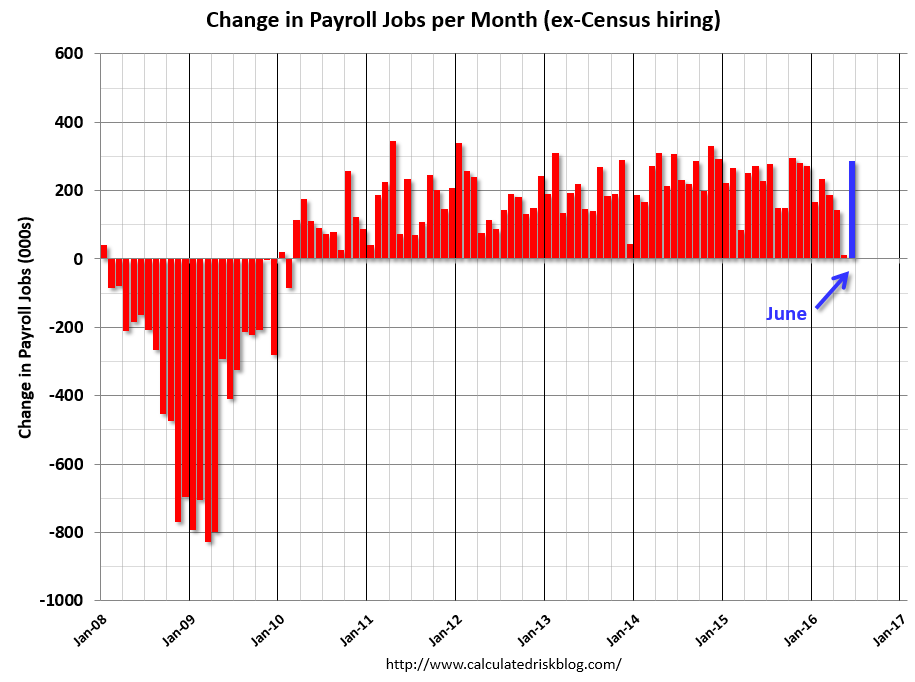

US jobs on Friday night blew up just about everyone to the upside, from the BLS:

Total nonfarm payroll employment increased by 287,000 in June, and the unemployment rate rose to 4.9 percent, the U.S. Bureau of Labor Statistics reported today. Job growth occurred in leisure and hospitality, health care and social assistance, and financial activities. Employment also increased in information, mostly reflecting the return of workers from a strike.

… The change in total nonfarm payroll employment for April was revised from +123,000 to +144,000, and the change for May was revised from +38,000 to +11,000. With these revisions, employment gains in April and May combined were 6,000 less, on net, than previously reported. Over the past 3 months, job gains have averaged 147,000 per month.

