From News:

RETAIL prices have stayed low for a long time. So suspiciously low that the Reserve Bank of Australia (RBA) started to wonder if something had gone wrong.

It did a big investigation which it published last week. The reason they found? Mostly Aldi.

The RBA says we’ve had “a large downward shift in the average rate of retail inflation” that is not explained by labour costs or import costs. It blames technology (the internet) but also competition spurred by new foreign retailers.

Bunnings revealed just this week that even it worries about Aldi. Senior executives say they know lots of people will shop for tools at the discount supermarket, so Bunnings has to respond. Both companies are selling a drill for $89.99 this weekend, for example.

Bunnings has matched Aldi with it’s own cordless drill for $89.99 this week to prevent them getting a hold of the hardware market.Source:Supplied

Aldi is not only lowering prices via direct competition — it is also showing other retailers just how badly Aussies want discounts. That is encouraging Coles and Woolies to slash prices too, even where Aldi is not a big threat.

Here is the bit from the RBA Bulletin recently:

Exchange rate pass-through is usually considered in two stages: from movements in the exchange rate through to the Australian dollar cost of imports (first stage); and from the cost of imports through to final consumer prices (second stage). Since the exchange rate began to depreciate in mid 2013, first-stage pass-through to imports of retail items has been largely consistent with its historical relationship (Graph 5).[6] However, there appears to be a marked divergence between inflation in import prices and final prices for retail goods beginning in 2010.

This divergence may be consistent with a change in second-stage exchange rate pass-through, which would indicate a change in firms’ responses to exchange rate movements. However, as discussed above, there is a range of costs other than imported COGS that contribute to retail inflation within the retail supply chain; movements in these costs could also drive the divergence between import and final prices of retail goods. Hence, the relationship between import price inflation and retail inflation should be tested conditional on movements in the other determinants to assess whether the divergence is a change in second-stage exchange rate pass-through or something else. That is, the effects of movements in the exchange rate need to be disentangled from movements in other costs. This can be done by utilising a basic econometric model of retail inflation.

A pretty marked divergence since 2010. And no doubt Aldi and some other increases in competition have played a role.

But this reeks of the kind of “Australia is different” analysis that dogs everything that the RBA does and Mish Shedlock has a better macro explanation:

Australia consumers are tapped out. Housing costs are absurd and people are struggling.

Aldi is not lowering prices because it wants to. Rather, consumers demand lower prices and are willing to wait for them. Stores have to lower prices if they want sales.

Economist Jason Murphy claims “But all this can only go on for so long. The Aldi effect can’t cause low inflation forever.”

Murphy misses the boat as much as the RBA.

Nothing is forever, especially attitudes. But it is consumer attitudes that are the driving force for low prices, not Aldi.

This attitude change can last for years if not decades. Japan is proof enough.

Once the housing bust really gets going, the RBA just might be shocked at how far off their model is.

