• The Westpac MNI China Consumer Sentiment Indicator recovered in September, rising 3.3% to 115.2 from 111.5 in August. The Indicator is still well below its long run average of 120 but is slightly above the average read over the last 12mths.

• Some of this month’s rise reflects the waning impact of severe weather events. Flooding affected 24 of China’s 36 provinces in July-August, likely contributing to the weak sentiment read in August which was close to previous survey lows.

• All five components improved in September. Consumers’ near term expectations recorded the strongest gains: ‘family finances next 12mths’ up 7.1% and ‘business conditions, next 12mths’ up 4.9%. These two components saw the sharpest falls in August, particularly in China’s North East where flooding was the most severe. Assessments of ‘business conditions, next 5yrs’ recorded a milder 2.6% rise with views on ‘family finances vs a year ago’ up 1.3% and assessments of ‘time to buy a major item’ up just 0.7%. Notably, all components remain materially below their long run averages.

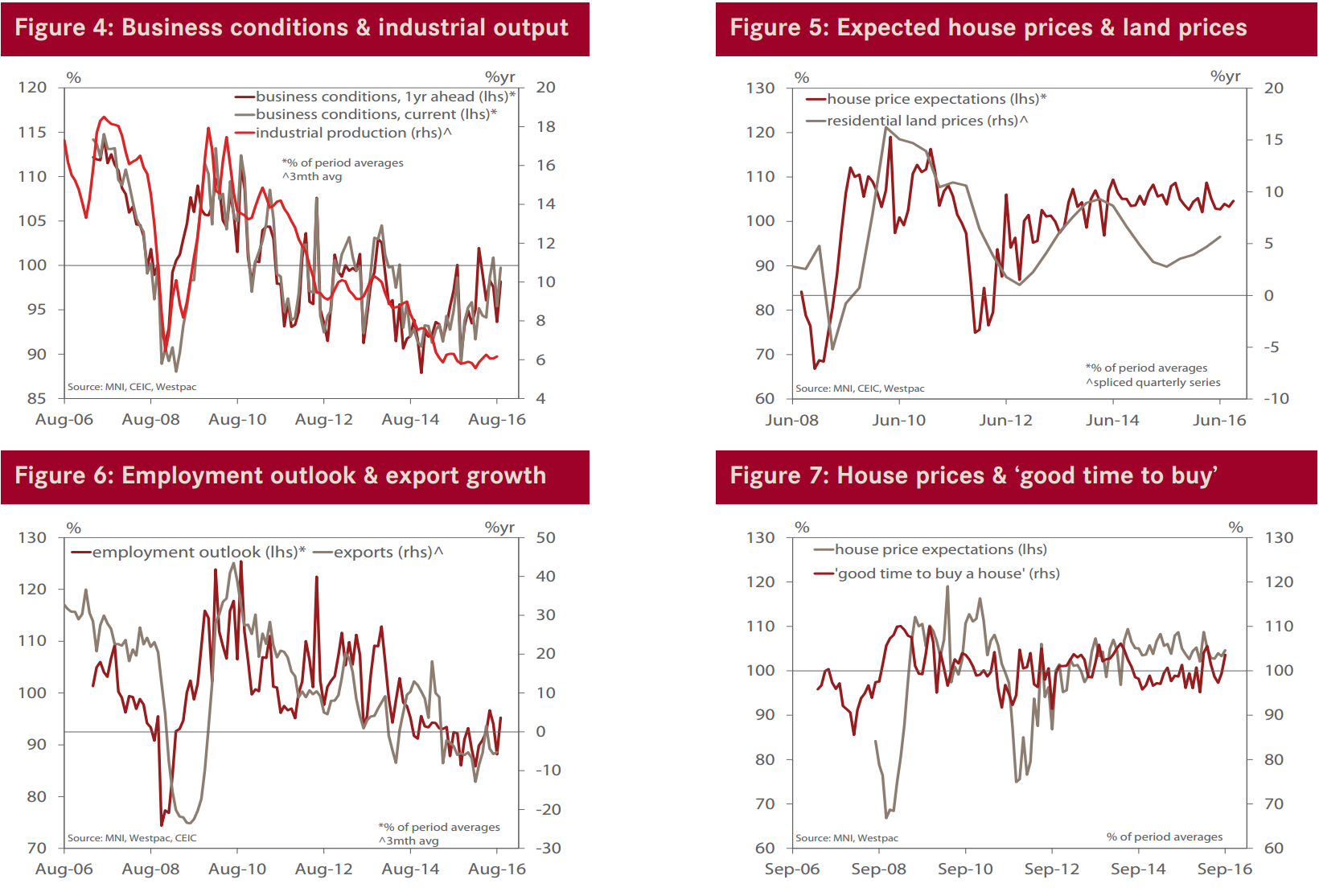

• Chinese consumers also marked up their assessment of current business conditions: the ‘business conditions vs a year ago’ index up 4.6% and basically in line with long run average reads (note that this index is not part of the headline composite but is highly correlated with the other measures of industrial activity). Job security recorded a particularly strong rebound, the employment indicator surging 8.0% more than reversing last month’s 7.4% drop.

• Consumer attitudes towards real estate have been more stable in recent months and firmed again in September, the housing composite rising 1.5% to be nearly 3% above its long run average. Consumers reported solid gains in house price expectations (+1.3%) and assessments of ‘time to buy’ (4.2%) both hitting five month highs. More consumers reported ‘house purchase’ as their primary ‘motivation for saving’ (10.9% up from 8.6% in August) although the proportion nominating real estate as the ‘wisest place for savings’ slipped back.

• Consumers’ purchasing plans also improved although here the gains were more muted and uneven – expected spending on ‘shopping’ posted a solid rise but plans for ‘discretionary’ spending on entertainment declined and on ‘dining out’ were up only slightly . Perceived buying conditions mostly improved but in most cases were still below June levels – autos were a notable exception. • This month’s rebound in confidence is clearly a welcome development, particularly after the sharp slide in JuneAugust. However, even with a recovery, sentiment is still at a low level overall and yet to establish a convincing recovery. The September rise is a step in the right direction and the improvement in labour market expectations is an important positive but much of the detail, around spending and saving behaviour in particular, points to more lacklustre growth for consumer sectors near term.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.

• The Westpac MNI China Consumer Sentiment Indicator recovered in September, rising 3.3% to 115.2 from 111.5 in August. The Indicator is still well below its long run average of 120 but is slightly above the average read over the last 12mths.