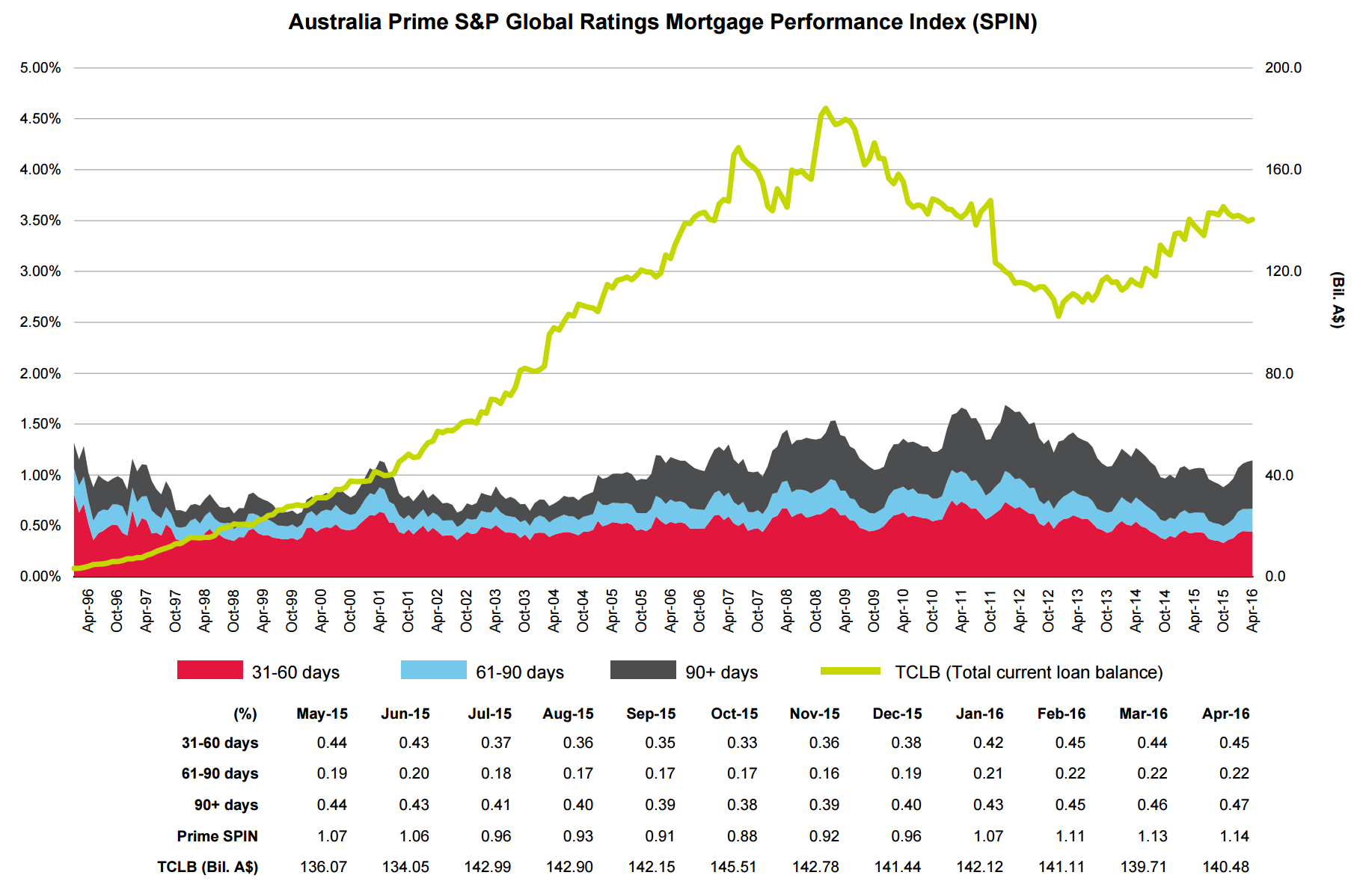

S&P is out with its monthly RMBS arrears data and the news is a little discomforting. S&P puts on a smile:

The number of Australian housing loans in arrears rose for the sixth consecutive month in April for prime residential mortgage-backed securities (RMBS), as measured by Standard & Poor’s Performance Index (SPIN). The prime RMBS SPIN increased to 1.14% in April from 1.13% in March and 1.06% in April 2015, according to S&P Global Ratings’ recently published “RMBS Arrears Statistics: Australia.”