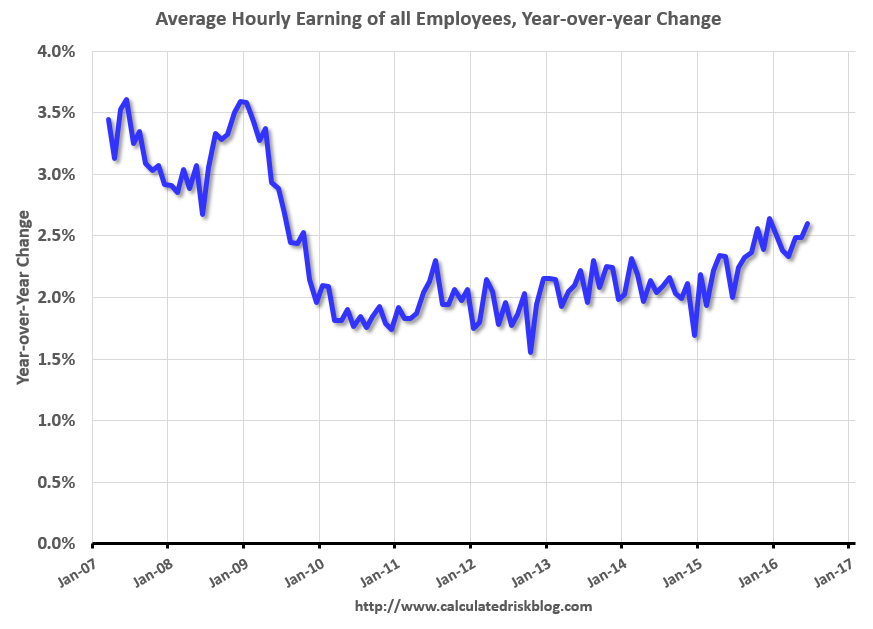

…In June, average hourly earnings for all employees on private nonfarm payrolls edged up (+2 cents) to $25.61, following a 6-cent increase in May. Over the year, average hourly earnings have risen by 2.6 percent.

Recall that 35k jobs were lost and then gained across the two months owing to a large Verizon strike. The three month average remains a material slowing in the US labour market.

Charts from Calculated Risk, the headline:

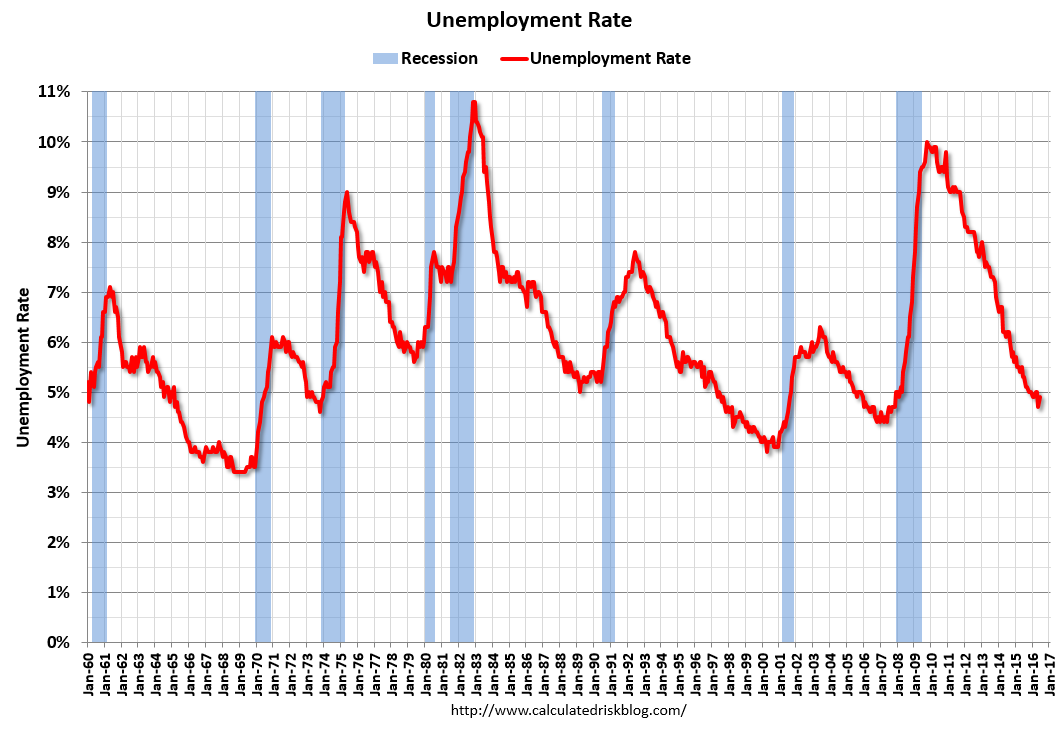

The unemployment rate rose a little:

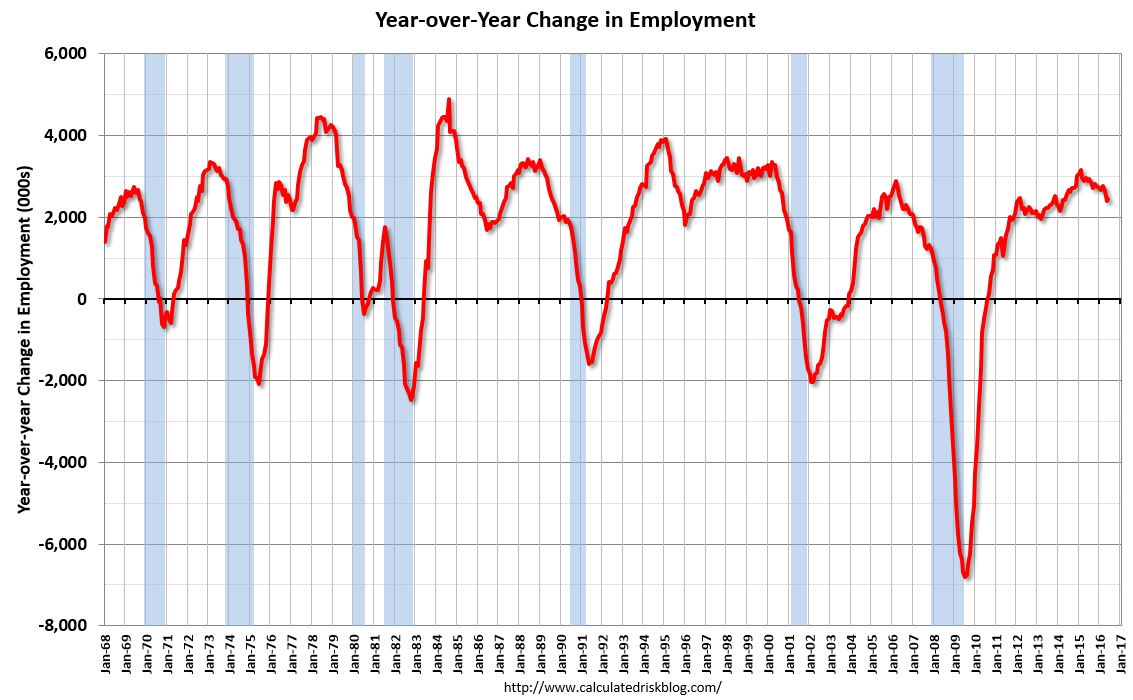

Year on year growth ticked up:

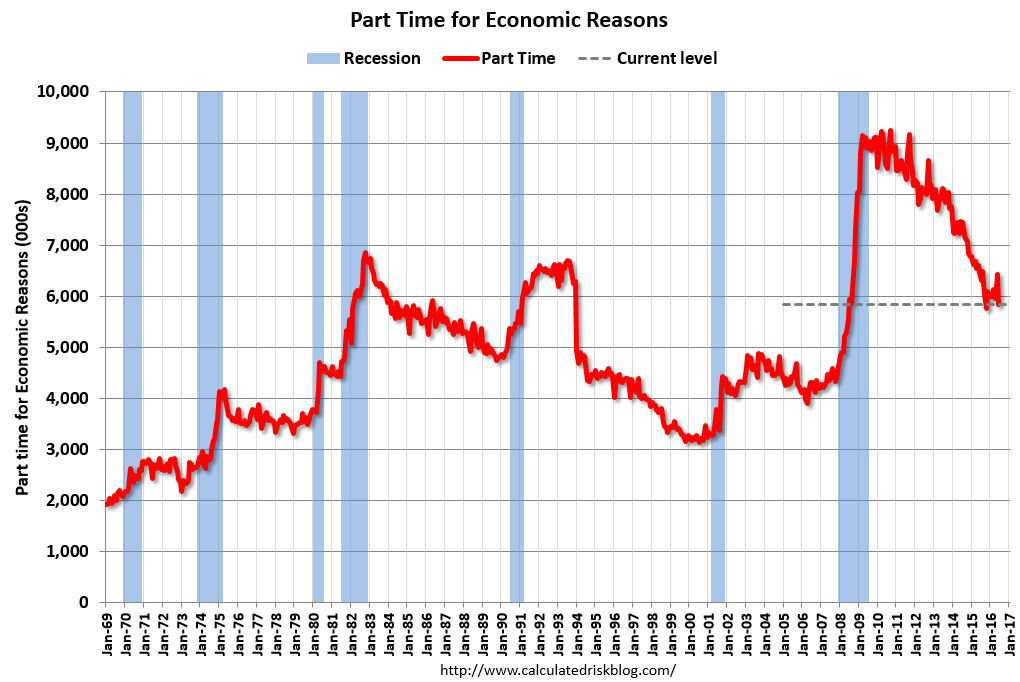

Part time ticked down but is still very high:

