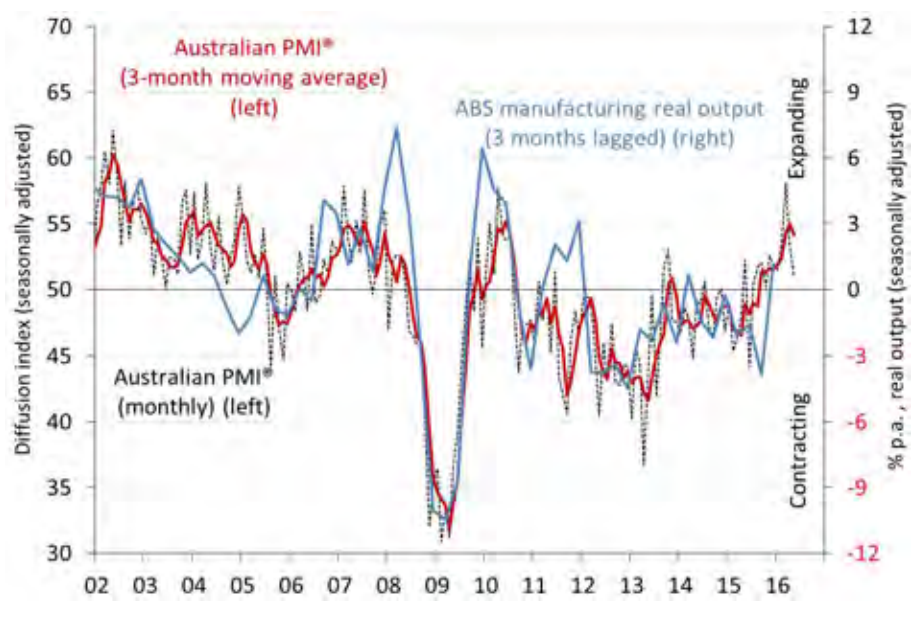

The Australian PMI® expanded for an eleventh straight month in May – the longest unbroken period of growth since September 2006 – despite easing by 2.4 points to 51.0.

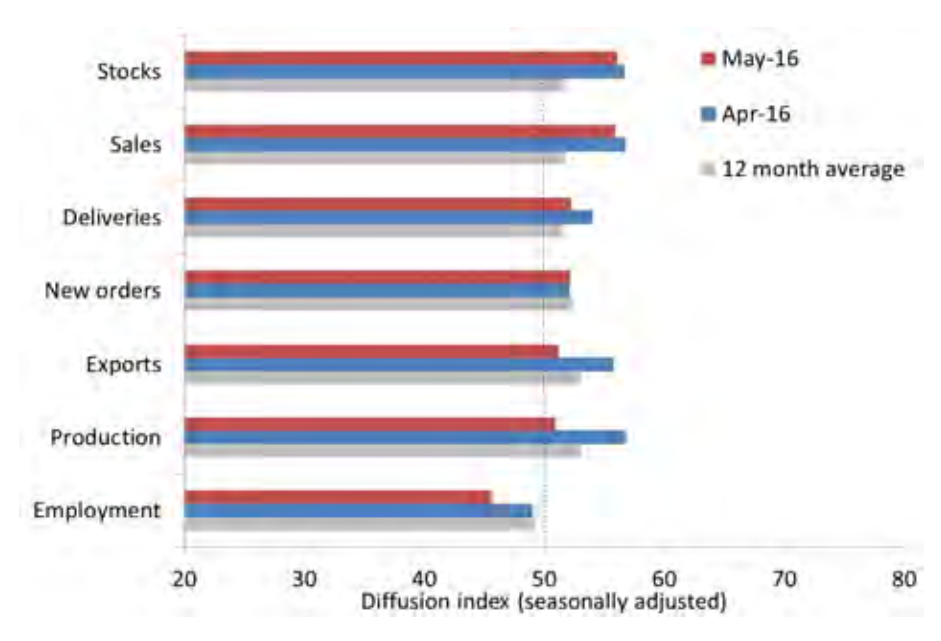

As in April, six of the seven activity sub-indexes expanded in May, although most eased from last month (see table below). The exception, once again, was the employment sub-index (down 3.4 points to 45.6).

Five of the eight manufacturing sub-sectors expanded (that is, above 50 points in three-month moving averages). Food, beverages & tobacco (down 8.8 points to 65.3) and wood & paper products (up 1.9 points to 67.7) remained in strong expansion, as did petroleum & chemicals (up 5.4 points to 59.9).

Printing & recorded media (up 4.1 points to 49.7) and machinery & equipment (up 2.8 points to 50.6) both stabilised, while metal products (up 0.2 points to 44.1) and textiles, clothing & other manufacturing (down 3.9 points to 47.1) contracted in May.

The input prices sub-index increased by 5.9 points in May to 63.2, reversing the easing in input price pressures seen last month. Wages growth strengthened again, rising 3.9 points to 61.3.

The manufacturing selling prices sub-index reversed its recent downward trend, climbing 5.5 points to stabilise at 50.6.

Comments from manufacturers in May indicate some wariness about the potential effects on their business from the upcoming Federal Election. Margins remain tight and competition is aggressive, particularly from overseas businesses. The recent volatility in the Australian dollar is having some adverse effects and input prices continue to climb as a result. Defence spending appears to be lifting activity in some sectors, but drought conditions in some locations are dampening manufacturing activity elsewhere.

That big fall in employment could be election related. It will be interesting to see if it repeated over the other PMIs. Full report.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.