While we have seen increases during the past six months, the April result was below the 1.25% average for prime loans over the past decade. The SPIN for low-documentation loans increased 35 basis points in April to 4.76%, with most of the movement in the 31-60 day and 61-90 day categories. Low-doc loans represent around 1.3% of the total loans outstanding that underlie prime RMBS transactions, down from a peak of 13.2% in January 2008. The SPIN for nonconforming loans increased to 4.25% in April from 4.08% a month earlier.

Most of the increase in arrears was in the 61-90 day arrears category, while 30-60 day arrears declined during the month. The nonconforming measure remains low by historical standards and well below the peak of 17% in 2009. The SPIN measures the weighted-average arrears more than 30 days past due on residential mortgage loans in publicly and privately rated Australian RMBS transactions. The SPIN is calculated for prime and nonconforming residential mortgage loans.

But the headline chart shows that the downtrend is done and we’re now trending higher:

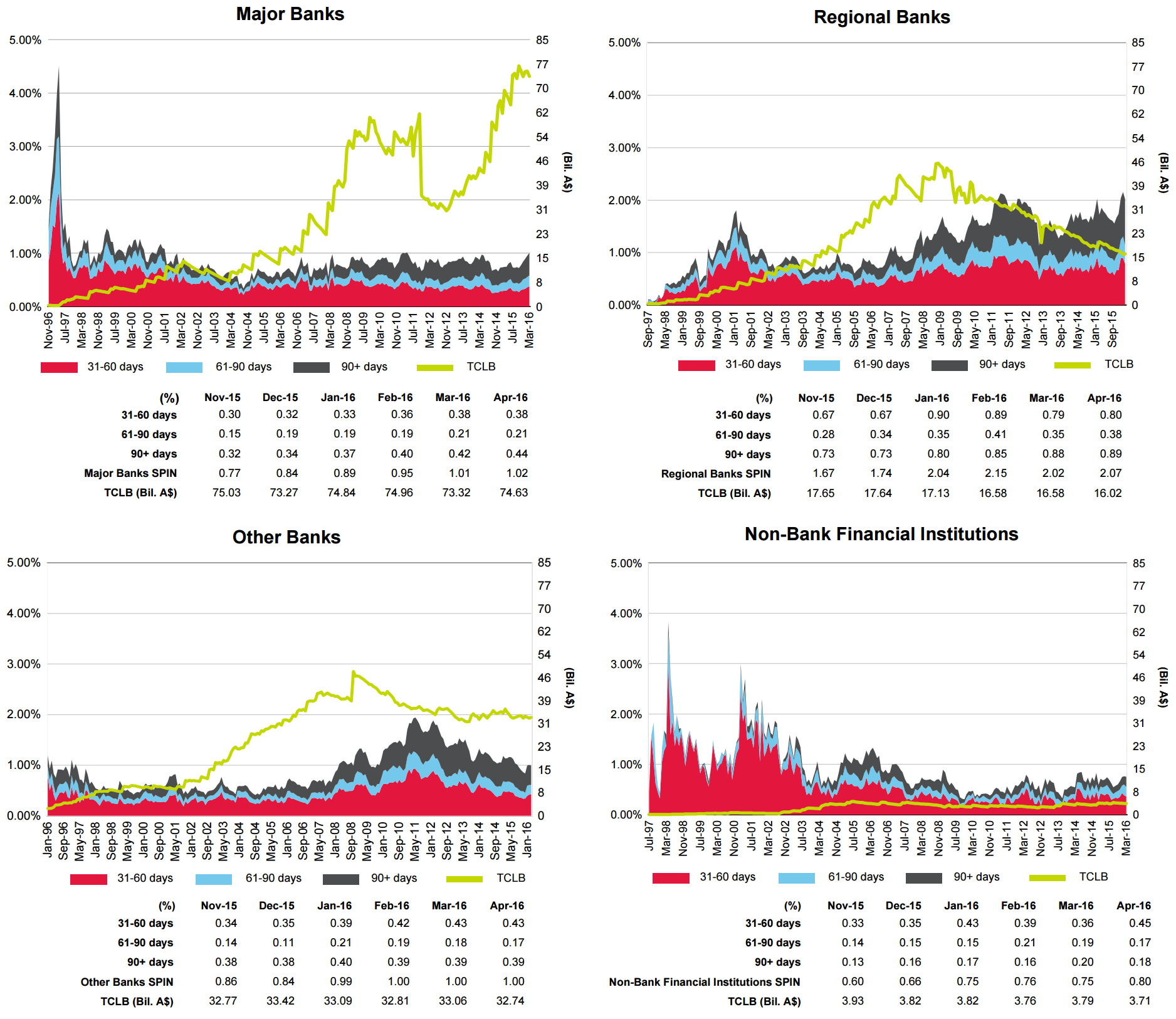

Moreover, major banks are leading the way with arrears at post-GFC highs as regionals wrestle with similar:

The overall metrics are held down by the fading role of yesteryear’s lenders as their mortgage books run down.

