Chair Yellen’s semi-annual testimony to Congress gave her another opportunity to outline the Committee’s current expectations for the outlook, for the US economy and monetary policy.

The narrative again covered all the key points offered last week in the press conference following the June FOMC meeting.

“Economic growth has been uneven over recent quarters”; and in April and May, “the average pace of job gains slowed to only 80,000 per month” (in part due to the Verizon strike). But “it is important not to overreact to one or two reports, and several other timely indicators of labor market conditions still look favorable”; also, “there are some tentative signs that wage growth may finally be picking up”. Consequently “the recent pickup in household spending, together with underlying conditions that are favorable for growth, lead me to be optimistic that we will see further improvements in the labor market and the economy”.

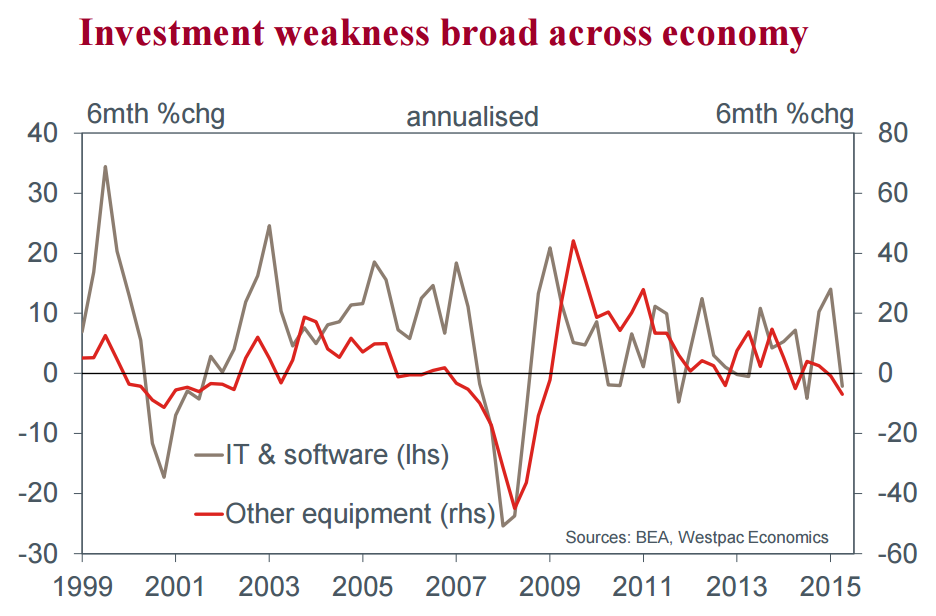

This is a cautious but positive view of the economy, one that could justify further rate hikes over the coming year. One area of the economy that has often been referenced of late but not analysed in detail is business investment.

During the testimony, some further colour was provided. While “the energy sector was [unsurprisingly] hard hit by the steep drop in oil prices since mid- 2014… business investment outside of the energy sector was [also] surprisingly weak”. Together with the “latest readings on the labour market”, “the weak pace of investment illustrate one downside risk– that domestic demand might falter”. This concern vis a vis investment picks up on a longer-term issue previously discussed by Chair Yellen in her address to the ‘The World Affairs Council of Philadelphia’ on 6 June, namely US productivity.

In that address, Chair Yellen asserted that productivity should improve the further we move away from the recession, aiding total output, household incomes and, in time, inflation. However, there is a risk this does not occur. Overnight, Chair Yellen noted “we cannot rule out the possibility expressed by some prominent economists that the slow productivity growth seen in recent years will continue into the future”.

Should this transpire, the longer-run expectations of the FOMC would come under significant pressure. Of greatest importance is that lower potential growth would beget a terminal Fed Funds Rate closer to zero and a much tougher challenge raising the Fed Funds Rate from its current setting to this steady-state level.

So while the FOMC continues to put forward the view that conditions will warrant “gradual increases in the federal funds rate”, it is clear that the risks to this view are heavily skewed.

Against the median expectation of the Committee, two hikes in 2016; three in 2017; and three more in 2018, we expect one in 2016; two in 2017; and one in 2018 – a peak rate of 1.375% versus the FOMC’s 2.375% 2018 figure and their longer-run 3.00%.

The views of the market and 2016 FOMC voter St Louis Federal Reserve President Bullard go further still in emphasising the potential downside. Currently the market has one hike priced in by end-2017 and a high probability of another by end-2018. President Bullard instead sees one near-term hike, but no more to end-2018. All of this is to say that, for an economy growing at trend near the lower bound, the only thing that is certain is uncertainty.

I still expect ‘one and done’ as China derails the Fed in H2.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.