Recall Peter Martin from a few days ago:

Apparent strong house price growth in Sydney and Melbourne is unlikely to dissuade the Reserve Bank from cutting interest rates on Tuesday, in part because it’s not what it seems.

The CoreLogic home price index jumped 3.1 per cent in Sydney and 1.6 per cent in Melbourne after the Reserve Bank cut rates in May, and then a further 1.2 per cent and 0.8 per cent in June sparking fears that the Bank had ignited a new house price boom.

The jumps were inconsistent with other data showing that sales volumes and credit growth were weak.

Now Reserve Bank watchers believe they’ve cracked the puzzle. CoreLogic changed the way it calculated its indexes in May, adding to the apparent increases in cities whose prices had a history of rising quickly.

Until May it had removed extremely low and high prices from its index using bands defined in dollars. In May it switched to using bands defined by the top and bottom few percent of prices. Bank watchers believe the change pushed up the apparent price rises in Sydney and Melbourne, meaning the actual increases are less alarming.

In yesterday’s statement, the RBA said of house prices:

Supervisory measures have strengthened lending standards in the housing market. Separately, a number of lenders are also taking a more cautious attitude to lending in certain segments. The most recent information suggests that dwelling prices have been rising only moderately over the course of this year, with considerable supply of apartments scheduled to come on stream over the next couple of years, particularly in the eastern capital cities. Growth in lending for housing purposes has slowed a little this year. All this suggests that the likelihood of lower interest rates exacerbating risks in the housing market has diminished.

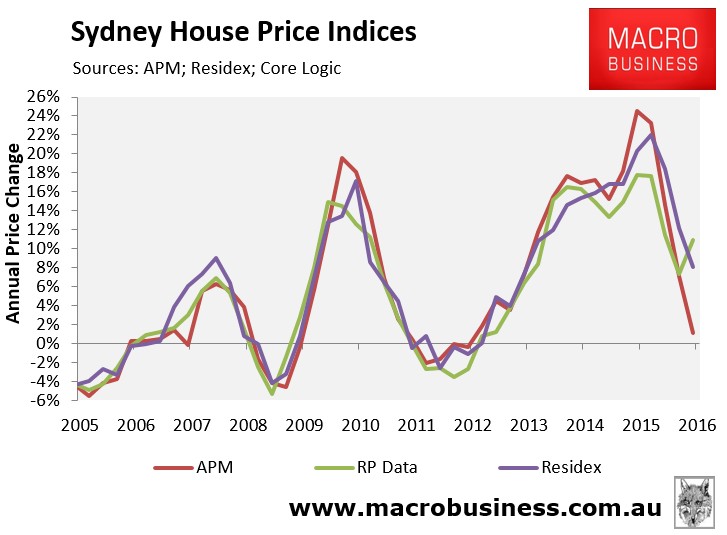

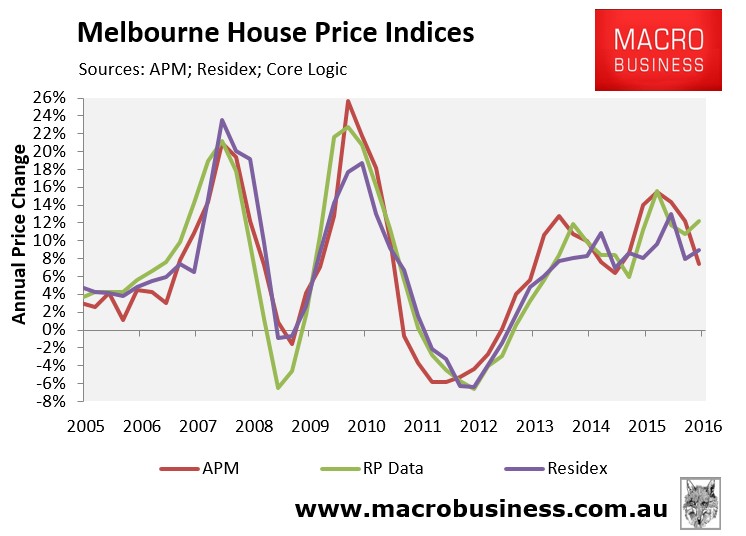

What does “only moderately mean”? Here are the three main indexes today:

You’d be hard-pressed to describe CoreLogic’s year on year price growth of 11% in Sydney and 13% in Melbourne as “only moderate”. Residex’s 8% and 9% respectively might qualify for the uber-bullish. APM’s 2% and 7% respectively seem the best match.

