According to the AFR it is:

It wasn’t quite the soother the Reserve Bank needed. News that the economy grew at its fastest pace in four years in the second quarter of this year would normally be well received by the RBA.

But right now any good news on the local economy could send the Australian dollar higher, and that is not what the central bank wants….The talk on trading desks would be along the lines that if the economy is doing well, why cut rates?

And if there’s not going to be any more rate cuts then the $A can start to rally again.

I don’t think so. Even though I do think the window for Fed hikes this year has now closed. The currency does not just rely on the Fed, after all. There are many drivers, five of them in our view, so let’s check them all out:

MB’s five driver model for the Aussie is:

- global and Australian growth (or, more recently, Chinese growth and Australia’s terms of trade);

- interest rate differentials;

- investor sentiment and technicals; and

- the US dollar.

For the first, Australian growth has been relatively strong in GDP terms over the past year, certainly in terms of relative performance with other developed economies, so that’s supportive. However, the risks for the next year still tilted towards below trend growth as the triple capex hit of mining, residential construction and car industry combines. Fiscal support will help but net exports will fade and the consumer remain muted.

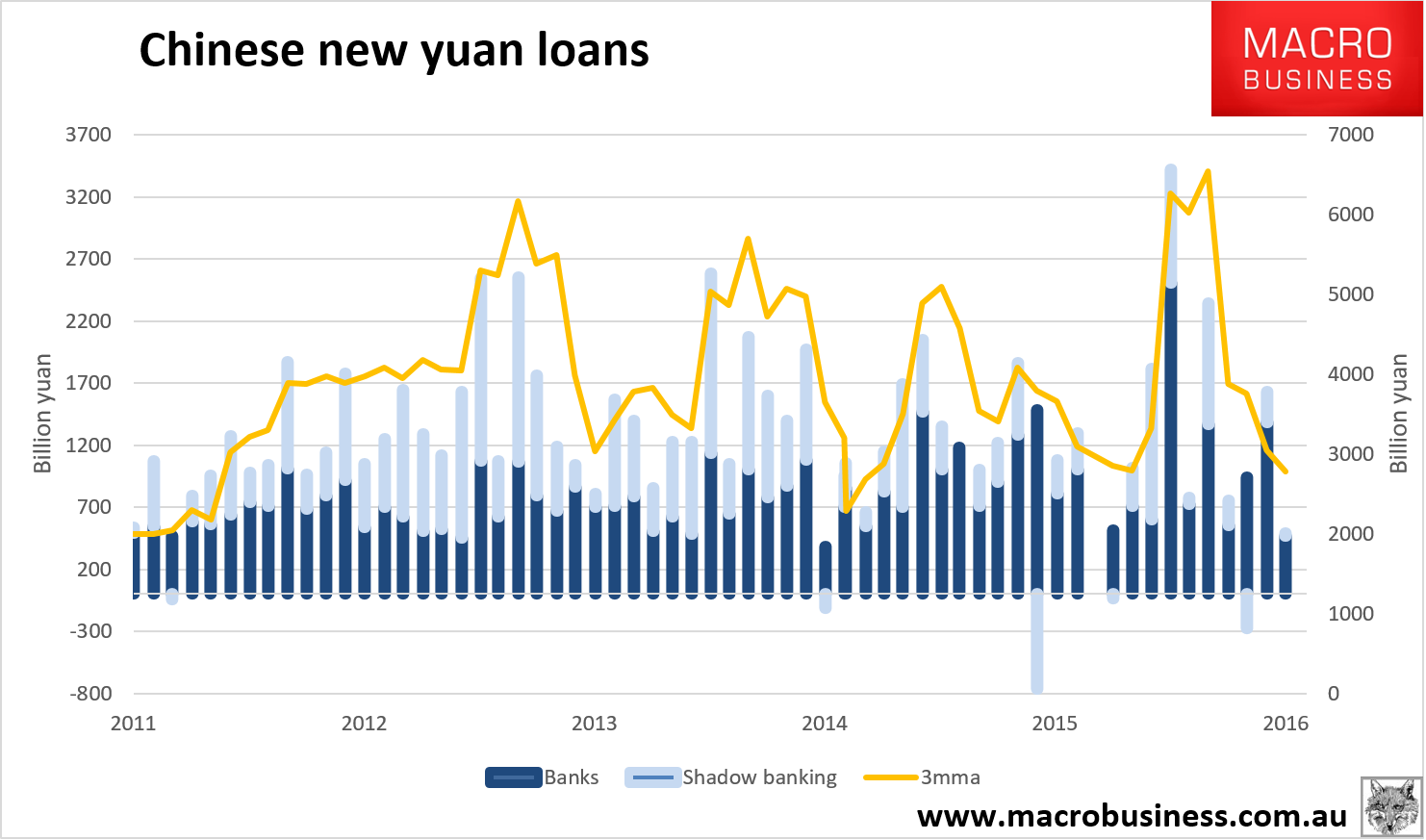

As well, and perhaps even more importantly, Chinese growth is poised to slow materially into Q4 and Q1 next year. Its stimulus credit pulse ended in May and it usually has a tail of six months or so:

