This is kind of obvious from Deutsche but it’s nonetheless charted in a way to give it substance:

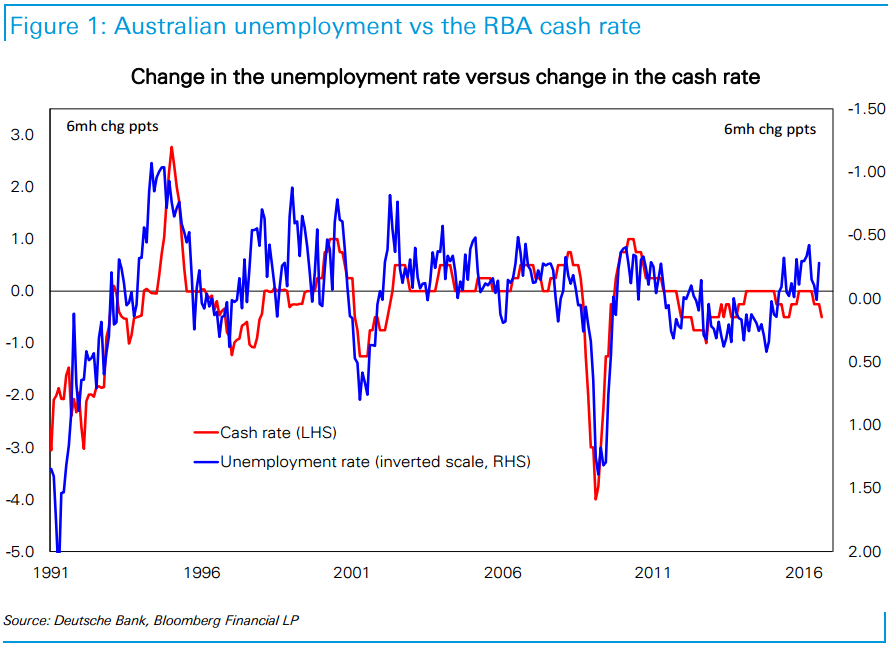

Going into the RBA’s May Board meeting we thought that the Bank would focus on the relatively robust activity side of the economy and elect not to cut the cash rate. This reflected our long standing view that the key to the RBA’s policy reaction function was the trend in the unemployment rate. With the unemployment rate actually lower over a 6 month horizon going into the May meeting the historical experience suggested to us that a rate cut was unlikely. Figure 1 shows the link between changes in the cash rate and changes in the unemployment rate since the early 1990s.

In the event the RBA did cut the cash rate, saying that the decision “follows information showing inflationary pressures are lower than expected.” We immediately concluded that the Bank’s reaction function had shifted and so we forecast a follow-up rate cut Q3 and then a further one in the first half of 2017. Our expectation that the cash rate would fall to 1.25% by mid-2017 reflected our view that the only way the RBA’s revealed preference to defend the downside to inflation would be achieved was if the AUD fell substantially. In our view this required the market expectation for the front-end interest rate differential with the US to fall to zero – which we thought could be achieved by the combination of several more rate cuts by the RBA and a number of rate hikes by the Fed. If the Fed delivers less the RBA will have to cut by more in order to take the AUD into the mid-60 cent range we think is required to have a reasonable expectation that inflation will lift to 2% over a reasonable time frame.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.