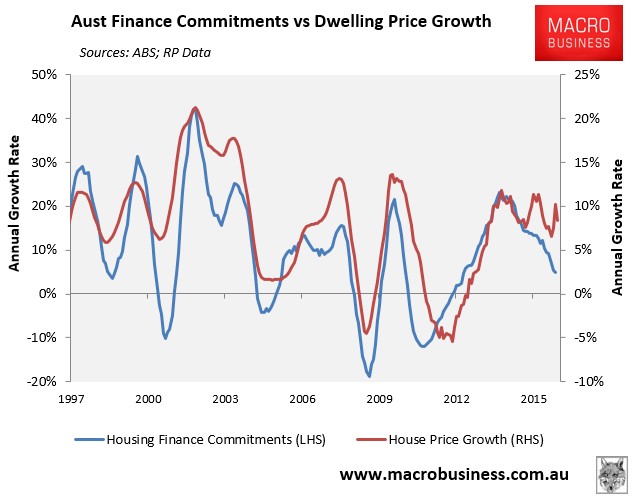

In terms of mortgage credit and historic relationships to prices, APM is also making the most sense:

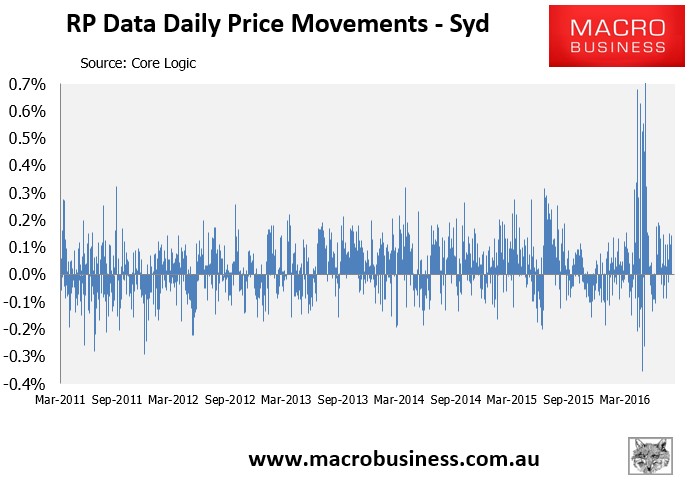

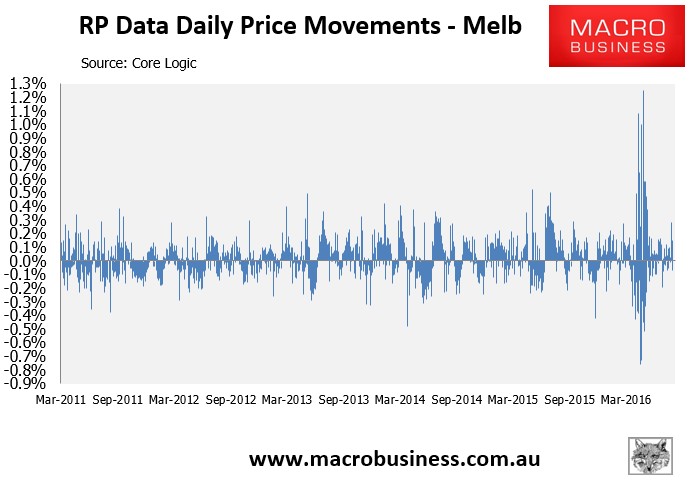

And we know that CoreLogic volatility exploded in May when it changed its methodology:

So, it appears the RBA has given the CoreLogic shift the bird. Given it is the premier index in the nation, used by everyone in markets above all others (including the RBA until now), it is urgent that the bank explain what house price measures it is now relying upon and why.

It is equally urgent that CoreLogic explain what on earth it’s done to its index.

Otherwise, Australian monetary policy is currently being set in a house price vacuum which in any economy would be bad but in the Propertocracy is potentially catastrophic.