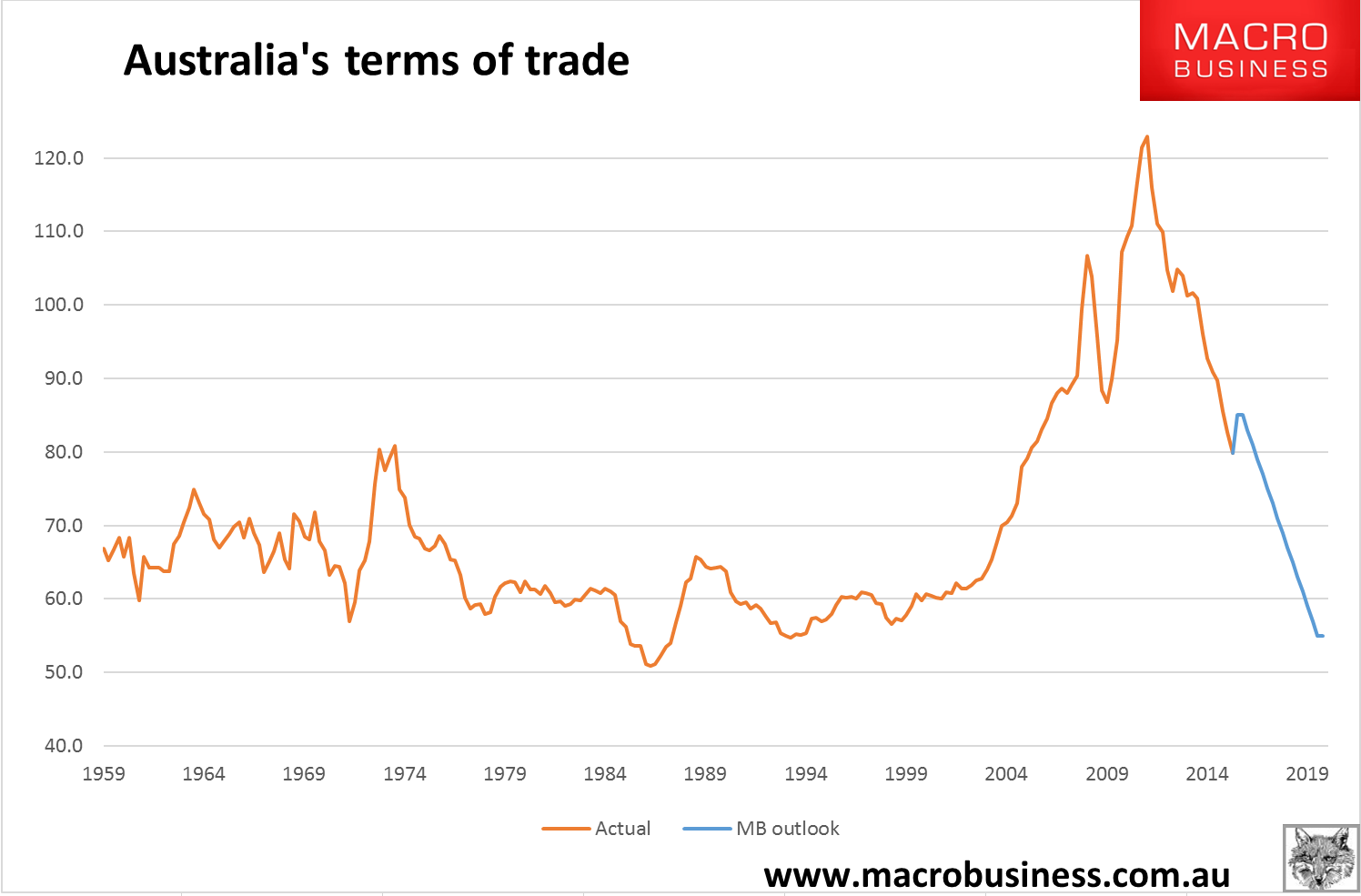

Thus the temporary lift to Australia’s terms of trade we’ve seen this year will begin to reverse:

How quickly the draw down transpires depends upon the pace of Chinese slowing. We expect an incremental slope not sudden drop as fiscal support is sustained but the chances of another kick of the credit can have swung into the negative in recent weeks as China’s reform rhetoric has returned. Australia’s three main commodities of iron ore, coking coal and thermal coal should all come under pressure for much of next year. I am also of the view that oil will fall into year end as it enters its seasonally weakest period and supply remains too strong.

In conclusion, expect driver one to weigh on the currency through Q4 and for much of 2017.

