From Macquarie:

Our China economist Larry Hu has published a preview of China’s September and Q3 macro data, which will be released on October 19. Thanks to the property market and price reflation, we believe the economy continues to improve. For September, industrial production (IP) growth could be stable at around 6.3% YoY. We expect real GDP to grow 6.7% YoY in 3Q16, the same as in the previous two quarters. But nominal GDP growth, which improved to 7.2% YoY in 1H16 from 6.4% in 2015, is set to pick up further in 2H16. As such, monetary policy will likely stay put, and the focus of policy makers is now on the property market, where Larry notes that this round of property upcycle is hardly a national phenomenon. In the past 12 months, 48 out of the 70 biggest cities had home price growth lower than 5%. As such, tightening monetary policy at the national level doesn’t make sense either. Instead, Beijing will rely more on local governments to curb any property frenzy within their own territories.

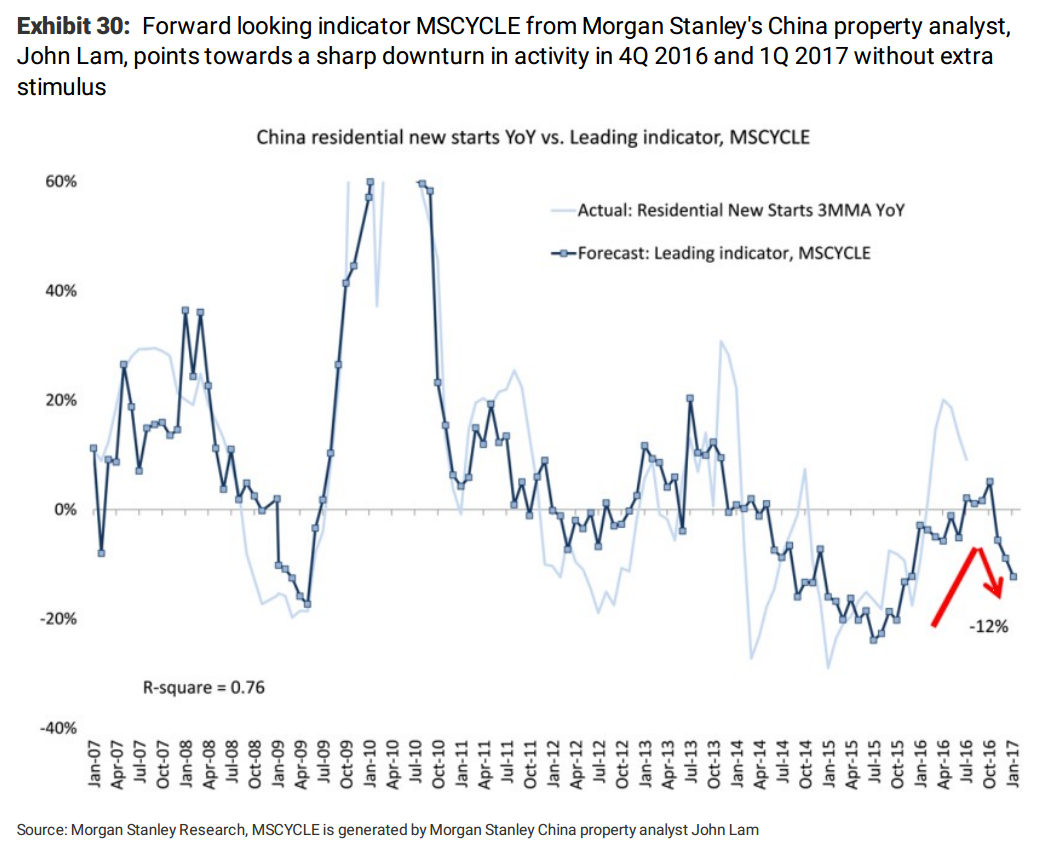

Yep. But I expect the prudential tightening to have an out-sized impact on construction activity because it is tracking prices largely in the first and second tier cities which are the much lower construction volume districts. We can see this already in Morgan Stanley’s leading indicator: