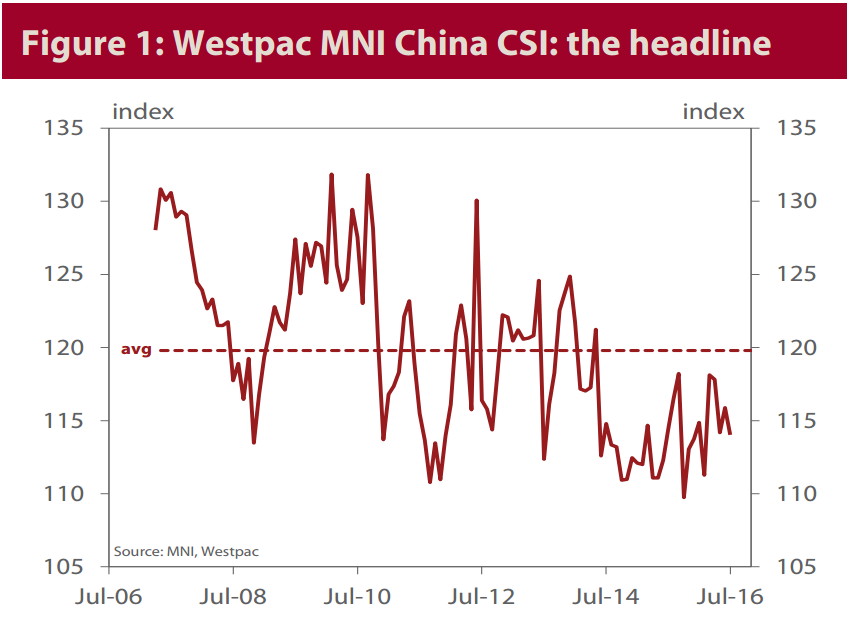

• The Westpac MNI China Consumer Sentiment Indicator slipped 1.6% to 114.0 in July from 115.9 in June. The Indicator is now back in line with its May read and remains well below its 10yr average of 119.7.

• Note that the survey was in the field over the first half of July, in the midst of global financial market turmoil following the UK’s surprise ‘Brexit’ vote but prior to recent severe flooding in Northern China.

• All components retraced in July. Assessments of ‘time to buy a major item’ posted the biggest fall, down 2.9%, closely followed by ‘family finances vs a year ago’ down 2.3% and ‘family finances next 12mths’ down 1.9%. Assessments of the business outlook showed more modest declines – ‘business conditions, next 12mths’ down –0.7% and ‘business conditions, next 5yrs’ down –0.5%. All components have been below their 10yr average levels over the last three months.

• The pull-back is despite a further improvement in current business conditions. ‘Business conditions vs a year ago’ rose a further 2.2% in July after surging 5.2% in June to a new 2½yr high (note that this index is not part of the headline composite but is highly correlated with the PMIs & official IP). Job security deteriorated however with the employment indicator down 2.7%, reversing about a quarter of the promising improvement seen over the previous four months.

• Consumer attitudes towards real estate were steady, the housing composite up 0.3% nationally and 1.3% above its long run average. Assessments of ‘time to buy’ were more downbeat (–1.4%) but house price expectations firmed (+1.2%) The proportion nominating real estate as the ‘wisest place for savings’ rose a further 2.7pts to an 18mth high with 11% of consumers nominating house purchase as the primary ‘motivation for saving’ (up 1.6pts in the month and 4.5pts over the last year). Responses around savings more generally continued to show a strongly ‘risk averse’ tone.

• Spending-related sentiment – both purchasing plans and perceived buying conditions – pulled back sharply in July. After hitting a 2yr high in June, shopping plans slumped 5.8% in July. Planned spending on ‘entertainment’ and ‘dining out’ was more stable. Assessed buying conditions softened across the board with all categories showing 3-4% declines.

• While overall the fall in sentiment is not large it again casts doubt about the sustainability of recent improvements. Up until April there appeared to be a convincing upswing in confidence taking hold and spreading from expectations to more tangible improvements in current business activity, buying intentions and labour market conditions. The uptrend has lost its way since then and although consumers continue to report improving business conditions they appear less confident that gains will be sustained and less inclined to spend. Whether Chinese consumer confidence weakens further or regains its upwards momentum in the months ahead will be a critical factor for economic activity, particularly while export sectors and investment activity remain soft.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.