We are witnessing the start of a fundamental change in the economics of employing people in Australia. Already some of our biggest employers, such as Woolworths, Coles, McDonald’s, KFC, Bunnings, Big W, Hungry Jack’s, Kmart, Target and United Petroleum are in the front line of the revolution.

The fundamental shift looks set to change the economics of labour-intensive industries like retailing as the flow-on effects hit profit and pricing levels. Just how far the wage bills will rise is impossible to determine at this stage, but unless the shift allowance and penalty rates are changed, the cost increase will range between five and 20 per cent of wage bills. And if back pay is ordered then payments might involve billions.

With due respect, bullshit:

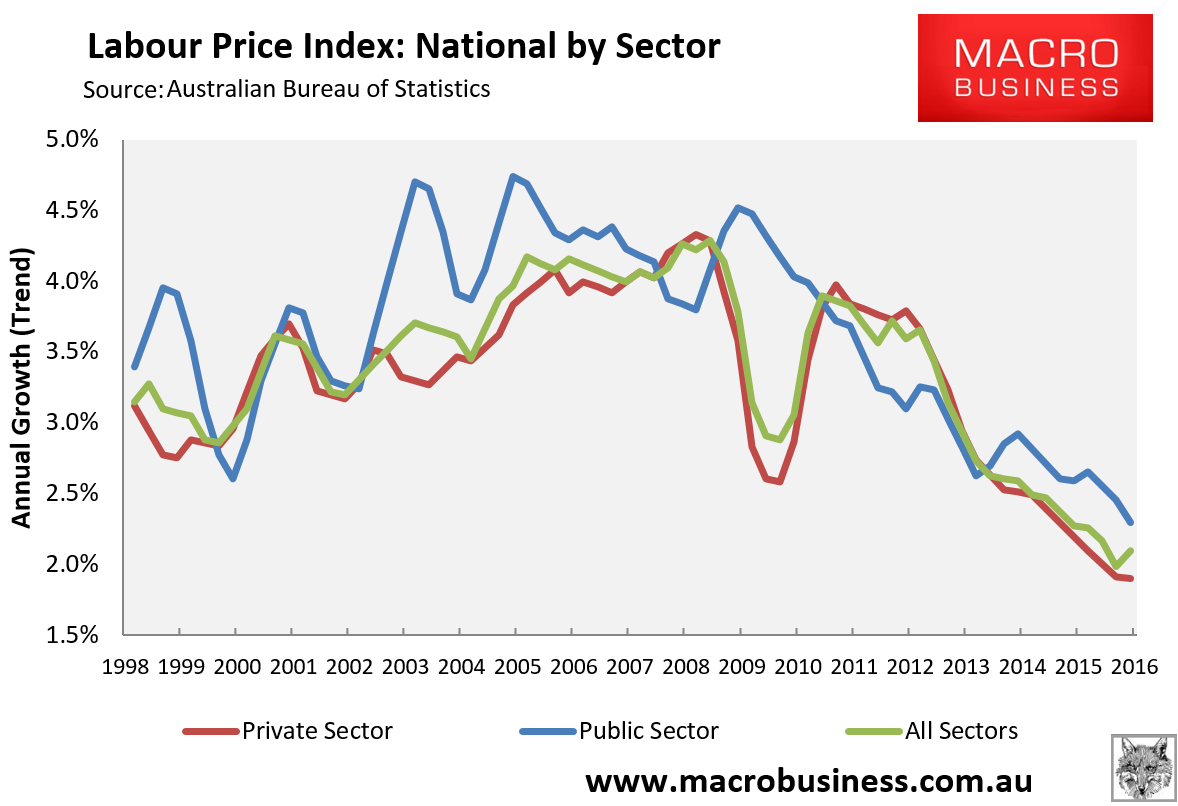

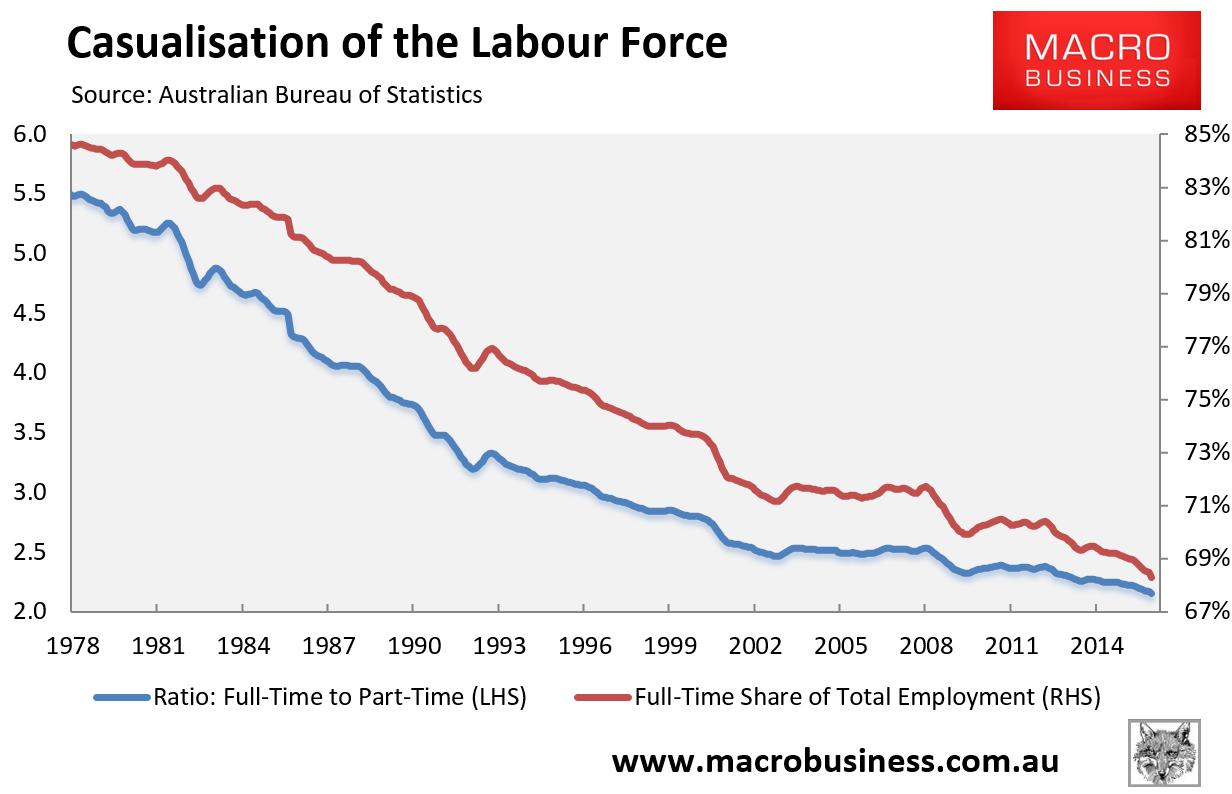

And the primary driver is a move to part time work:

Advertisement

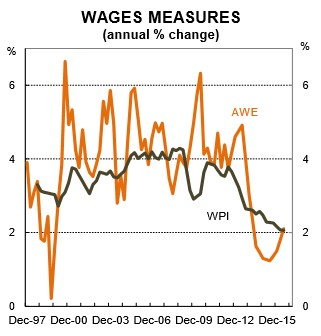

Which even CBA admits means less pay rises:

As a general rule, economists and policymakers should welcome part-time employment growth when it reflects the desires of employees… As a society, a shift towards part-time employment is a positive development if that reflects the desires of the population… The well-being of society should come above the pursuit of economic growth – if a shift to part-time employment is part of raising welfare then it should be embraced.

