There are not many authorities around the world that would be fretting about a lift their terms of trade but Australia is one of them. The reason is that the material lift in dirt prices driving recent improvements in the terms of trade has also raised the Aussie dollar and in so doing has completely stalled any kind of “rebalancing” in Australian tradable sectors. UBS has more:

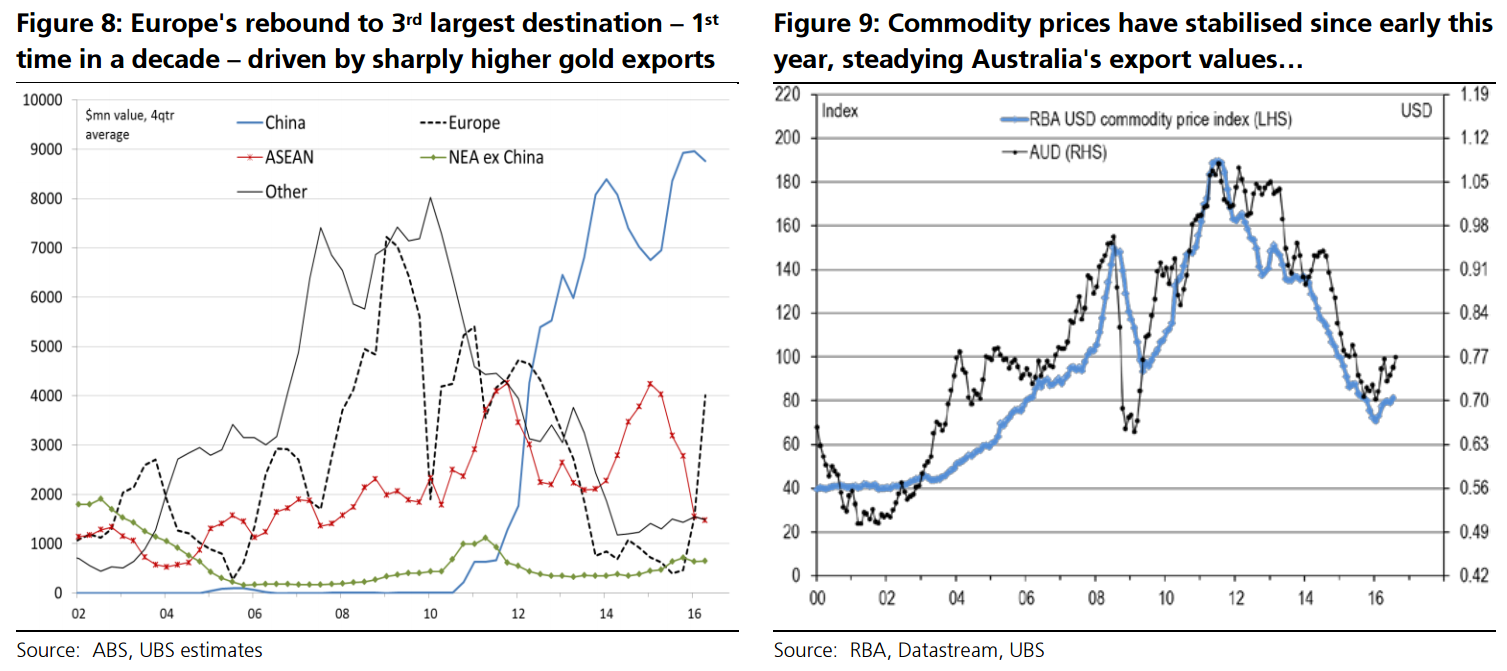

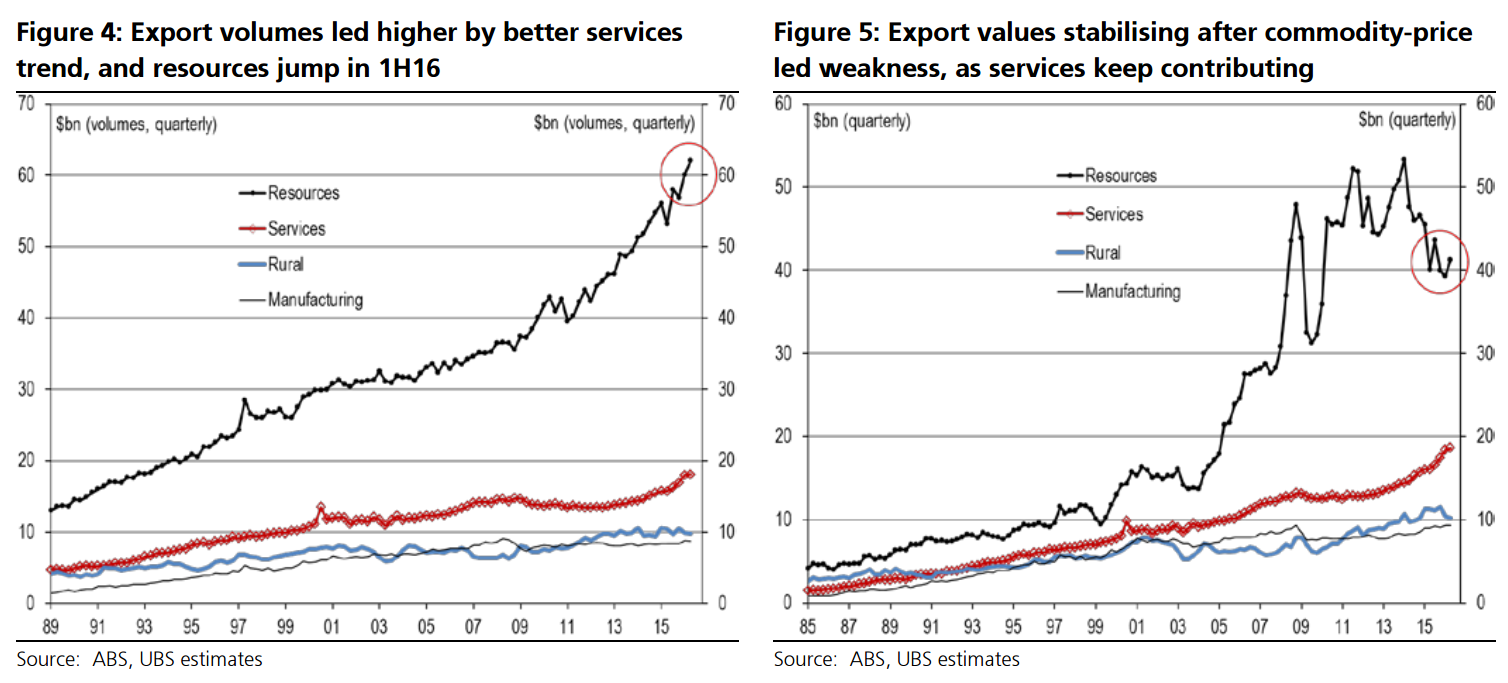

Australia’s commodity exports, both volume & value, are making a comeback. Indeed, when the Q2 GDP data are released early next month, we expect to see another gain in export volumes, the 4th consecutive, with a ~1½% q/q rise in Q2 lifting to ~2½% the y/y contribution to growth from net exports, alone worth 80% of Australia’s overall ~3% y/y GDP growth (with domestic growth closer to 1% y/y). The recent stabilisation in Australia’s commodity prices, with USD prices up 12% from their early 2016 lows (& up 8% in AUD terms from end-15), is combining with better volumes to underpin a rise in Australia’s export receipts, likely up 4% y/y for Q216, their fastest pace in more than 2 years. While we look for some softening in commodity prices over 2H16, recent trends should see Australia’s terms of trade rise in Q2, the first quarterly gain in almost 3 years, suggesting the worst of the ‘negative income shock’ from falling commodity prices may have passed. Also of note, while higher resource volumes and steadier prices have unsurprisingly lifted China’s share of Australia’s goods exports higher, to 34% from 31% (still below the peak of 39% at end-13), Japan’s trade share has slumped to just 12% from a 20- year average of 19%, led lower by iron ore, coal & (most likely) LNG exports. In contrast, Europe has almost doubled its goods export share to 9% from 5% – to be Australia’s 3rd largest destination, the first time in a decade – driven by a 500% jump in gold exports (to $4.0bn in 15/16, from $0.6bn in 14/15).

