― Measures of consumer sentiment globally suggest the shock from the UK’s ‘Brexit’ vote has been minor and that sentiment overall is slightly positive, albeit with above average reads in developed economies partially off set by below average reads for emerging economies.

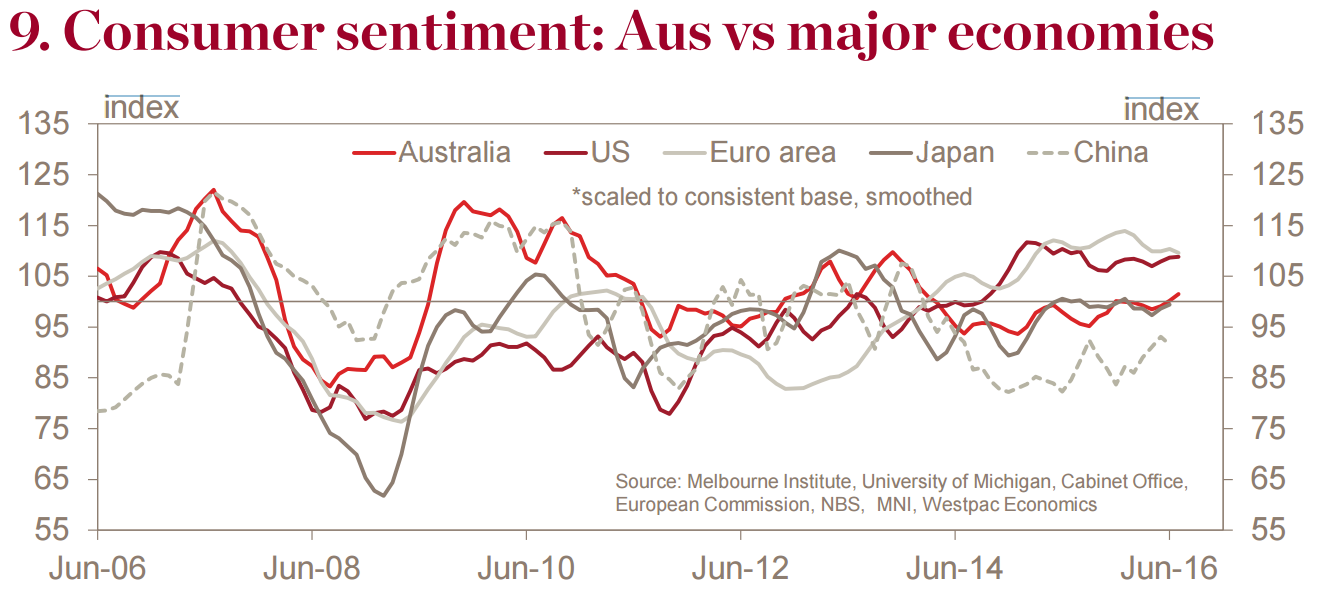

― Chart 9 shows sentiment across the major economies and Australia. All measures are scaled to a consistent base and smoothed to reduce volatility. Most recently, consumer sentiment in the US and Euro area has been well above average (9-10pts). In contrast, sentiment is around average in Japan and 8.5pts below average in China.

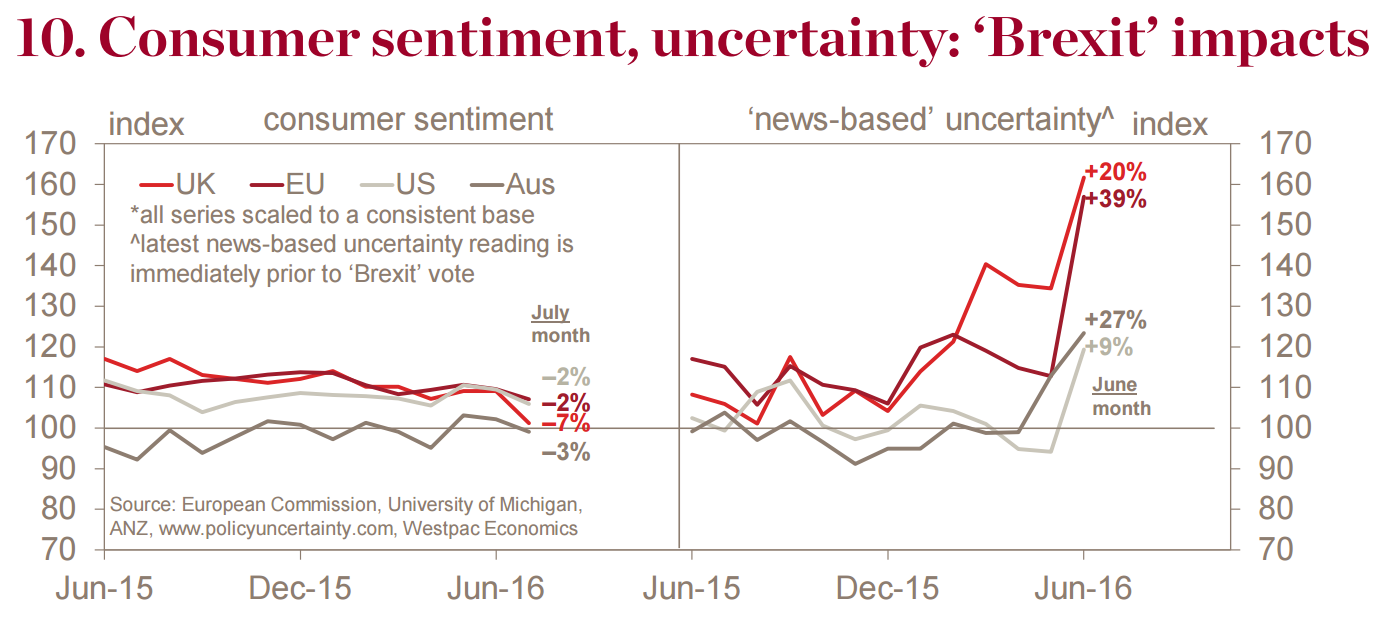

― We now have a handful of post-‘Brexit’ readings on consumer sentiment. Together these suggest a material hit to sentiment in the UK but a much more muted impact elsewhere.

