From UBS, the “shortage” appears to be on thin ice:

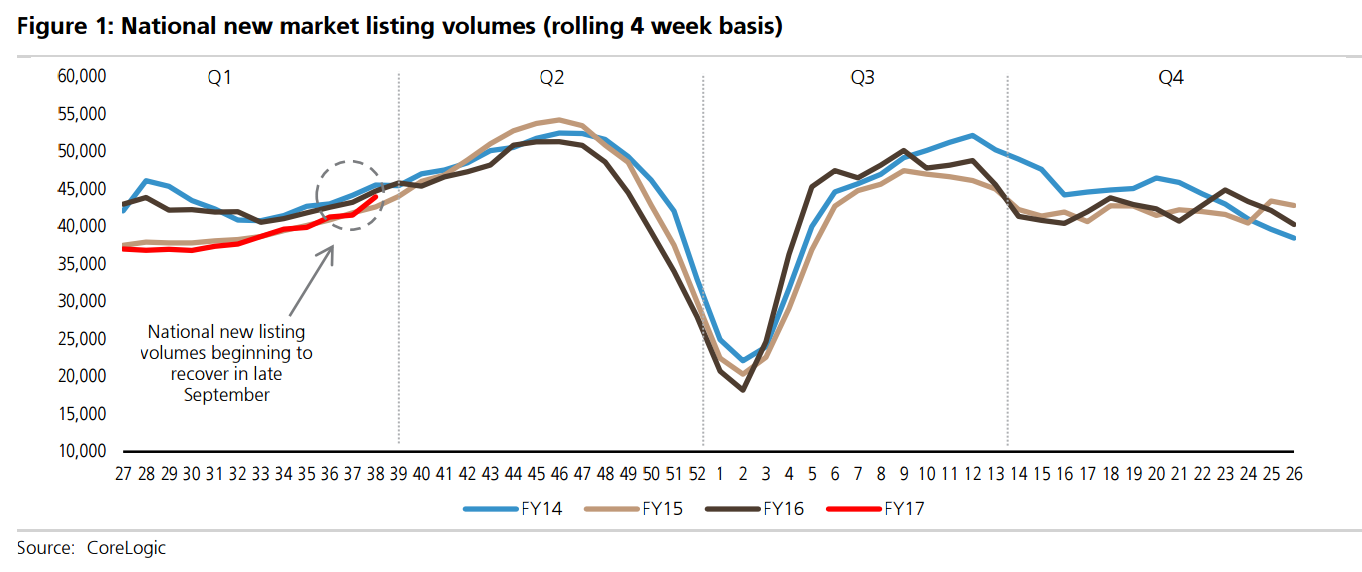

1Q17 new market listing volumes look to be down -5% yoy After a weak July (volumes -11% yoy) and August (-5% yoy), national new listing volumes appear to have stabilised in September. For the four weeks to 25-Sep-16, national volumes are now only down -0.4% yoy. The flat national result is however being driven by stronger regional markets, as capital city listing growth remains negative. New listings for the capital cities combined were down -14% yoy in July, -7% yoy in August, and -3% yoy for the 4 weeks to 25-Sep-16. Sydney and Melbourne in particular are both still weak: down -18% yoy and -2% yoy respectively at 25-Sep-16. New listing volumes for Brisbane (+6% yoy), Adelaide (-0.1% yoy), and Perth (+16.4%) are however faring well.

Next catalysts: REA 1Q17 and FXJ AGM update both due in early November A -5% yoy decline in new listing volumes should result in a soft 1Q17 for both REA and Domain. However we are beginning to see signs of a recovery in the back end of September. As a reminder CoreLogic data is provided on a rolling four-week basis. Volumes were down -3.9% yoy for the four weeks to 11-Sep-16, but flat (-0.4% yoy) for the four weeks to 25-Sep-16. This suggests national new listing volumes have rebounded to positive growth in the last two weeks of September, which could bode positively for Oct / 2Q17 volumes. Given September is also a seasonally strong month, REA’s 2Q result may also benefit from revenue deferrals from the back end of 1Q.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.