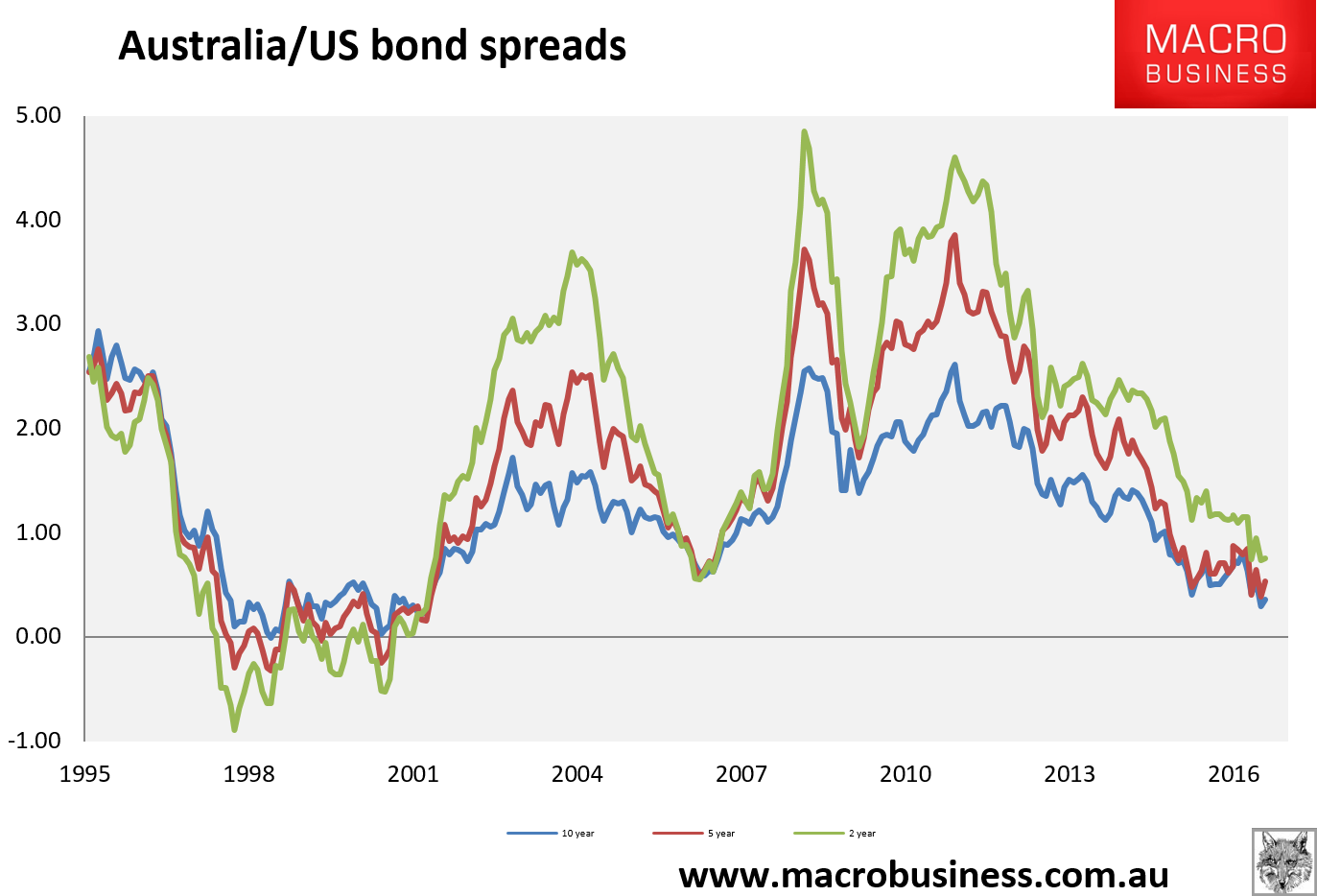

Driver two, interest rate differentials, has swung a little the other way. With the Fed likely paused for now there is no spread compression coming from the US. Moreover, Australia’s solid GDP performance, slightly firmer price pressures and doubts over the direction of the housing market will likely now have the RBA on hold through the end of the year. The US/Australia spread has thus stopped falling for now:

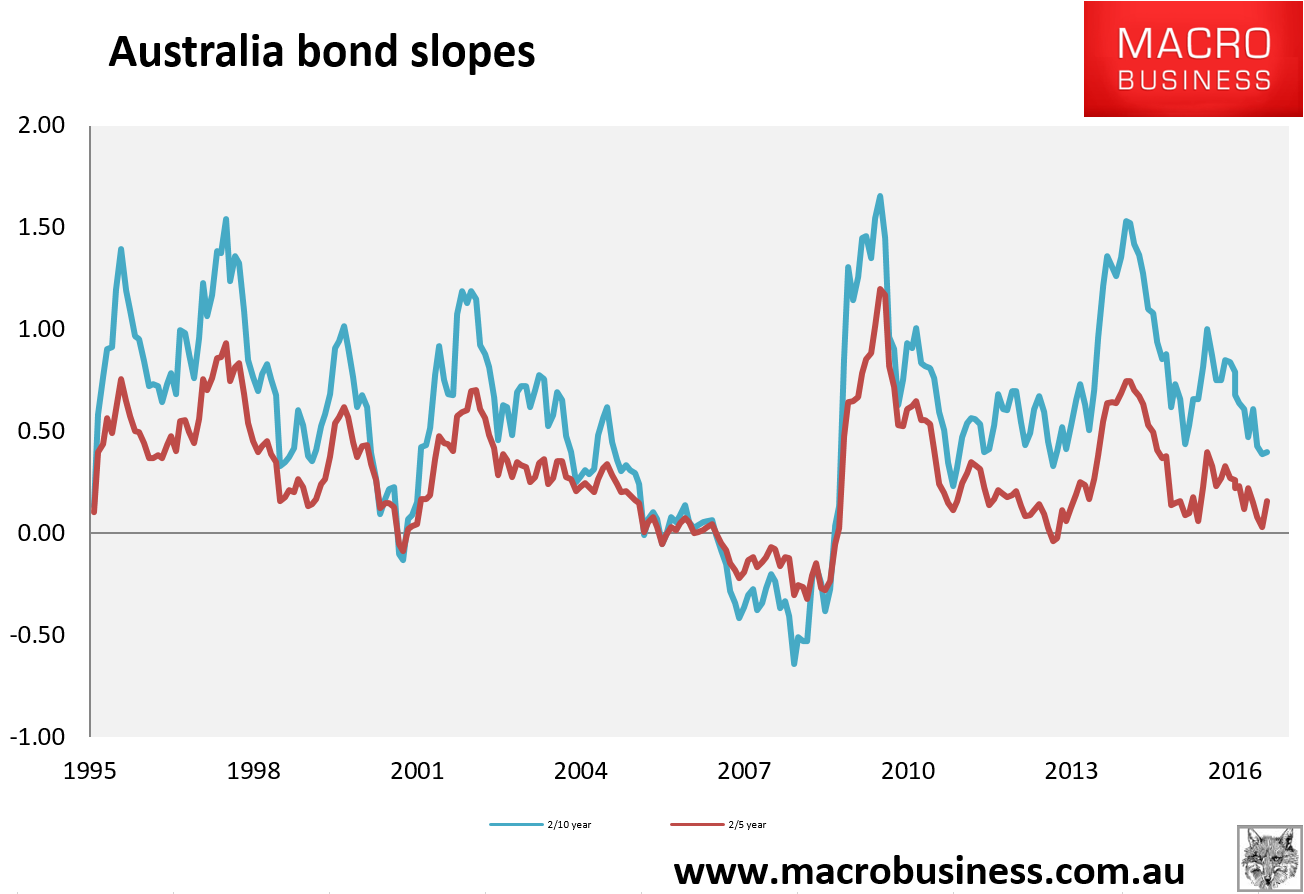

However, the yield curve or slope is still very flat on the 2/5 year, and hardly tearing it up on 2/10 either, signalling that the RBA is still in easing mode:

The last two years have seen two mid-year rate cuts and the same next year seems a fair assessment of timing. So, driver two is supportive for now turning currency bearish within six months.

Driver three, chart technicals, now looks a little bullish for the Aussie on the daily chart with the declining channel converging on a rising base:

The monthly chart is even more clear:

I can’t add much to that except to say that the macro set up is a near perfect rerun of the 2013 experience when the world waited for the Fed just as China was set to run out of stimulus puff.

For now, at least, the charts are neutral to bullish.