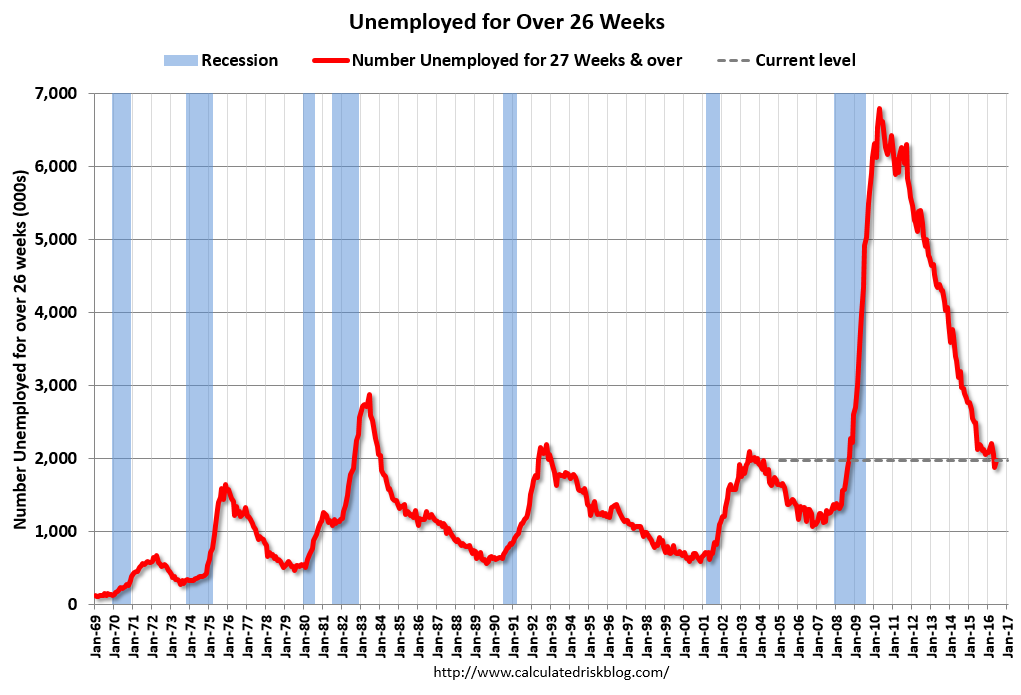

Long term jobless lifted and is still very high:

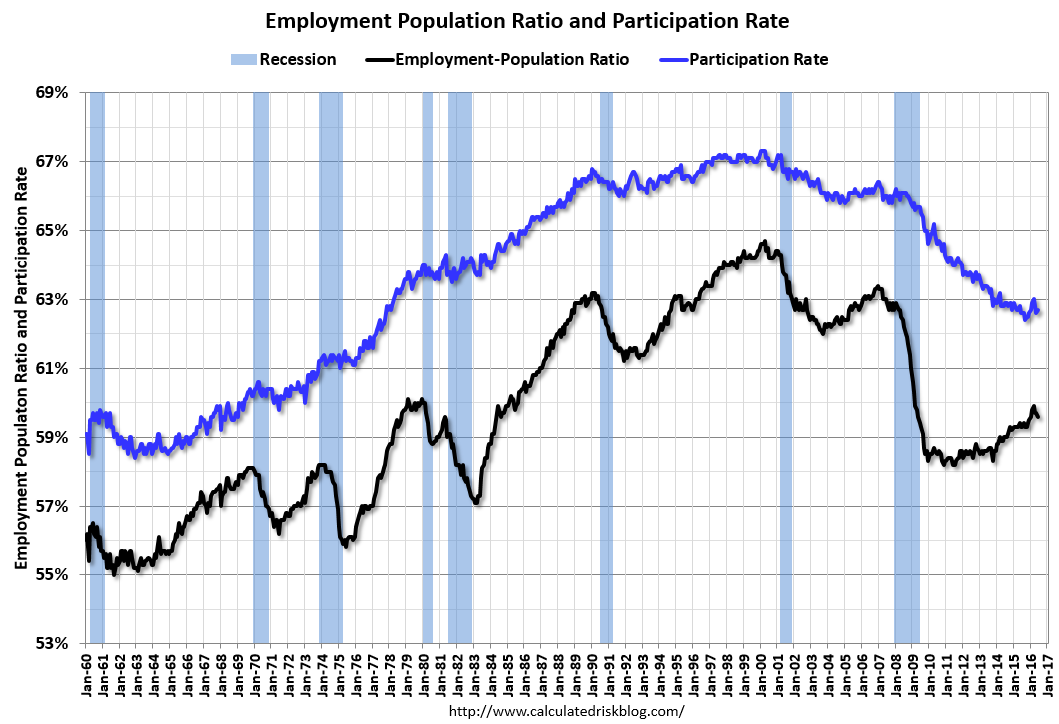

Participation improvement has still stalled:

Income resumed its shallow growth trend:

A strong report but with such volatility it’s obvious that we should look at the moving averages which still project a material downshift in the US labour market in the last quarter. Jon Hilsenrath warned of a hawkish Fed:

Fed officials are likely to be relieved by today’s job report, which shows a noted rebound from the one for May, and not panicked into raising short-term interest rates quickly. They are likely to look at the two months together; May and June averaged job growth of 149K, a slowdown from prior readings and roughly in line with the pace of gains officials believe is needed to keep the jobless rate below 5%. Moreover, 2.6% year-over-year growth in average hourly earnings for private-sector workers will strengthen the Fed’s conviction that waning slack in labor markets is putting modest upward pressure on wages. Taken altogether, this increases the chances of a September rate increase. But officials are likely to remain in a wait-and-see mode.

And Goldman:

MAIN POINTS:

1. Nonfarm payroll employment increased by 287k in June, a sharp rebound from a downward revised 11k rise in May. Net revisions for the prior two months totaled -6k. The three-month moving average of employment growth was to +147k—above our and Fed estimates of the payroll “breakeven” rate, or the amount needed to reduce spare capacity in the labor market over time. Job gains in most categories accelerated last month, especially in the weather-sensitive retail (+30k vs. +3k), leisure & hospitality (+59k vs. -3k), and construction (flat vs. -16k) sectors. Most other details in the establishment survey were also firm, including increases in manufacturing (+14k from -16k), information (+44k from -39k; reflecting the conclusion of the Verizon strike), and temporary help (+15k from -19k) categories. The payrolls diffusion index—which represents the percent of industries with employment rising—rebounded to a trend-like 62.4% after falling to its lowest levels since early 2010 in May.

2. The household survey was slightly softer than the establishment survey, showing a 67k increase in employment in June, following soft growth in May (+26k) and April (-316k). The unemployment rate rose to 4.9% (4.899% unrounded), as the labor force participation rate rose by one-tenth to 62.7%. The U6 underemployment rate declined 0.1pp to 9.6%, mostly due to a decline in involuntary part-time employment.

3. Average hourly earnings rose 0.1% in June (vs. +0.2% consensus) and were up 2.6% on a year-on-year basis, an increase from 2.5% in May. In our view the below-trend increase in average hourly earnings reflects calendar quirks, rather than fundamental news about wage growth. Average weekly hours remained at 34.4 for the fifth consecutive month.

4. With payrolls, unemployment claims, consumer sentiment, vehicle sales, and a number of business surveys in hand, our preliminary read for the June Current Activity Indicator is +2.1%, up from +1.0% in May (labor market data in the CAI are adjusted for the effects of strikes). The three-month moving average edged up to 1.7% from 1.6% in May.

5. For Fed policymakers, today’s report is likely to allay concerns about US growth momentum, in our view, and keep the committee on track to raise rates at some point later this year. We continue to see a 25% chance of a rate increase in September and a 40% chance of a hike in December—plus some small possibility of a rate increase at the November meeting. Action as early as the September meeting would require definitively strong growth data between now and then, plus negligible fallout from the vote in the UK to leave the EU.

Europe and China slowdowns are coming. The Fed is done.