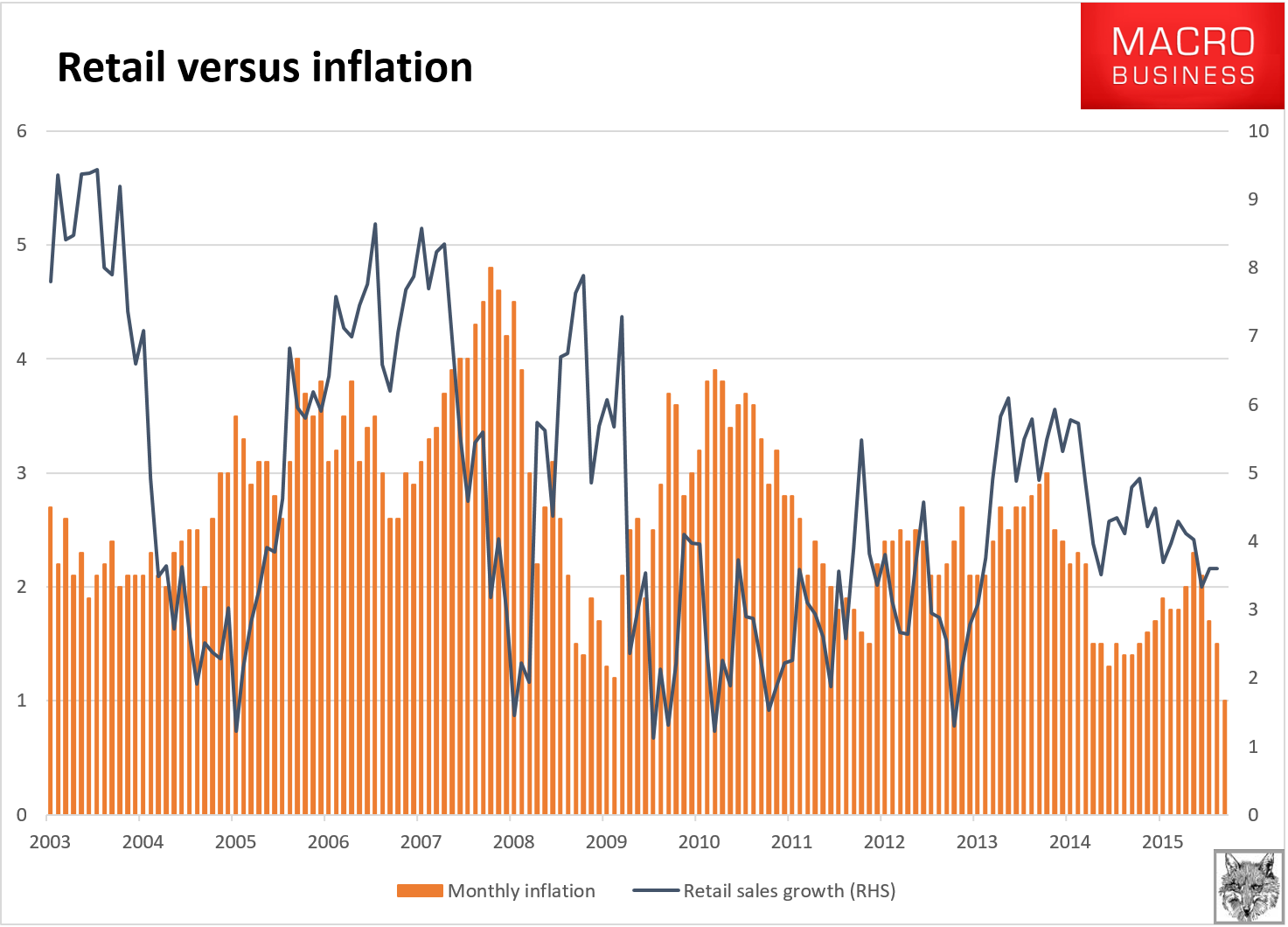

You can take or leave the rhetoric but the basic point is very likely right. Retail sales growth has been trending down since 2010 and so has inflation:

I don’t have the granularity of data to explain the 2009 and 2010 divergences but I’d be willing to bet that they can be explained by the GFC for the first period and the mining boom for the second. That is, ex-retail disinflation and inflation pulses.

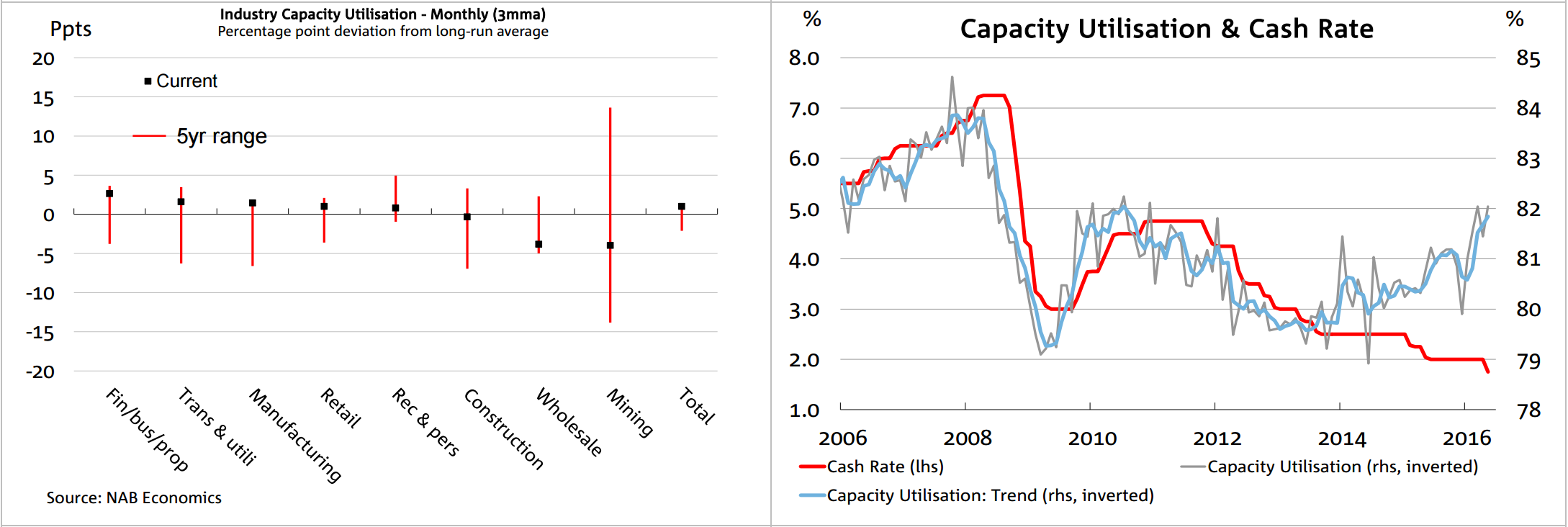

As well, retail has operated with excess capacity for most of the past five years, from the NAB survey:

Demand is much weaker in retail sales than it has been historically. Combine that with weak incomes and the post-GFC savings pulse and it’s no wonder that retail is fighting a market share battle resulting in lowflation.