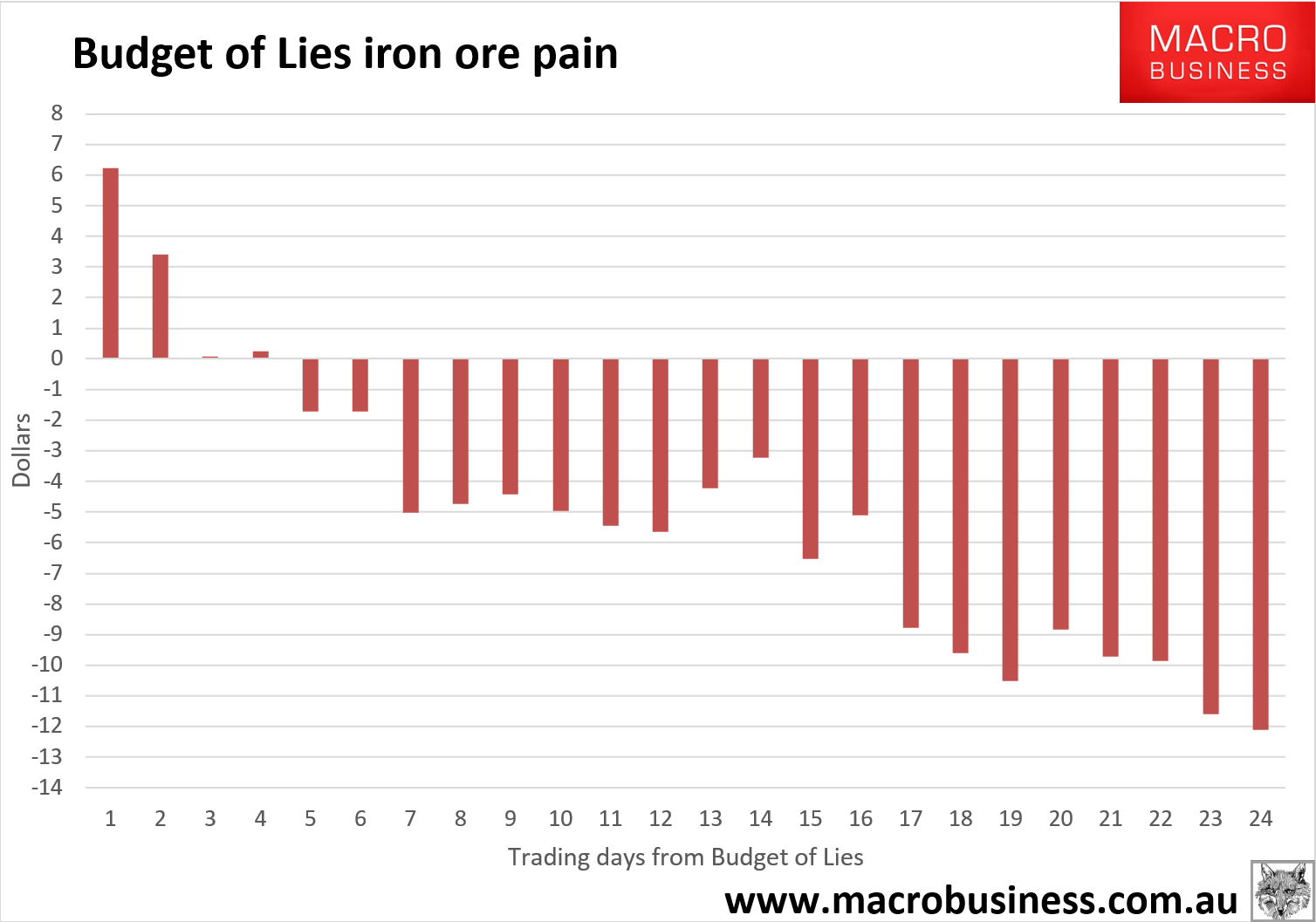

Three days into the 2016/17 Budget of Lies year and the iron ore price is spraying red ink all over it as the outlook for $55 hits the brick wall of a spot price at $42.90:

There’s a little offset in the dollar falling from the Budget of Lies outlook of 77 cents to 72.2 cents but its marginal versus the pace of the iron ore decline.

