Earnings disconnect from the economy. Our equity strategy colleagues highlighted this week the loss of earnings momentum in reporting season despite reasonable real GDP growth domestically. Many of the factors they reference that are creating this underperformance – including global factors and low inflation – are captured in very low nominal income growth.

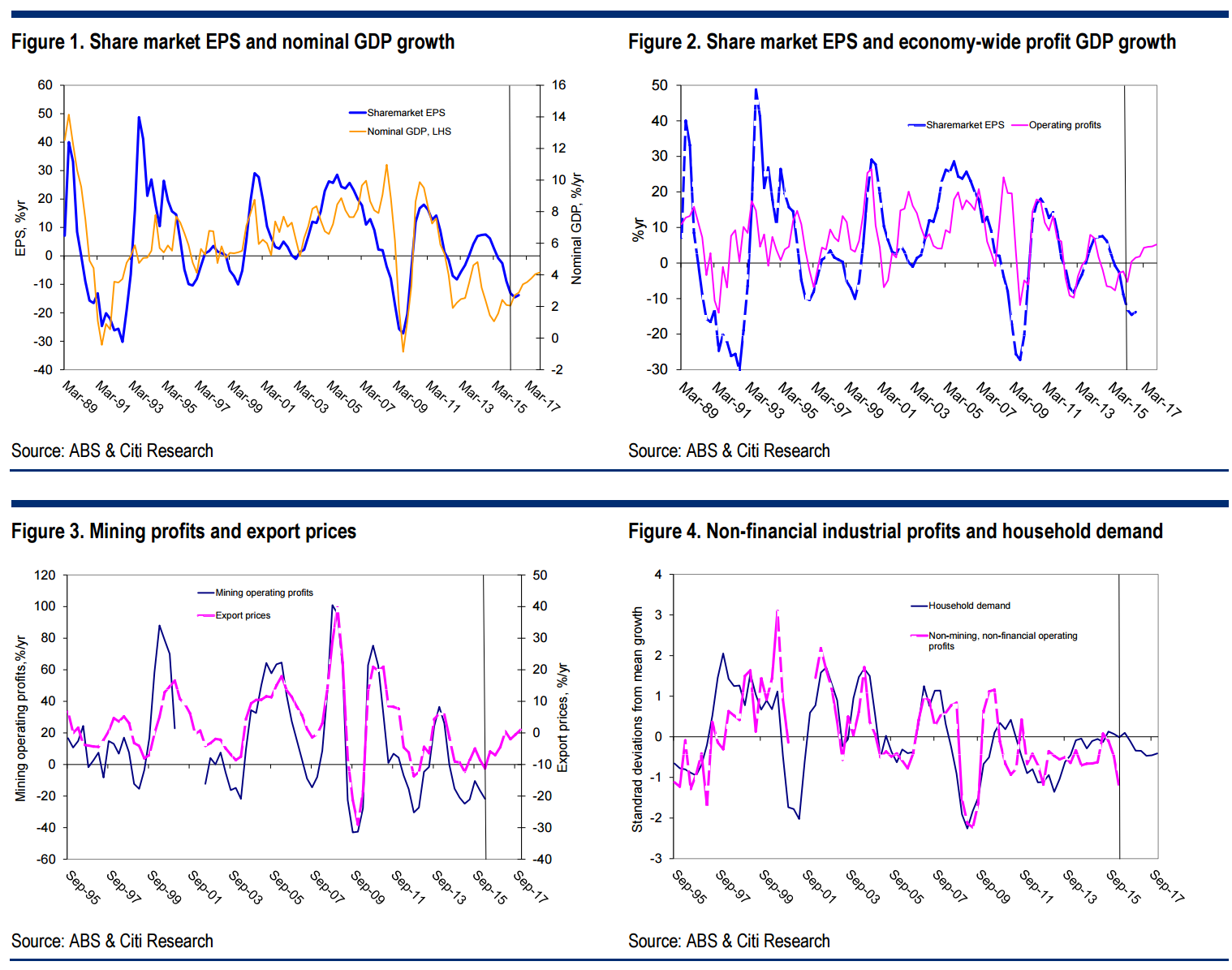

Earnings have followed lower nominal GDP. In an environment where nominal incomes are only growing by 2% it isn’t surprising that company earnings would be struggling (Figure 1). The combination of low inflation, and therefore low interest rates and low pricing power, and the declining terms of trade has impacted earnings of a wide range of businesses from resource companies to industrial and financial companies.

The good news is that the slowdown in nominal GDP may have bottomed. The recent bounce in commodity prices should see a rise in the terms of trade in H2 this year. Provided this isn’t offset by a rise in the AUD this should be positive for resource earnings. The RBA also forecasts that inflation has bottomed and will pick up gradually. This too would lift nominal GDP and imply some pricing relief for retailers and other industrial businesses.

Share market earnings are weaker than economy-wide profits. Profits in the National Accounts from the ABS include all companies across the economy. This broad measure of profits has been falling, but not by as much as share market earnings (Figure 2). Apart from company coverage differences, share market P&Ls include abnormals, capital gains/losses on trading activities and offshore production. Weaker earnings from these sources therefore could help explain the differences with the National Accounts estimates.

Any pick up in nominal income growth is likely to be sub-par by past standards. Even if inflation has bottomed, and the risk is that it hasn’t yet, interest rates are likely to remain very low and the RBA could cut rates further given that the cash rate is still well above most other global rates and this is creating an upward bias to the AUD. In addition, the sub-par global economic growth, less commodity intensive growth in China and increasing commodity supply will limit the upside to commodity prices and the terms of trade. In any case, according to the ABS data splitting profits across resource companies and industrials (ex banks), profits have underperformed key economic fundamentals (Figure 3 and Figure 4). This potentially suggests there are structural headwinds to lifting profit growth in a low income environment.

We might see a brief reprieve for profits growth next year on this year’s iron ore rebound and then it’s back into the lost decade, I’m afraid.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.