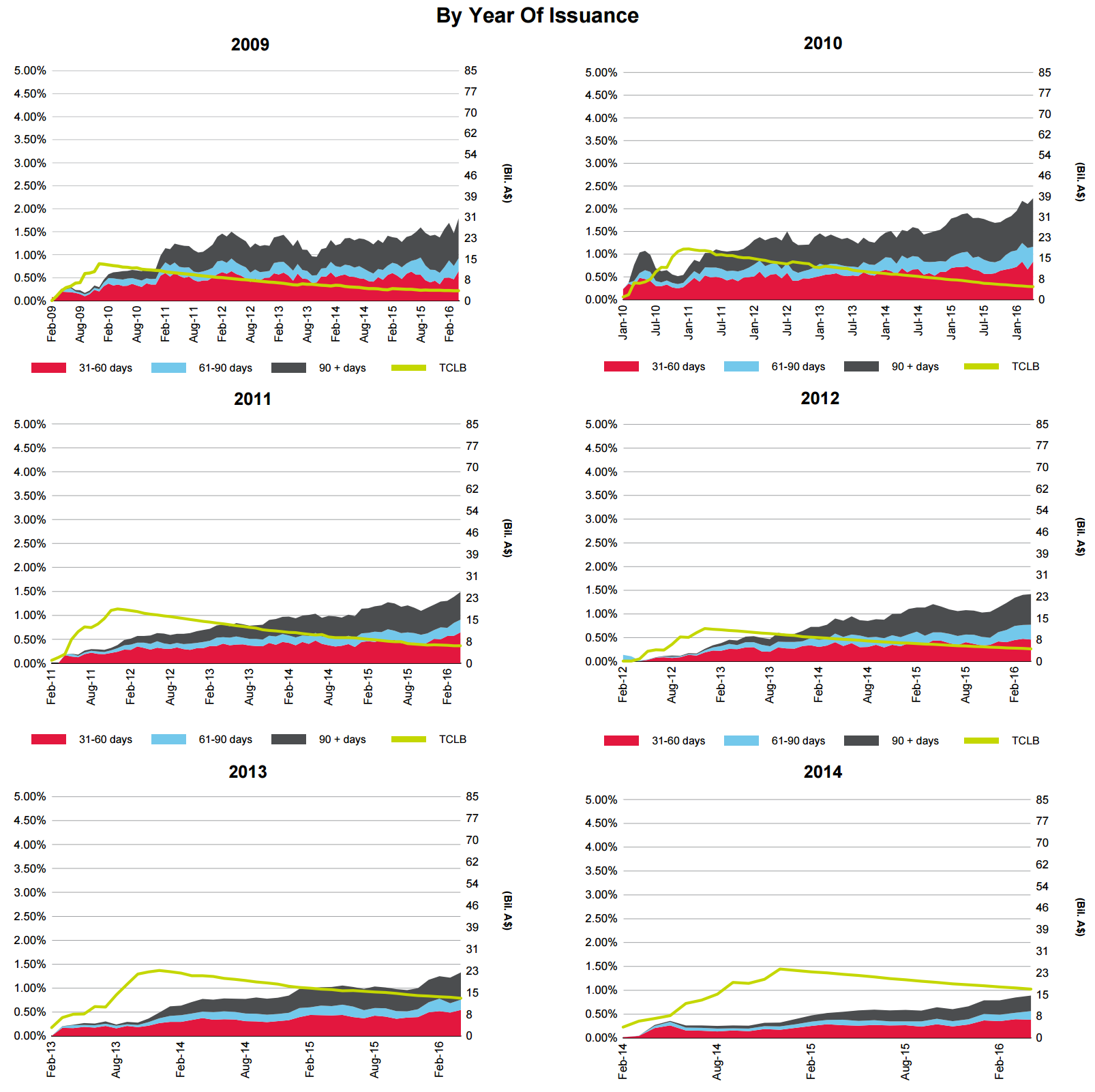

As for mortgage vintages, “Rudd Prime” is leading the way higher but everything is trending up:

The overall level of arrears remains low but there is a clear warning bell in the data for big bank investors given their still huge payout ratios cannot be sustained if we see anything other than the most modest of delinquent loans.