The good news for Australia is that headwinds from the mining bust may be moderating. The bad news is that tailwinds from the housing boom may fade. Nominal domestic growth looks set to remain weak, and recession remains a tail risk for 2017.

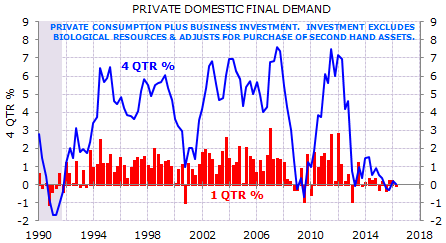

Australia’s private sector has been flattened by the mining boom busting. Real private domestic demand stalled as falling terms of trade cut income and mining investment collapsed (Exhibit 1).

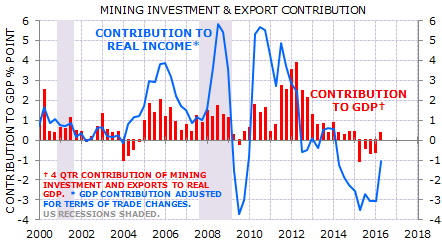

The flat-lining private sector reflects the netting out of two divergent trends. The mining bust has been the major headwind. Mining has been a modest drag on real GDP, but GDP is a misleading metric. The big story is the mining drag on income, reflecting the fall in commodity prices (Exhibit 2).

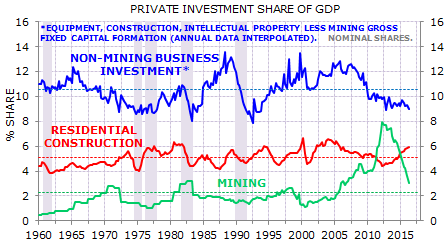

June quarter national accounts data hinted that the drag from mining may be over. This seems too optimistic: more likely the drag will continue, but moderate. First, mining investment is likely to continue to decline. Investment spending remains above-average as a share of GDP, while the trough is in my view likely to be below average (Exhibit 3).

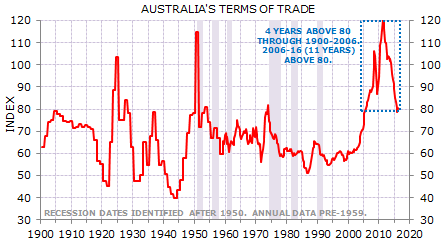

Second – and more importantly – the terms of trade likely have further to fall. It would be remarkable if the terms of trade bottom at a level exceeded only four times in the 105 years to 2005 (Exhibit 4).

More to the point, it would be remarkable if the supply-side expansion in key commodities, such as iron ore, is at an end with profit margins so high.

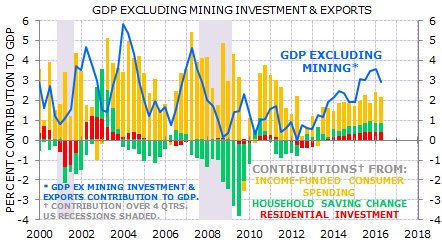

The amazing turn in mining-related income – a 9 percentage point swing from the 2010 peak to the 2015 trough – has been partly offset by a lift in non-mining activity. I have under-estimated this offset – in particular the broad effect of housing on activity. This includes not only the direct contribution from residential investment, but also wealth effects: household saving fell as house prices rose. In aggregate, this explains much of the lift in non-mining activity from the 2013 low (Exhibit 5).

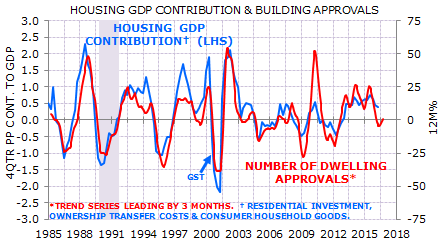

The forward-looking point is that there are signs that housing-related growth may moderate, just as there are signs that the mining drag may moderate. Dwelling approvals suggest that the direct housing contribution to growth will stall in 2017 (Exhibit 6).

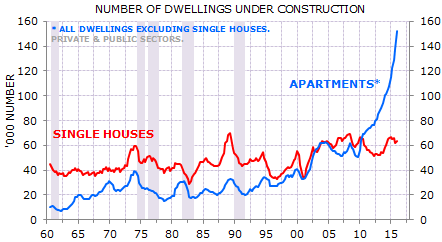

It’s likely that pockets of the housing market will see a hard landing. Prices are falling in mining states: prices in Perth are down 10½% from peak; they are down 14% in Darwin. Rents are down 16¼% in Perth and down 23½% in Darwin. It also seems fairly clear there will be sharp declines in inner-city apartments in Melbourne and Brisbane, and perhaps Sydney. There is an unprecedented pipeline of apartment construction (Exhibit 7). However, it remains the case that broad-based job losses remain the most likely cause of widespread house price declines. While that is a risk for 2017, it’s not my base-case.

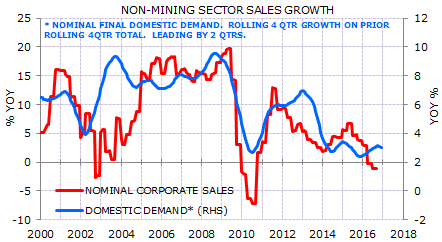

In short, Australia is a likely to start a rebalancing of sorts – one where mining remains a drag on national income, but a shrinking one, while housing-related activity remains a support, but a fading one. This is a mix where domestic corporates will continue to face anaemic top-line growth (Exhibit 8), which will keep labour income in check.

In short, the base case remains more of the same heading into 2017. This is a setting where the RBA will likely retain an easing bias, particularly if the hunt for global yield keeps the A$ riding above its usual fundamentals. My view remains that commodity prices have not made their cycle lows, and likewise the A$ ultimately has further to fall.