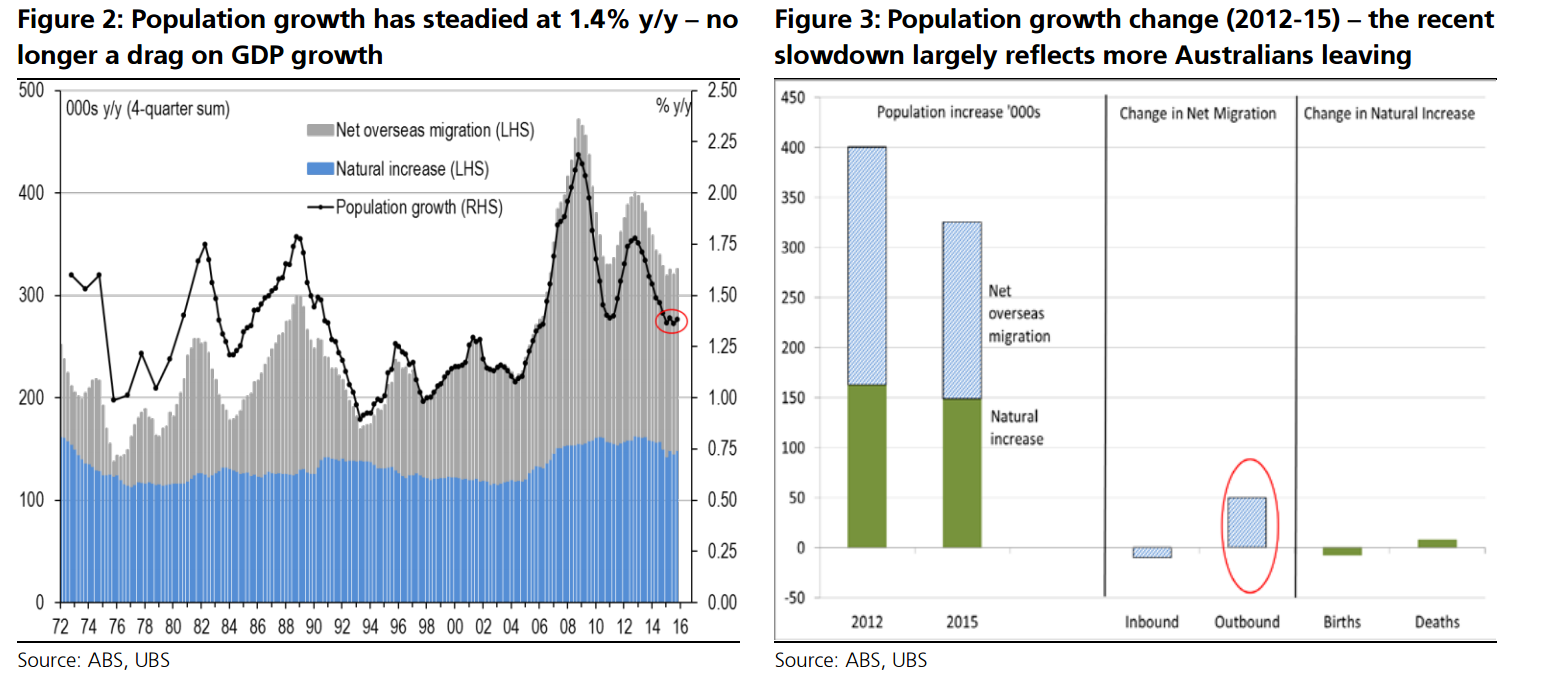

Australia’s population growth has stabilised at 1.4% y/y – still high by international standards – after a few years of slowing from 2012’s recent peak of 1.8% y/y. This stabilisation is positive news for Australia’s growth outlook.

80% of this prior population growth slowdown has been due to reduced net overseas migration (with the rest due to a few less births & a few more deaths per year). But interestingly, slowing in net migration has been almost entirely due to a pick-up in Australians migrating offshore (with a record 306k Australians migrating outbound in 2015), rather than fewer inbound permanent migrants.