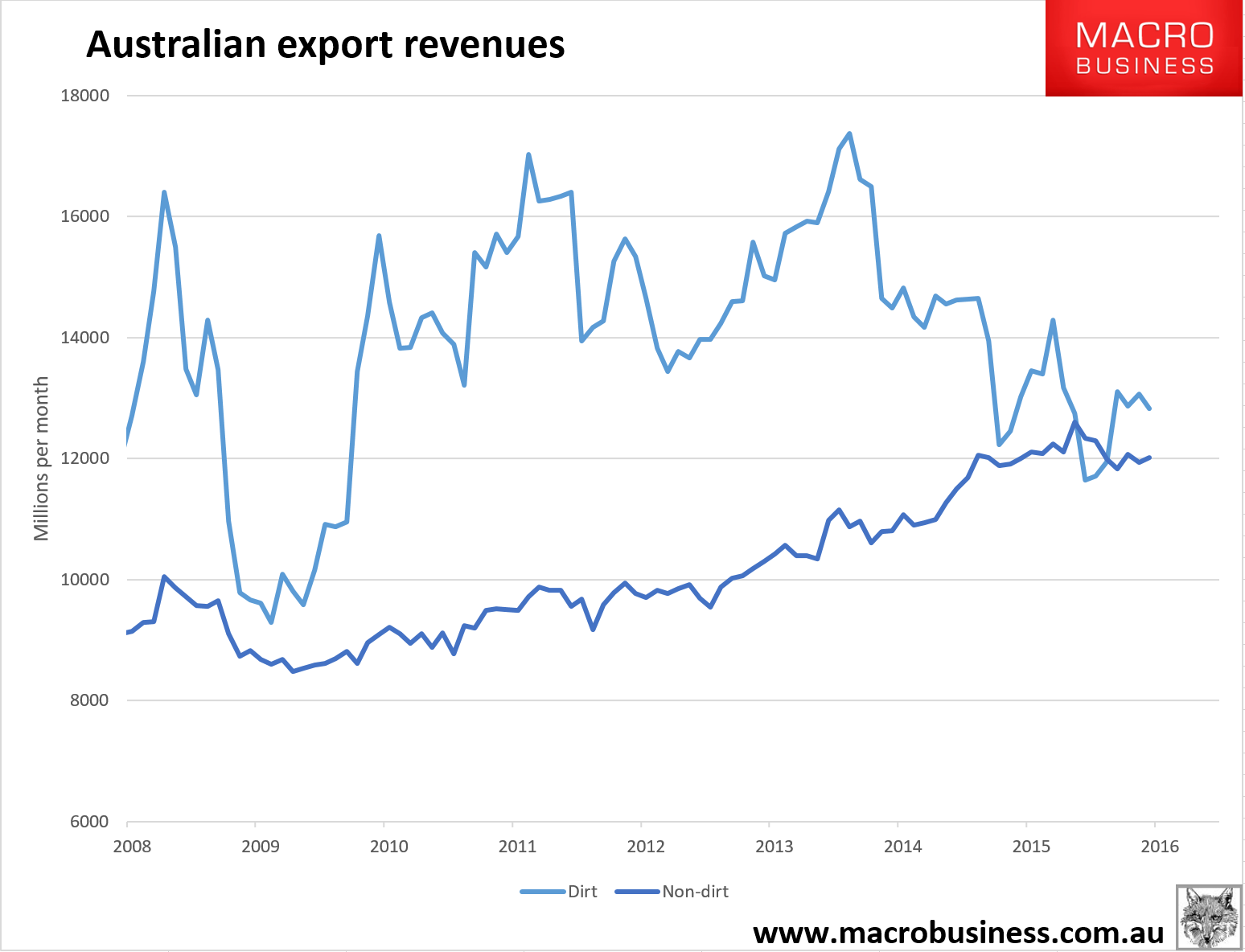

Let’s look at those bottom charts up close. For mining versus non-mining exports:

Advertisement

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.