Of late, market participants have found it difficult to ascertain what course of action the FOMC is likely to take in coming months, with a number of divergent perspectives on policy being offered.

Chair Yellen’s address to the Jackson Hole Symposium was therefore eagerly awaited, with all hoping a clear road map forward would be provided.

However, her address was non-committal; that is also the best characterisation of subsequent comments by Vice Chair Fischer.

From Chair Yellen, “Looking ahead, the FOMC expects moderate growth in real gross domestic product (GDP), additional strengthening in the labor market, and inflation rising to 2 percent over the next few years” is clearly a positive view of the economy. And, “in light of the continued solid performance of the labor market and our outlook for economic activity and inflation, I believe the case for an increase in the federal funds rate has strengthened in recent months” is evidence of a desire to raise rates.

However, Chair Yellen then went on to emphasise that “the economic outlook is uncertain, and so monetary policy is not on a preset course”. She also noted that “Our ability to predict how the federal funds rate will evolve over time is quite limited because monetary policy will need to respond to whatever disturbances may buffet the economy”.

In effect, the economy does not (yet) warrant a rate hike; and, while we are (likely very) close, conditions could deteriorate again.

The remainder of Chair Yellen’s speech was focused on various aspects of monetary policy — past, current and future. Albeit likely included to encourage confidence and discussion, a lengthy section on what the FOMC could do if the economy slowed — namely recommence asset purchases “until conditions had improved markedly” — added a sombre tone to the speech overall.

Following Chair Yellen’s address, Vice Chair Fischer offered an opinion on her intent. As Westpac Strategy’s Richard Franulovich noted at the weekend, when asked if Fed watchers should be looking for a move as early as September and indeed possibly more than one hike this year, Fischer stated “I think what the Chair said today was consistent with answering yes to both of your questions”. But, immediately negating the comment’s significance, he then stated that “these are not things we know until we see the data”.

Following Friday evening’s events, market participants unsurprisingly raised the odds of a rate hike by year-end to 85%, but they remained unconvinced on September, with it now a 40% probability. To our mind, market participants’ preference of December over September is appropriate, as is their unwillingness to price in a meaningful chance of two hikes by year-end.

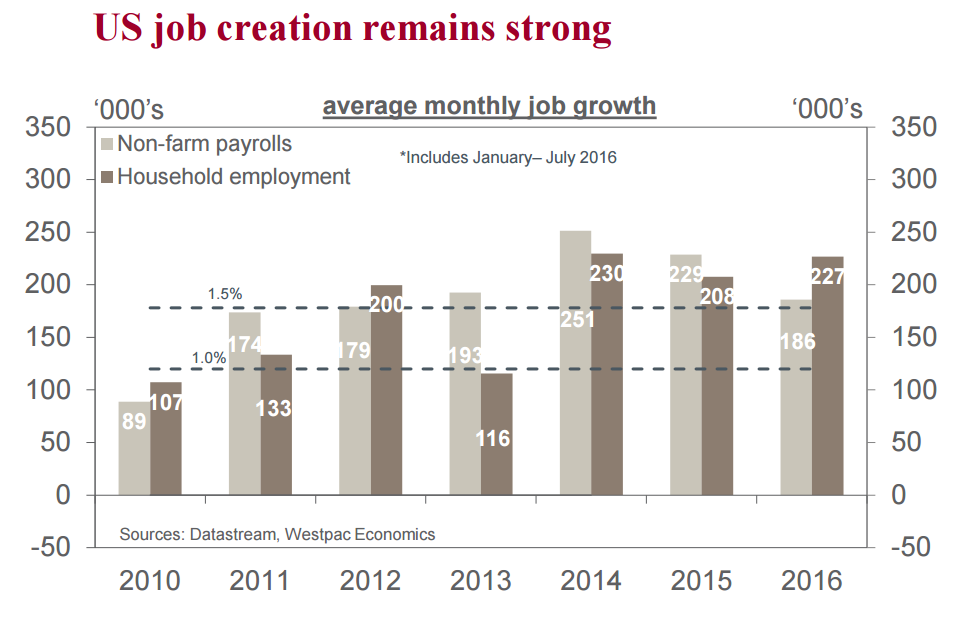

That being said, evident in both Chair Yellen and Vice Chair Fischer’s remarks is a strong focus on the labour market. Although GDP has disappointed, nonfarm payrolls and the household survey both continue to provide a firm justification for rate hikes.

If August provides another well-above expectation employment print (due on Friday), then the market would be wise to substantially raise the odds of September versus December. Having repeatedly been caught out by swings in momentum, three strong employment gains and the promise of wage and consumer price inflation may be too good a justification for the FOMC to ignore. Note, that does not mean a follow-up hike would follow immediately in December.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.