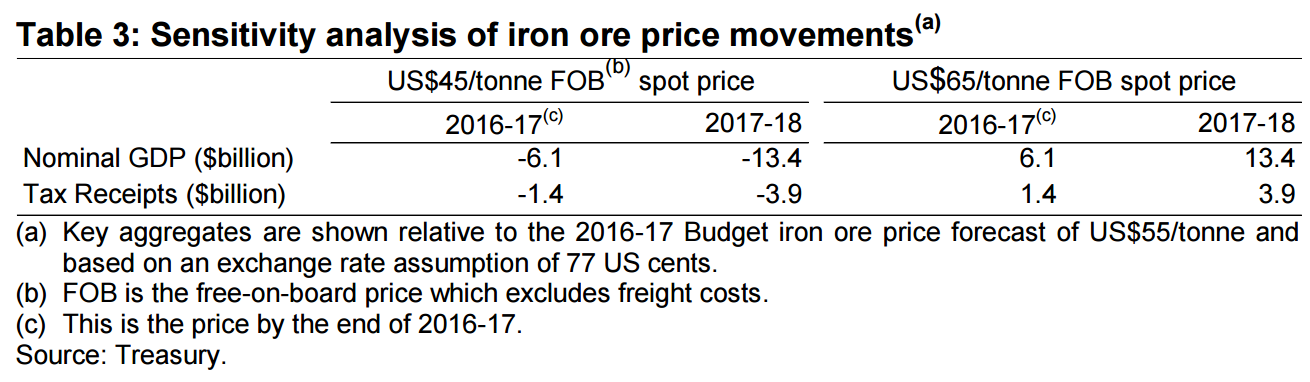

Here is Treasury’s own sensitivity analysis for what this means:

So, on day three of the 2016/17 Budget of Lies, it is behind by roughly -$15bn in nominal GDP and more than -$4bn in revenues.

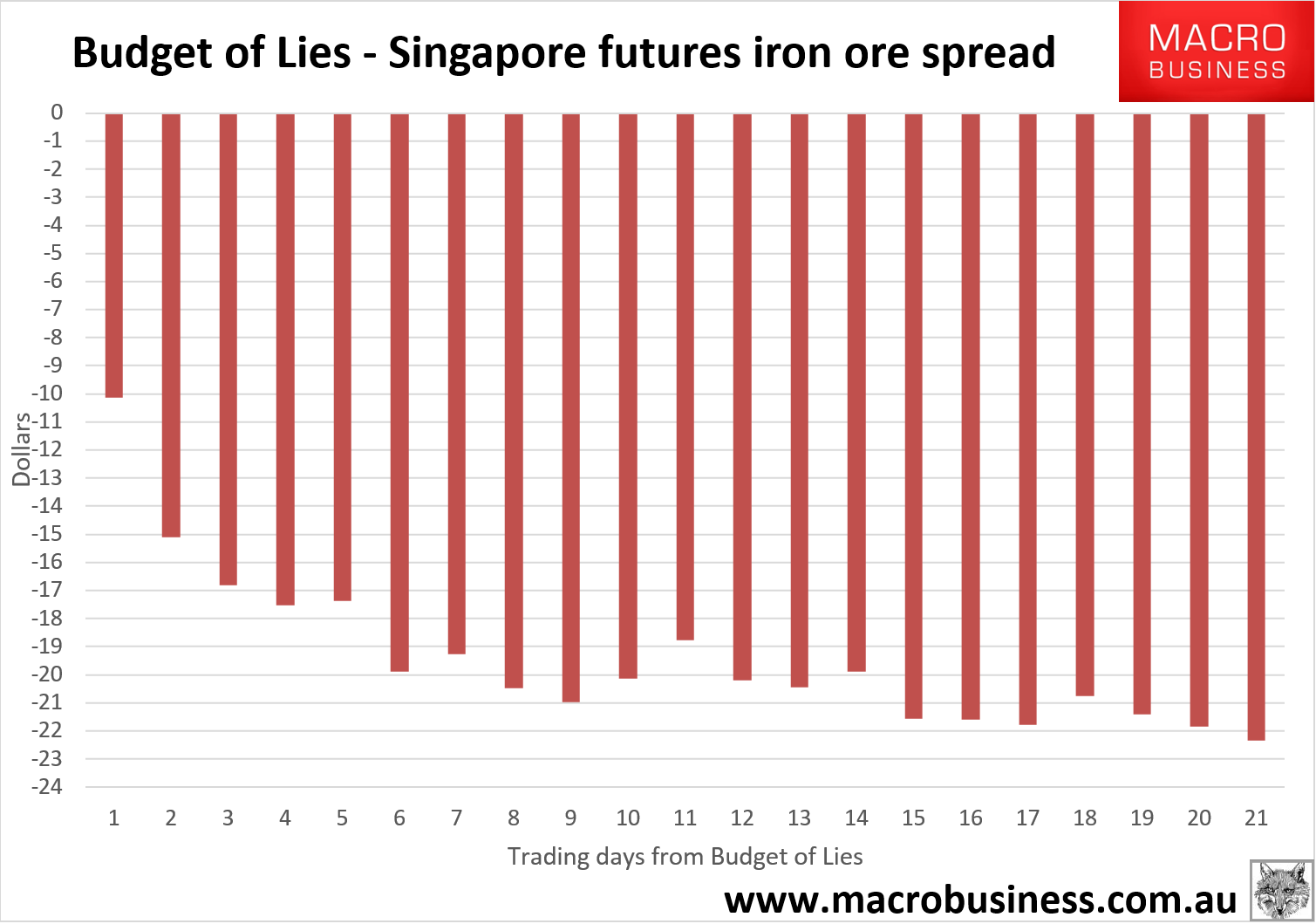

But of course we’re still only on day three and the iron ore price is going to keep sinking. Futures are now forecasting -$22 plus:

I expect that by the election the spread will be out to -$25 per tonne, a full 45% drop on the Treasurer’s fantasy outlook. Taking the most reliable futures market in Singapore, on iron ore alone the Budget is currently mis-pricing nominal GDP by some $27 billion and tax receipts by $8 billion per annum.

But that is only the beginning. Other assumptions are just as bad:

- dwelling investment to grow 2% when we already know it has peaked in ABS data;

- business investment is expected to fall -5% when hard ABS data is already measuring it at -18%;

- wages and demand growth based on 1.6% productivity gains and 2.5% wages growth when the current trend is sharp falls and 1.6% wages growth in the last quarter (and still falling);

- nominal growth is supposed to be 4.25% but when you add the right outlook it falls to 2.5%, the same as this year, at best.

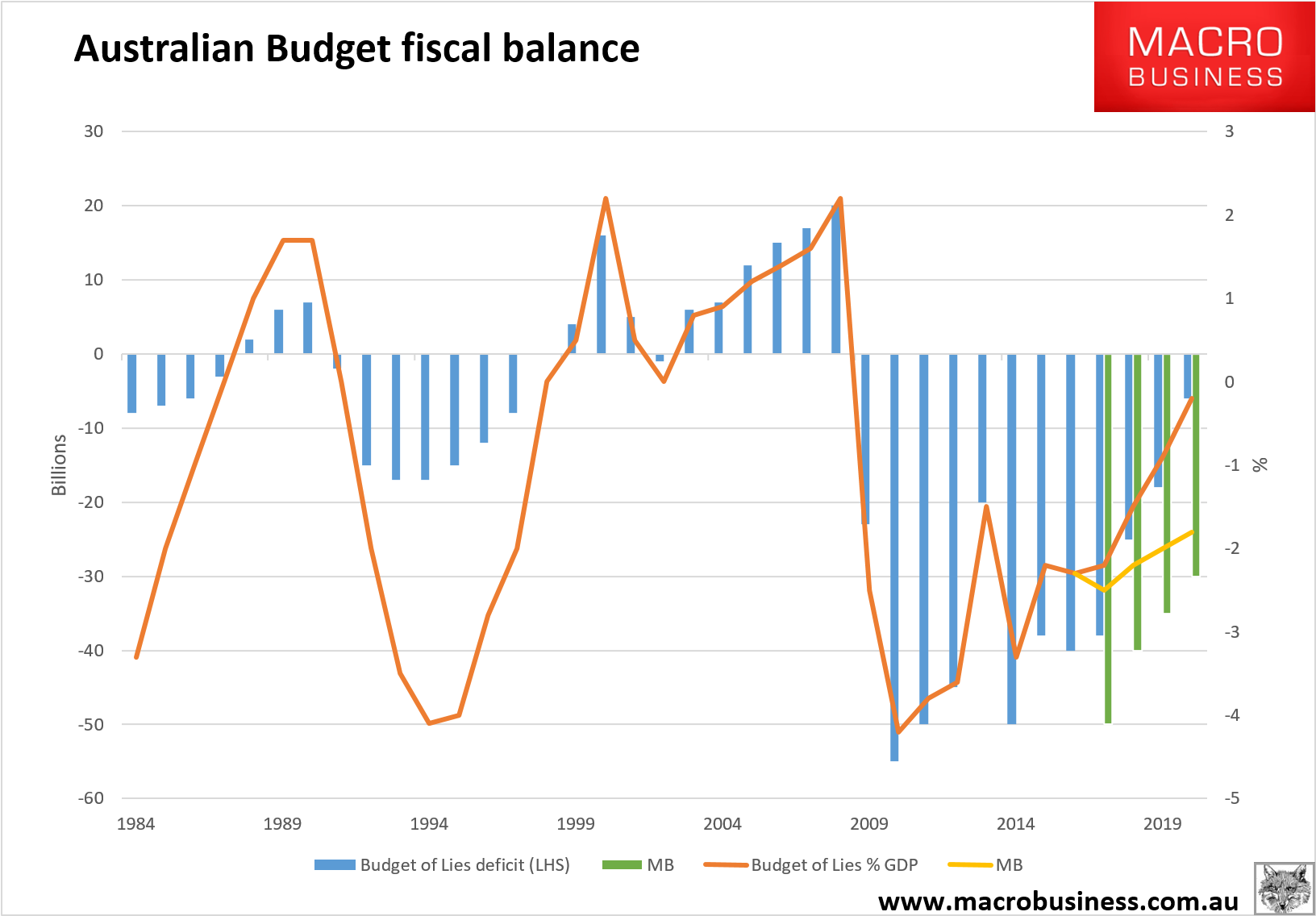

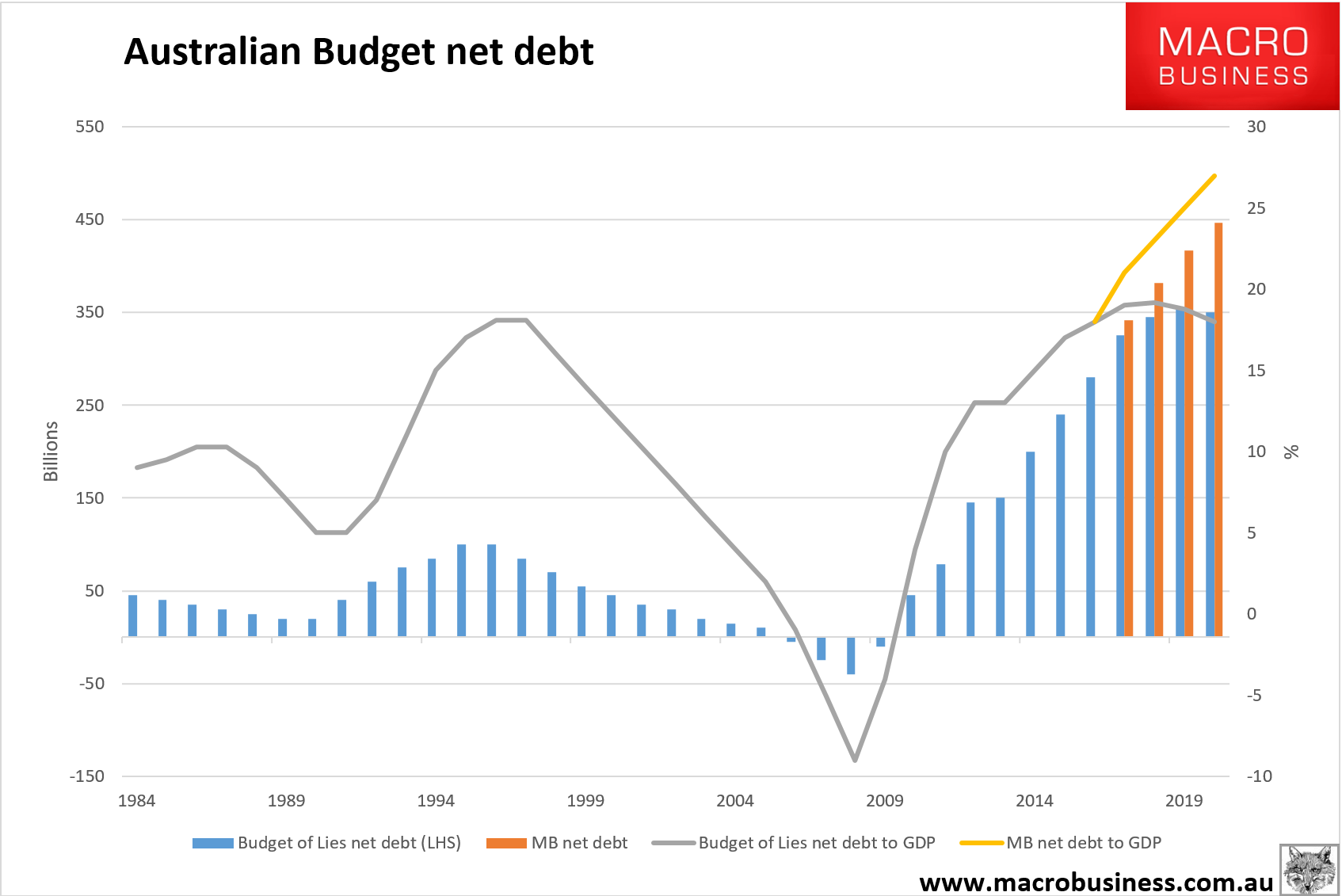

So, the deficit reduction outlook is also a lie. Here’s what the chart looks like when you apply realistic assumptions:

And the net debt outlook as well with realistic assumptions:

There is zero Budget repair underway, and remember that this does not account for any end-of-cycle disruption which is plainly coming well before 2020.

The Budget is a ham-fisted attempt to hoodwink credit ratings agencies and, given even the RBA and Treasury don’t believe the numbers, the CRAs will have no choice but to put Australia on downgrade watch after the election. S&P’s 30% net debt target breach is in plain sight and Moody’s outlook for commodity prices is much the same as MB’s.

The sooner the better quite frankly so we can get on with facing reality.