June quarter reports from gold producers are confirming what rampant share prices in the sector have already indicated: the industry is booming.

Northern Star managing director Bill Beament has no doubts: “If you look at the overall Australian gold sector, it is in fantastic shape.

“It is a very exciting time to be a gold producer,’’ Mr Beament said at the release of the group’s June quarter production report.

A combination of strong production, near record local gold prices and cost-cutting saw free cash flow total $64 million.

That took free cash flow to $224.2m for the June year, a 21 per cent increase on the previous year and building Northern Star’s end-of-year cash and equivalents position to $326m, up from $178m a year earlier.

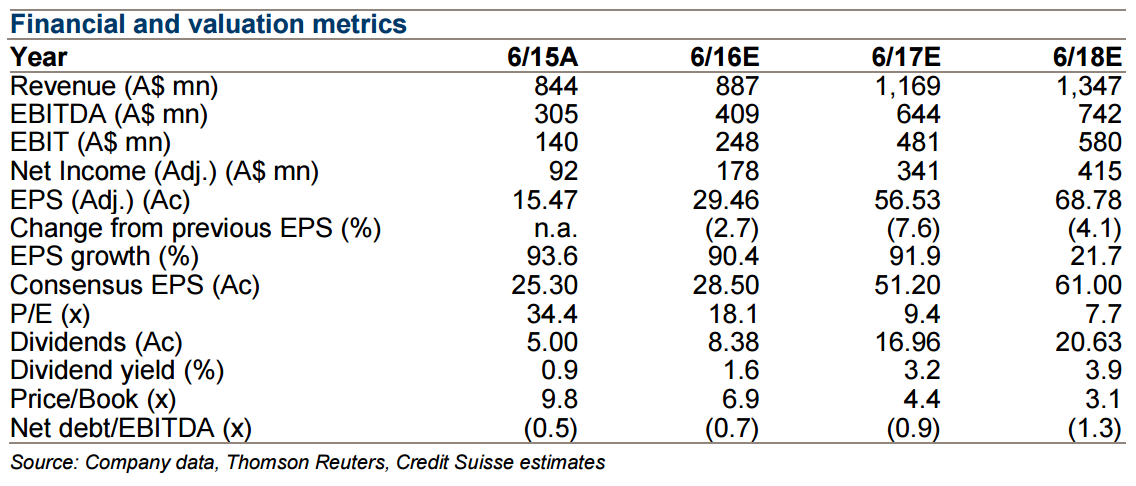

Guff aside, here is Credit Suisse:

Softer JunQ delivers above mid-guidance

■ JunQ 130koz at $1,056/oz AISC, while above mid-guidance, was marginally disappointing, being the weakest quarter by 10koz when consistency (140-145koz/q) was expected, as flexibility improves and PLU performance lifts. MarQ 142koz at $985/oz, DecQ 145.2koz, SepQ 140.2koz totaling 558koz at $1,041/oz, above mid FY16 guidance 535- 570koz but pleasingly below bottom-end of $1,050-$1,100oz AISC guidance.

■ Key strengths: Good cost control—lower AISC achieved than previously delivered from higher production; strong exploration results. The business is generating strong free cash, buoyed by elevated A$gold. JunQ free cash flow $64mn and FY16 A$224mn for net cash of A$326mn.

■ Key weakness: Slow turn around at Plutonic—FY16 64koz <77.5koz guidance. JunQ 17koz makes FY17F 100koz look stretched. Revised FY17 guidance not yet provided. FY17 (30 November 15) guidance for ~600koz at A$1,020/oz, requires a strong Plutonic recovery, consistent Paulsens, Kanowna Belle and Kundana, and stronger Jundee. Flexibility and planning horizon improving but short-term production outcomes are influenced by opportunistic mining of material identified on the run during development.

■ As a softer quarter with little commentary, no new FY17 guidance and outstanding reserves and resources, there is no basis for adjusting FY17 expectation. Current projection requires performance not evident from FY16 or from the JunQ.

■ With Diggers and Dealers approaching, we expect further news flow over ten days, with FY17 guidance, reserves and recent exploration success at Jundee, Kundana and to some extent Kanowna, logically to be a core component of the MD’s presentation and site visit discussion.

■ NST’s premium to our generous stretch valuation is inconsistent with the lack of visibility and reliance on extrapolation of future discoveries assumed in the mine plan. No change to NPV-driven target or Underperform rating.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.