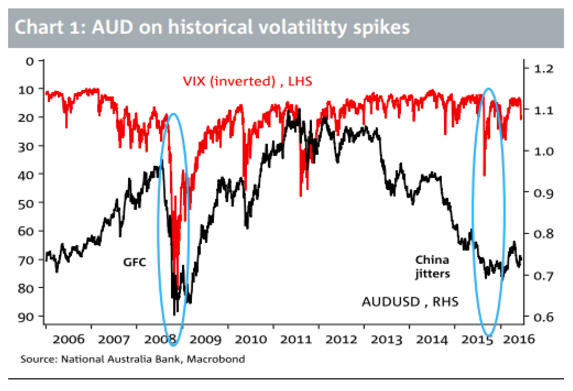

In attempting to quantify the potential implications for the AUD, we note that last August when Chinese stock and currency market-related stresses saw the ‘VIX’ proxy for market risk aversion briefly above 50 from below 20, the AUD fell from above 0.74 to below 0.69.

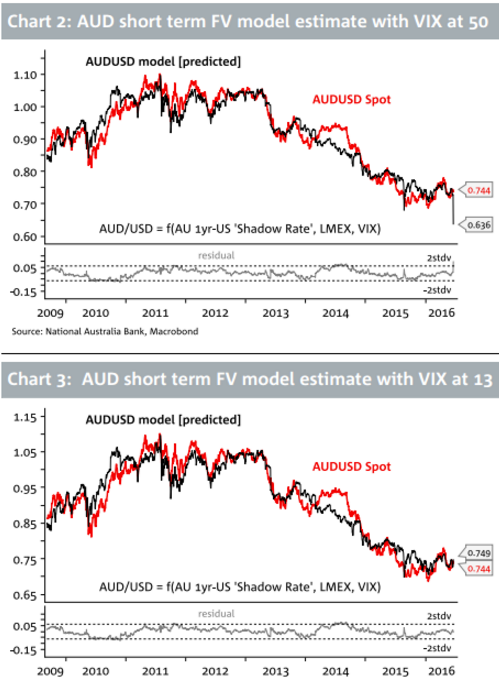

If we go back to the collapse of Lehman brothers when the VIX rose as high as 90, AUD fell from 0.98 to 0.60 (Chart 1). Stressing our short term fair value model with similar levels for the VIX (50 and 90) keeping all else constant, we derive fair value estimates of 0.64 (Chart 2) and 0.52 respectively We’d emphasise these are not forecasts, but do serve to illustrate the potential for severe downward pressure in the event that global risk markets are freaked out by a vote for Brexit.

Our sense is that AUD would quickly revisit the current cycle lows in the 0.68-0.69 area in the case of ‘Brexit’ and rally to 0.75-0.76 (based on current levels) in the case of a vote for ‘Remain’ (Chart 3).

The most important point to take away from this, Brexit or not, is that the Aussie is NOT a safe haven currency.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.