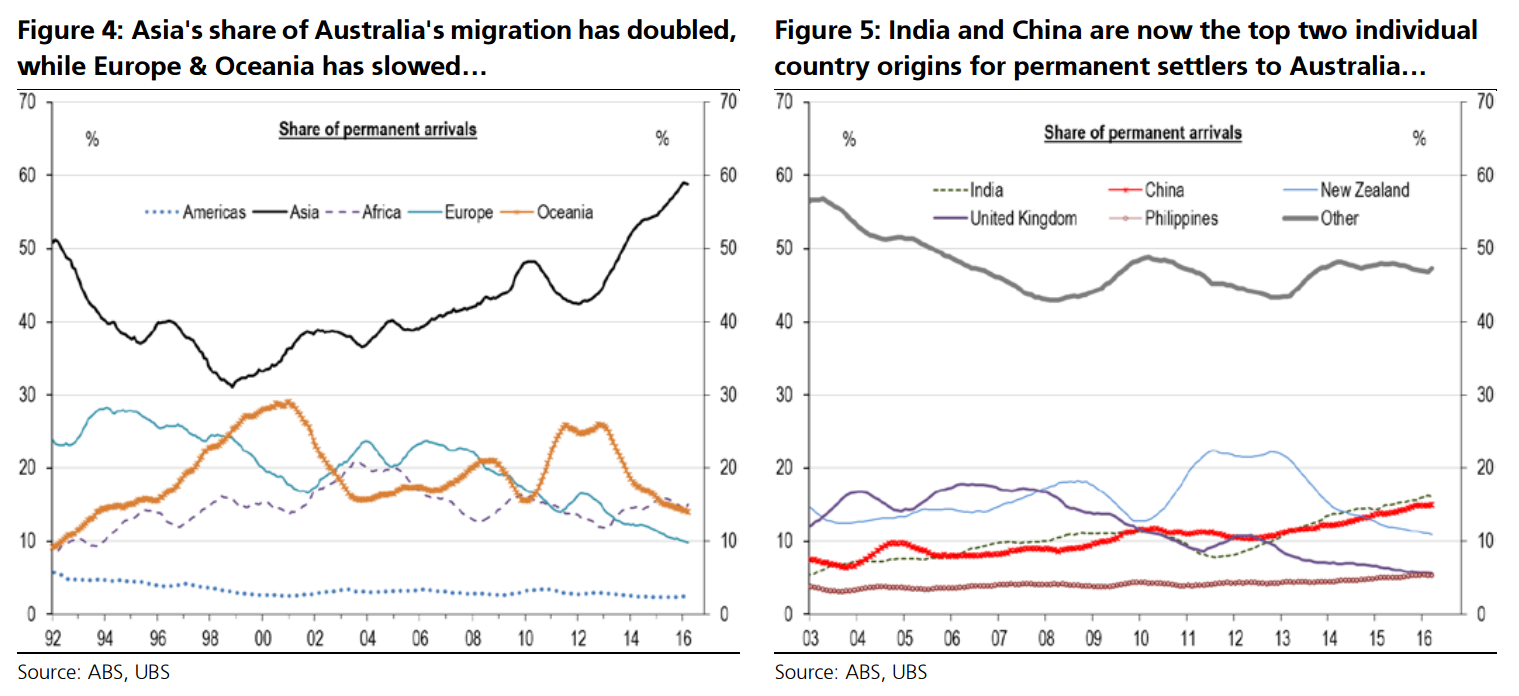

Where does Australia source its relatively steady flow of almost 500k inbound new arrivals each year (2% of the population)? Almost 60% come from Asia, while those from Oceania & Africa make up about 15% each. Only about 10% come from Europe, while the Americas are a small but steady 2-3% each year. This is in stark contrast to the late 1990s, where once 50% of arrivals came from Europe & Oceania together (halved now to only 25%), and a smaller 30% came from Asia (now doubled to 60%). By country, the five dominant origins are India, China, NZ, UK & Philippines, which together determine about 50% of permanent arrivals. India & China have risen to the top two spots over the past 5 years (each rising from a ~10% to a ~15% share).