However, growth in part-time employment, rather than full-time work, becomes a problem (and indeed undesirable) when there is growth in the number of workers who are not working as much as they would like. This is captured in the underemployment rate. Unfortunately, the underemployment rate has been rising in Australia and it remains near its highest level on record. This indicates that a growing proportion of people are employed, but they are not working as much as they would like.

The sum of the unemployment rate and the underemployment rate produces the underutilisation rate which is the broadest measure of spare capacity in the labour market – it is high and presently sits above the level hit during the Global Financial Crisis. This means that the economy is operating below its capacity and there is an output gap. This has had implications for wages and inflation…

In our view, a material lift in investment (business or public) is likely to be the precursor to an increase in full-time jobs growth. Generally, a lift in investment is a sign of a genuine lift in current and expected demand. We would expect to see labour demand grow in such circumstances.

In the short term, a lift in private investment looks unlikely…

Whichever wage you slice it, wage growth is weak. The pulse of wage inflation is soft and the compositional changes in the labour market are negatively impacting the mining states (i.e. WA and QLD) in particular…

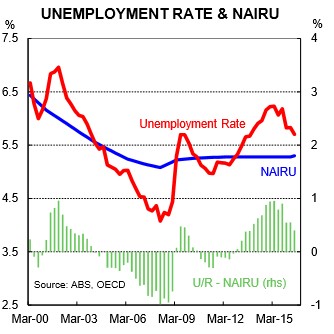

In our view, wages growth is unlikely to lift until the unemployment rate gets closer to the non-accelerating inflation rate of unemployment (NAIRU which is around 5¼%) and the underemployment rate starts moving south. Or to put it more generally, spare capacity in the labour market needs to be gobbled up for wages growth to increase. We are some way off that…

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.