Noise around the US political landscape has taken a turn following Clinton’s recent health scare. Polls now place Trump as an outside chance but no longer the long shot. Clinton has a 75% chance of winning the presidency according to the New York Times forecasting model with the probability of a Trump win at only 23%. Averaging national polls puts Clinton at 45% and Trump at 43% (source: NY Times). Given the relative calm that has enveloped the presidential election, in large part corresponding with the decline in Trumps approval ratings, a Republican victory would come against consensus expectations and would certainly emerge as a shock to current market thinking. While political uncertainty will increase as we move closer to the November 8th election date, the direct and/or indirect consequences for Australia and/or Australian USD earners, outside a landslide victory to Trump, should be relatively minor. Not only because we see limited scope for radical change, but also because outside of an economic downturn that drives a legislated largesse fiscal response, the impacts are probably more indirect than direct—FX and trade policy-related.

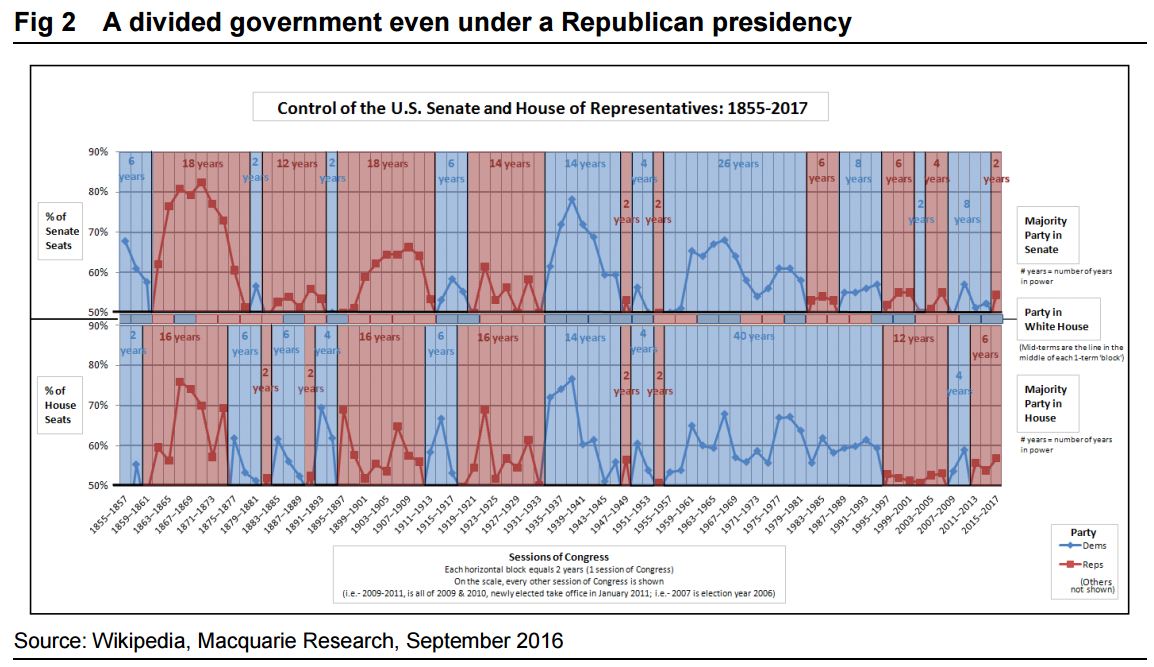

Over the past 3 months we have seen some ‘softening’ in policy rhetoric from Trump (particularly related to immigration), but both candidates can be considered a shift from the current political consensus of austerity and globalization. While there is headline risk around a Trump victory, it is unlikely that either candidate will be able to drastically change the landscape either politically or economically over the near term—nothing much more than incrementalism. Questions have been raised around Trumps impact on the Republican led Senate, but polls currently suggest Republicans have a sufficient lead to hold both the upper and lower houses. This suggests that under anything but a landslide victory to Hillary, it is likely that the Democrats will have to deal with majority led House and Senate. On the other hand, even under a landslide Trump victory, his proposals have been divisive enough to polarise support throughout his own party. A Republican or Democrat led White house will be set against a divided US government, which will potentially make speedy and/or substantial changes in policy direction difficult to implement. All told, there are commonalities across each candidates that will be played out in fiscal programs, trade policy and to a lesser extent, monetary policy indirectly through the Fed Chair. Both appear intent on ramping up fiscal spending via infrastructure; both candidates have expressed concern at current trade policies (including NAFTA) with an intention of renegotiating/scaling back participation. Paths diverge on income tax, where Trump proposes reductions and Clinton favours increases; Healthcare (the Republicans have campaigned to repeal the Affordable Care Act) and Trump has expressed a significantly more aggressive stance on immigration. Policy proposals around gun control, abortion and climate change are also areas of divergence, but not likely to be significant in their influence on Australia and/or USD earners.

Trade & Immigration – De-globalization didn’t start with Trump and it won’t end with Hillary…

Whether it be trade (goods and services), the movement of people or in the free exchange of information and financial flows, there is rising political pressure to protect citizenry and to increasingly counter the trend of globalization. Any number of metrics can be used to support declining benefits— rising income inequality, increase in non-tariff-based trade protection measures, shrinking supply chains, deteriorating demographics and declining productivity, to name a few.

The reality is that a deterioration in the underlying drivers of globalization have been underway for some time. The rise of populism is an outcome rather than an aberration and the result will be a further rise in the government state (this is an investable theme that has longevity over the coming decade in our view – TCL the obvious beneficiary but including LCC). On this basis, policies by Trump and Clinton are simply helping swing the pendulum a little faster and farther as they respond to rising suspicion and uncertainty (from the middle class) on the benefits of free markets.

Trump has blamed the US trade deficit (US$748bn in CY15) and the country’s economic problems on an “elite” class that has worshipped globalism over “Americanism”. He blames America’s sharp decline in manufacturing employment since 2000 and the country’s increasing class inequality on political leaders who have embraced free trade. Trump has voiced his desire to pull back from globalisation, but so has Clinton.

Both have proposed a renegotiation of NAFTA and to reject the Trans-Pacific Partnership agreement (TTP), which is currently being considered by the Congress. Trump goes further with other proposed trade policies to include prohibitive tariffs (up to 45%) on Chinese imports to the US until China allows the RMD to freely float and a 35% tariff on Mexican imports that would pay for a wall between the two countries.

For Australia, outside of a policy-induced growth slowdown, the main transmission channel would be via increased US-China trade tensions that potentially place Australia in a vulnerable ‘middle ground’ position, given close ties to both countries. Major Australian exports to the USA include beef, aircraft, meat and alcoholic beverages, which are not at particularly threat of barriers, but it will be shipping access via the South China Sea that could potentially prove an important roadblock for commodity exports.

In the South China Sea, China, the Philippines, Vietnam, and others are in dispute about who owns certain territorial waters and the resources below. As an assertive mediator, Obama has managed to prevent an escalation. While Trump has proposed “…a military island in the middle of the South China Sea”, he has articulated that he wants to reduce America’s military presence in the AsiaPacific region, noting that South Korea is a “very rich country” and the US is not “reimbursed fairly” for the protection it offers.

This could have serious consequences for Australia, given China is already involved in multiple island disputes (with Malaysia, Vietnam, the Philippines, South Korea and Japan), and could pursue its territorial claims more aggressively, which has the potential to interrupt global trade flows, particularly for Australia, given its close proximity and dependence on the South China Sea shipping routes. In addition, if there are growth impacts on China’s export engine, than it will feed into commodity demand.

Potentially the largest and more immediate consequences for Australia via trade proposals will be indirectly via how the US$ is impacted and hence via translation and domestic tourism. While now a non-consensus view, there is some validity to the idea that the combination of immigration and trade policies will push up real wages for low-skilled workers (and in turn boost consumption and aggregate domestic demand as well as lowering spending on imports (weakening demand for foreign currency) and pushing the USD higher.

Another adverse consequence is that while production in the US might increase, the now excess production in China and Mexico would be spread across other economies in the global trading system. This would be through some combination of lower prices (deflation) in China and Mexico, or through currency depreciation which would spread the burden of adjustment.

Australia and New Zealand would be exposed to the deflationary impulse, given that more than 20% of New Zealand’s imports, and almost 25% of Australia’s imports, are sourced from China. The disinflationary impacts are likely to result in further inflation disappointments in the short run, and could potentially dampen recoveries in non-mining (Australia) and non-dairy (New Zealand) activity.

Clean Energy – energy independence the old way

The differences between the Democrat and Republican position on clean energy policies (which include renewable energy subsidies, emissions regulations, fossil fuel subsidies, and climate agreements) are stark.

Trump, a firm advocate for oil (and its overall importance for the US economy), has expressed his intentions to confront OPEC and pursue energy independence for the US by aggressively expanding fossil fuel production. However, it would probably require a tax cut or some form of incentives for oil producers to have a material impact on US production growth. We see little risk that the US will reopen its coal export markets given its high cost and low-quality US thermal and coking coal mines compared to offshore competitors.

A Clinton presidency opposes offshore drilling, the Keystone XL pipeline, and drilling in the Arctic; and instead supportive of Obama’s Clean Power Plan and the Paris Climate agreement . While at face value, it is likely to have a negative impact on large owners of fossil fuel-fired power plants and automakers and upside to solar and wind players, to see this unfold we would need to see a blanket ban, which we think is unlikely. In fact, given that her exact measures and support for renewable energy companies still remain unclear, a Clinton presidency could have a more muted effect on these businesses.

Sounds roughly right to me. The major short term outcome of a Trump victory is a higher US dollar as protectionism, fiscal stimulus and geopolitical tensions all rise. Those pressures are only lessened not removed by Hillary Clinton.

The major long term impact is to very seriously undermine Australia’s “citizenship exports” growth model as “Americanism” demands more from allies and the anti-globlisation movement is pushed into political orthodoxy, legitimising all kinds of resistance to population growth currently thought of as “crack pot”.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.