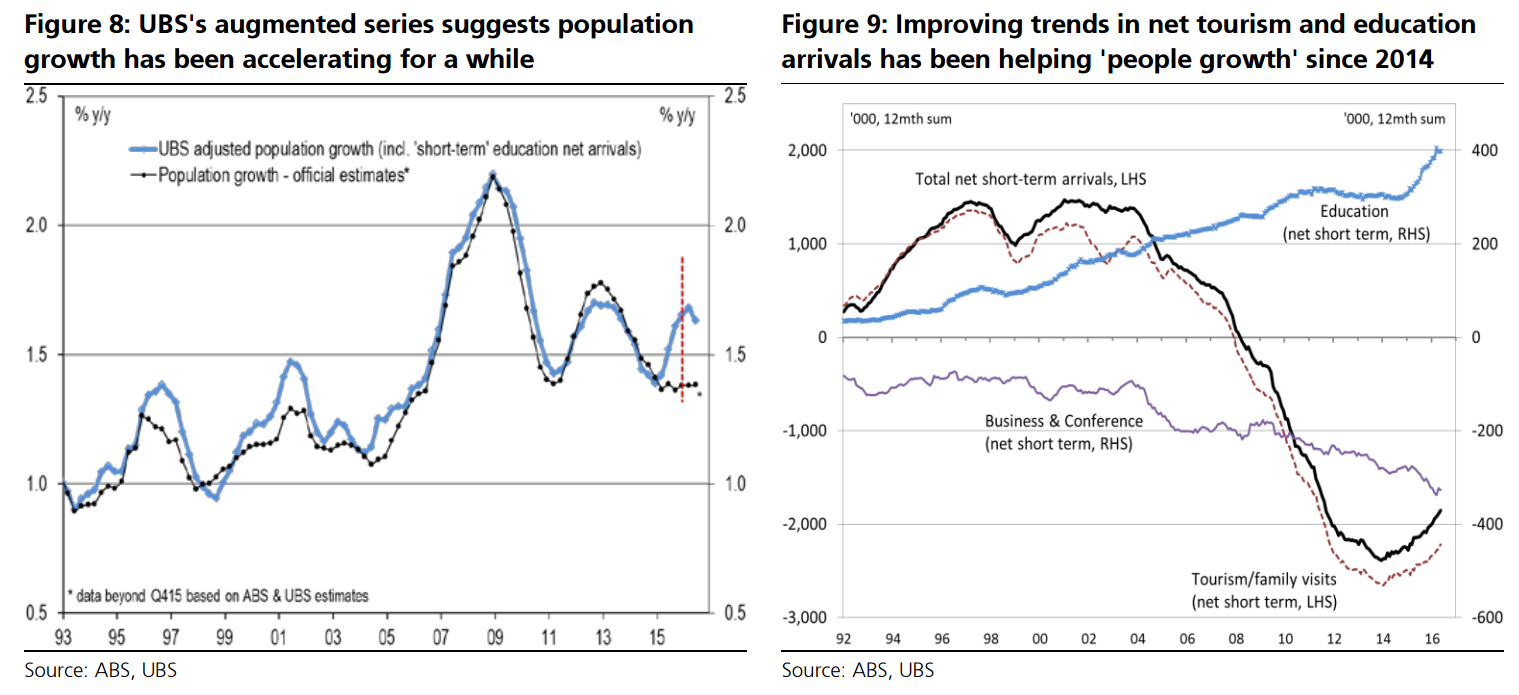

We also update our ‘augmented’ population growth series, which captures the ongoing 20% boom in short-term student arrivals excluded from the ABS’s population data, and our ‘people growth’ measure (~2½% y/y, which includes the still improving trend in net tourist arrivals). Both show the recent sharp pick-up in ‘people on our shores’ – helped by a lower AUD – that continues to positively support activity.

“Positively support growth” should read ‘positively support growth in chosen sectors while damaging it in others with a net result over time of a falling standard of living’.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.