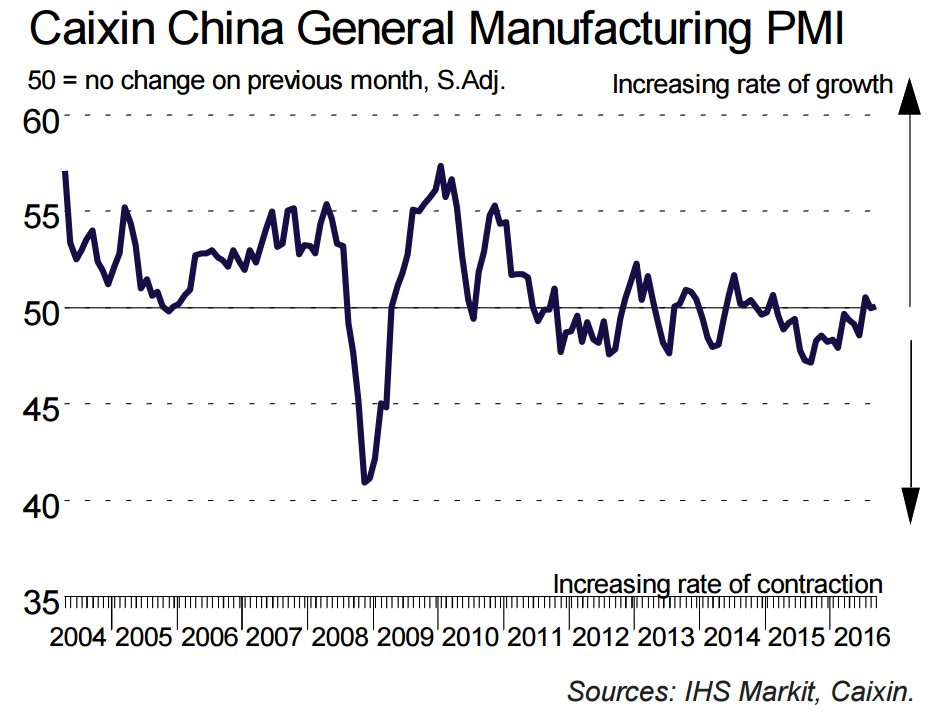

Having stagnated in August, Chinese manufacturers signalled little-change to overall operating conditions during September. On a positive note, output and total new orders continued to expand, albeit marginally, while firms raised their purchasing activity for the third month in a row. However, cost-cutting initiatives contributed to a further marked reduction in employment. As a result, companies signalled a sustained squeeze on operating capacity as highlighted by a further increase in the amount of outstanding business. Inflationary pressures appeared to intensify during September, with both input costs and output charges rising at quicker rates than in August.

The seasonally adjusted Purchasing Managers’ Index™ (PMI™) – a composite indicator designed to provide a single-figure snapshot of operating conditions in the manufacturing economy – rose only slightly from the no-change mark of 50.0 in August to 50.1 in September. Although this signalled only a fractional improvement in the health of the sector, it was only the second time the headline index had posted in positive territory since February 2015.

Chinese manufacturers continued to signal growth in new work during September. The rate of expansion remained marginal, however, despite quickening slightly from the previous month. Encouragingly, new business from abroad was broadly stable in September, which ended a nine-month sequence of reduction. While some firms mentioned that underlying client demand had improved, others mentioned that subdued market conditions had weighed on overall growth in new orders. As a result, companies took a more cautious approach to production, as highlighted by the slowest increase in output for three months.

Manufacturing employment in China continued its downward trend in September. Though the rate of job shedding weakened to its slowest in nine months, it remained marked overall. According to respondents, cost-cutting policies and efforts to boost efficiency led companies to cut their headcounts. However, lower workforce numbers and growth in new work added further to pressure on operating capacity. This was highlighted by sustained growth in backlogs of work, with the rate of accumulation the second-fastest since December 2014.

Purchasing activity increased in September, though the rate of growth was little-changed from August and modest overall. Consequently, stocks of purchased items rose slightly over the month. At the same time, relatively muted growth in new work contributed to a further accumulation of inventories of finished goods.

Stock shortages and adverse weather conditions contributed to a slight deterioration in vendor performance in September, after it was broadly stable in August.

Average cost burdens rose for the third month in a row during September and at a solid pace. As part of attempts to pass on higher input costs to clients, manufacturers raised their factory gate charges at a quicker pace than in the previous month.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.