― Sentiment in the UK dropped 7% in the Jul month, having already slipped since the start of the year (down 11% in total). ‘Flash’ estimates point to a much more muted 2% dip in the EU and the US. Note that in all cases, sentiment readings were coming from an above average starting point and remained above long run averages. This is in stark contrast to ‘newsbased’ measures of uncertainty that spiked to extreme levels in the Jun month.

― Consumers globally may be taking their cues sentiment-wise from financial markets – more specifically equity markets. These fell sharply immediately following the surprise result but recovered quickly and strongly (even, remarkably, in the UK and Europe). That means reactions may be, to some extent, provisional.

― The path forward post-‘Brexit’ remains complex and uncertain, and is likely to be drawn out. It will involve at least some further bumps along the way with a material growth slowdown now expected for the UK. There will probably be more shocks to come but the Jul reaction suggests the global impact is likely to be limited.

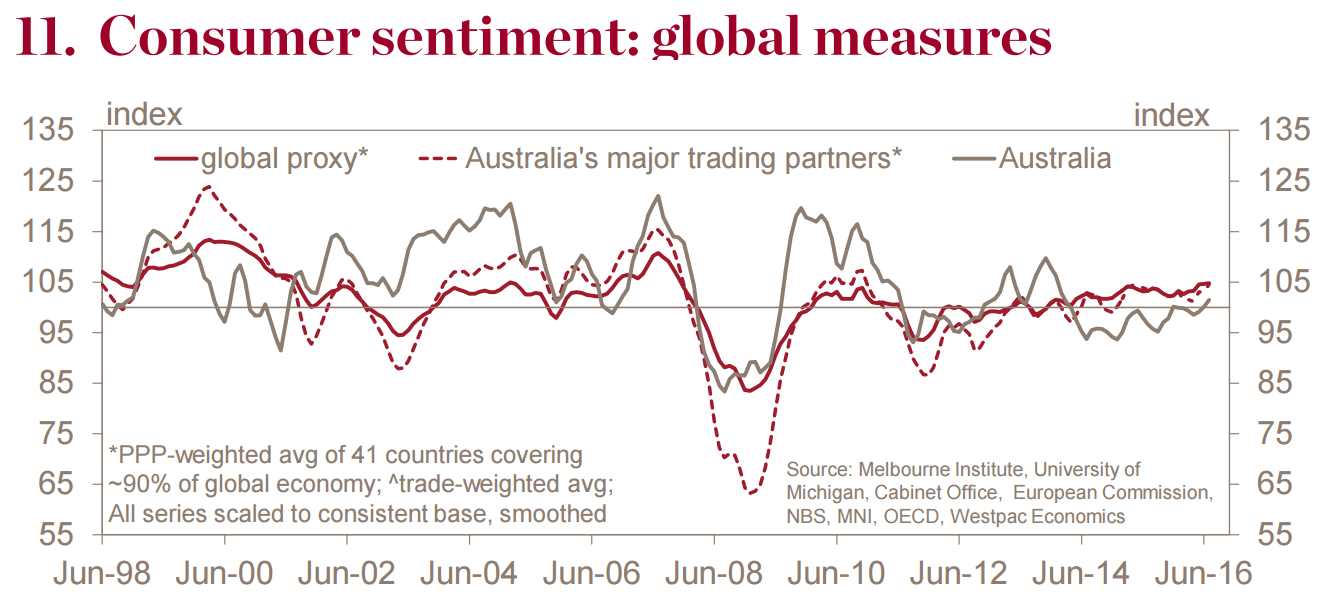

― Chart 11 shows a ‘global proxy’ that combines consumer sentiment measures from over 40 different countries, accounting for 90% of world GDP. This has held its ground in recent months despite the softening in Europe. Sentiment globally remains 4-5ppts above its long run average and up about 0.5ppt since Apr.

― Sentiment is weaker in the Asian region although even here readings vary. Sentiment remains relatively downbeat in China, Japan and Korea and very weak in Thailand but is holding comfortably above average in Taiwan and Indonesia and is solidly positive in India. Note that many markets do not have measures.

Amazing charts. We are much less confident than US and European consumers and well below the global average.

One can easily imagine what the Pasconometric turkeys that run the place would conclude about these charts: we need to be more positive. Lost on them will be that that is actually the problem. Australians know that their standard of living is falling. They see it in stagnant pay packets. They know it in the supermarket bill. They feel it in every traffic jam. They sense the bubble in their bones.

So when leaders tell them how lucky they are they only get more disillusioned with leaders, more angry at not being listened to and more withdrawn in terms of spending habits given nobody is offering a plan to fix things.

Advertisement

It’s like telling someone with depression to cheer up, it only makes them feel like sticking their head in the noose because it isolates them further. Pasconomics is the problem not the solution.

The answer to better consumer sentiment is the truth. Leaders should be honest about the structural challenge, should be open about its difficulties, and should draw the entire community into the answer which is quite straight forward. We’ve all got to give something up so that the economy overall can repair its competitiveness then things will improve.

In short, recognise the problem then offer a plan to address it. Don’t tell someone depressed to cheer up, give them the number of a good therapist.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.