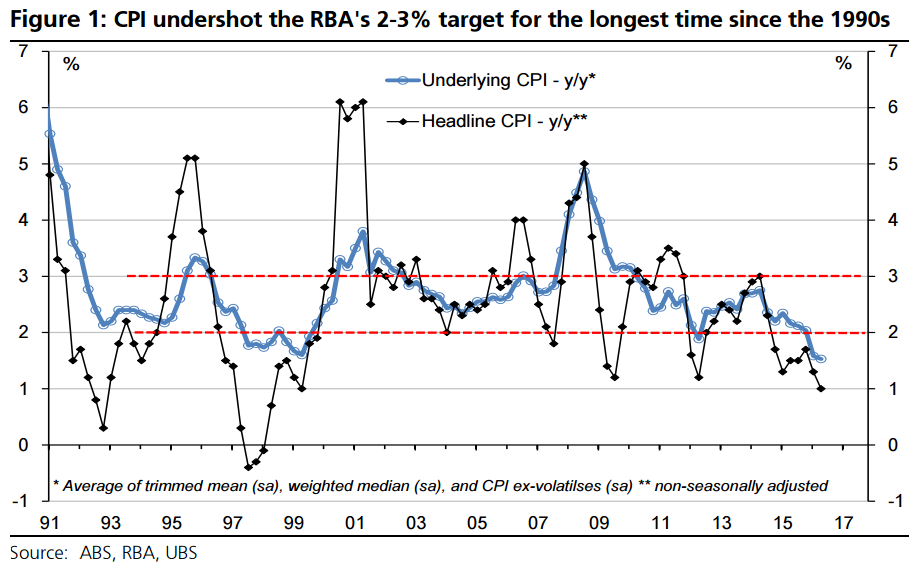

RBA ‘change at the top’ may lead to more target flexibility & focus on stability The RBA is undergoing material ‘change at the top’. As expected, the decade-long reign of Glenn Stevens ended in retirement, & long-serving deputy Philip Lowe was appointed Governor. With a change of Governor (or Treasurer), the RBA & Government update the Statement on the Conduct of Monetary Policy. Importantly, in this version there were two subtle, but material, changes to the “objectives of monetary policy”. Notably, the numeric goal of policy was reiterated as “CPI between 2 and 3 per cent, on average”. Firstly however, the previous Statement that referenced the target as “over the cycle” was replaced with “over time”, & now also emphasises a more flexible “medium-term” inflation target. While Lowe’s testimony to parliament downplayed the change by arguing “a flexible medium-term inflation target remains the right monetary policy framework”, & they have not been “inflation nutters”, we think it still implies a greater tolerance of below-target CPI, without leading to a rate cut…i.e. a hawkish tilt. While CPI has undershot the target for ~2 years, the longest period since the 1990s (Figure 1) – & the RBA forecasts it remain below, or at the bottom, of the target until 2018 – it may not indicate as much chance of easing as in the past. (Arguably, the RBA may also be slower to hike than ‘normal’, even if CPI eventually returns to the target.) The second change to the objectives of monetary policy was the elevation of the importance of financial stability. Specifically, the ‘medium-term’ inflation target “provides the flexibility …to set its policy…to achieve its broad objectives, including financial stability” [emphasis added]. Indeed, Lowe’s testimony noted the main change in the Statement was “to make the link between monetary policy & financial stability a little more direct;” although Lowe added that “yet, over the years, financial stability considerations have been a factor in our monetary policy.” Lowe also noted that “a very quick return of inflation” to target “at the cost of a material deterioration in the health of private sector balance sheets was unlikely to be in the public interest” We note this comes after total debt-GDP already spiked to a record high of ~255% in Q2-16, led by the private sector up to 208% (Figure 2).

We see this change as aligning with Lowe’s recent speech which pondered giving more weight to the importance of financial stability in monetary policy. Specifically, Lowe questioned “how policy should respond to a systematic weakening of balance sheets.”…and highlighted the (BIS) hypothesis that “the build-up of financial imbalances may be a better guide to the sustainability of growth in the economy than is the current rate of inflation [emphasis added]. Clearly, this hypothesis needs to be tested. If it were found to be valid, it would have implications for policymakers in a number of spheres, including monetary policy, prudential policy and even fiscal policy”.

Indeed, these two shifts in the RBA’s policy thinking1 are broadly consistent with BIS working papers that Lowe authored way back in 2002 and 20042 which argued for 1) a longer horizon for the inflation target & 2) elevating financial stability. Specifically, Lowe’s research “argued that in order to ensure price stability in a sustainable way two modifications to prevailing monetary frameworks might be desirable. First, central banks should consider articulating the pursuit of their price stability objectives over longer horizons than the one- to two-year ones normally associated with inflation targeting strategies. Second, they should consider paying greater explicit attention to the balance of risks to the economic outlook, as conditioned by the presence or absence of financial imbalances. In our view, these modifications could help establish the technical framework allowing central banks to lean against the build-up of financial imbalances, if and when they arise, even if near-term inflation prospects remain subdued [emphasis added]. This would help to limit the consequences of their unwinding on output and inflation further down the road, beyond normal policy horizons. Such an unwinding could result in serious economic weakness, in extreme cases in financial instability and, when taking place against a backdrop of low inflation, it could lead to unwelcome disinflationary pressures”.

Overall, we think these changes provide some support to our view that the RBA is a ‘reluctant cutter’, and hence we expect the RBA to keep the cash rate on hold until at least end-2017. It also suggests that if we were to be wrong, and the RBA ended up cutting the cash rate again, then the prospect that any easing would be coupled by additional macro-prudential tightening has probably increased. For example, the RBA (in conjunction with APRA) could lower the existing investor housing credit ‘cap’ of 10% y/y. However, APRA Chairman Wayne Byers recently noted “I could lower the cap to 7%, but I don’t know what difference that really makes” – given growth already more than halved to a 7-year low <5% y/y (Figure 3 – for background see credit cycle constraining RBNZ more than the RBA).

All true. Problem is, he will be forced to cut as the economy refuses to lift:

commodity prices resume their falls next year and so does the terms of trade;

the stall in national housing markets (albeit with fog over Sydney and Melbourne) weighs heavily on consumption growth;

the rollover in the dwelling construction boom, mining capex cliff and departure of the car industry will hold investment and the labour market back;

when the mining capex cliff ends so will the net exports uplift meaning GDP will be purely domestic demand dependent. It will be weak with households and investment sluggish offset by not enough fiscal stimulus;

ongoing Budget pain will prevent much more infrastructure roll out;

the population ponzi is also under increasingly fatal pressure though it is difficult to say when it will break;

if there is some minor renewed pulse in wages and inflation and rates are held then, in an oversupplied world, the dollar will rise to snuff it out, and

we’ll see some kind of external shock sooner rather than later.

Our Phil will be cutting again before long. My guess is we’ll see more easing in the first half of next year but timing these days is a mug’s game given bubble management is a much more subjective exercise than were the strictures of traditional price stability.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.