Advertisement

In short:

LNG volumes will add nicely to GDP but less than hoped given capacity will be idled on the global glut;

they hurt income because they are made at losses;

iron ore and coal will add more volume next year then begin to see volume falls, subtracting from GDP by ear end as the junior sector heads for Hades;

H1 will see an income boost from current prices but they will subtract from national income once the peak passes this quarter;

non-mining exports will struggle to grow until the resources rebound rolls.

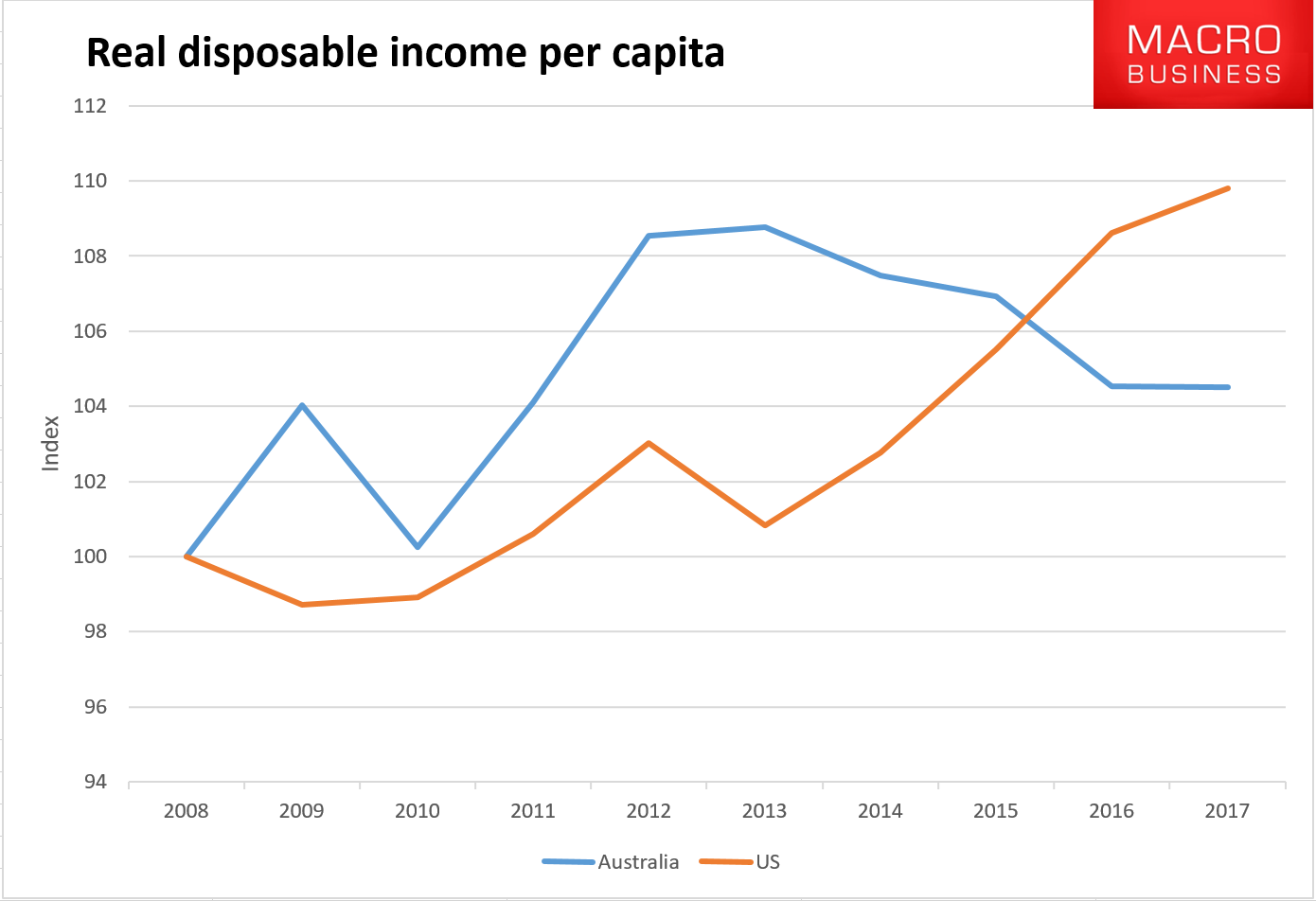

It’s a good story if you think GDP is the be-all and end-all of good economics. But if you think that standards of living are more important than the random whirring of widgets then it’s not quite so heavenly.

And yes, Bloxo, Australia has had an “income recession”, worse, in fact, the US’s Great Recession:

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.