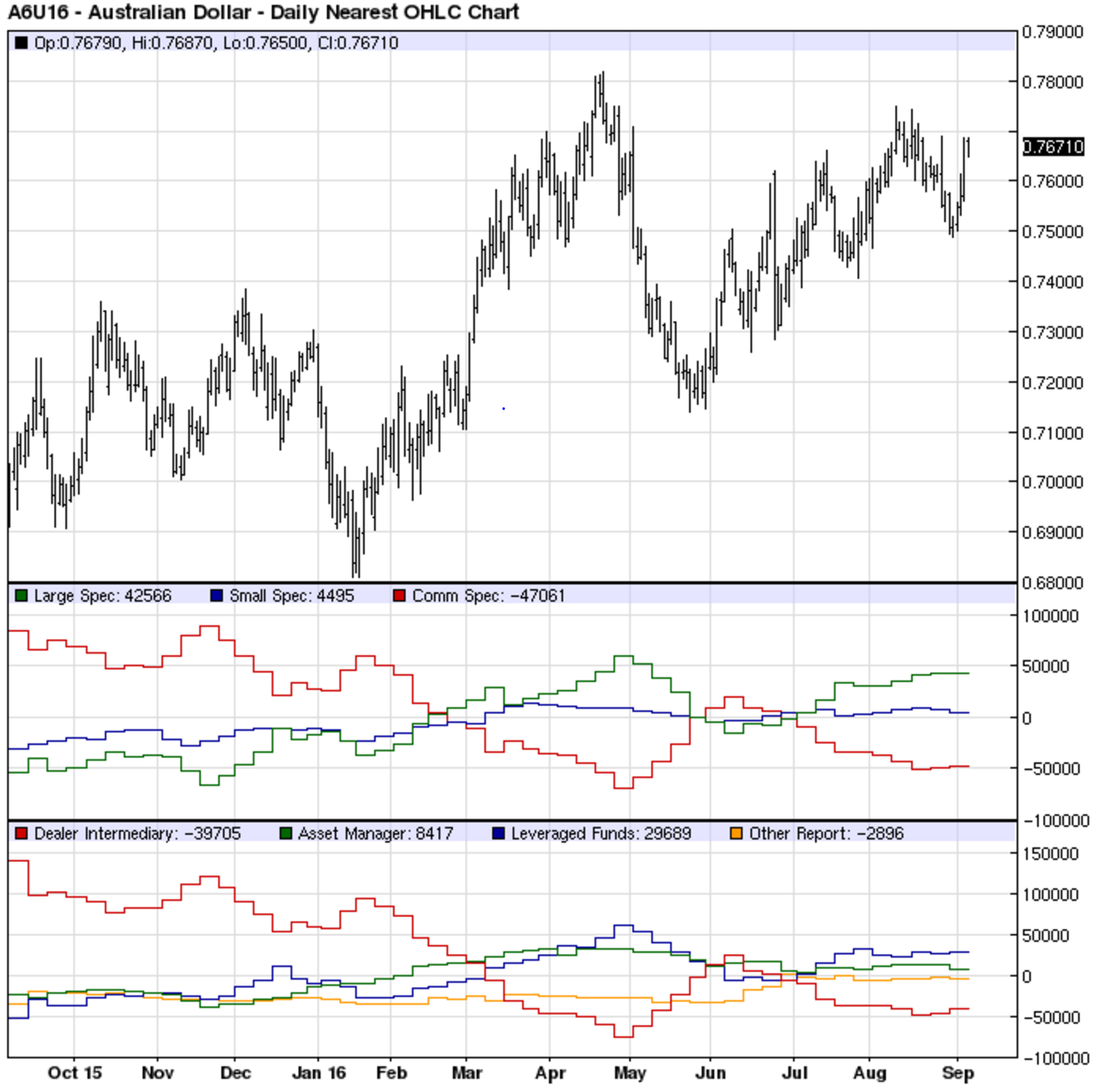

Driver four, sentiment, has the market still positioned moderately long with the Commitment of Traders report at +43k contracts:

Note the green line which has been higher but not by much. I can’t see sentiment falling of its perch given a paused Fed but I can see it being materially dented by a slowing China and the market is positioned moderately aggressively to the upside so this is bearish for the outlook.

The fifth driver, the valuation of the US dollar, has perhaps been the key change this year. Following the Mining GFC volatility of the first quarter, the Fed has roughly halved the pace of its intended tightening. That has taken a lot of pressure off the US dollar:

The chart pattern remains a perfectly neutral symmetrical triangle.

Further, when we compare the US outlook with the other large reserve currencies in Japan, Europe and Britain their weakness is very obvious with more easing likely. However, this simple pattern is complicated now by the specter of “quantitative failure” and the possibility that their extraordinary monetary tools are exhausted hence those currencies have been rising. This is premature. Japan especially has shown a willingness to innovate and its next steps will be “helicopter money” whether buying assets like stocks, giving away retail vouchers or to just fund government directly. While none of these is QE they most certainly are currency debasement!

In Europe, we have not only weak growth and the prospect of similar monetary innovation following Japan (though the Bundesbank will not be happy) but we also have severe political strains emerging around the guerrilla war with ISIS and its role in promoting anti-euro political parties in Britain, France and everywhere else to boot. This risk of a major country exit is real and any risk-adjusted valuation of the euro is much lower than its face value.

In short, even if the US dollar falls for while, I can’t see it getting far before reversing upwards given it is still the only major reserve currency worth owning. At least until the Fed embarks on another round of its own QE and that will take virtually a cycle-ending shock first.

The upshot of the five drivers is that the cyclical conditions for Australian dollar strength are currently dead neutral, which is perhaps why it is has been trading sideways for six months.

I raised my year end target to 73 cents recently on the back of changing circumstances and that still seems about right today. We could see a little higher before then but when China does slow and commodities fall the Aussie will get dragged lower once more.

Next year we still see 60 cents and have held a cycle low target below 50 cents.