The Real Estate Investment Trust (REIT) sector is one those Australia success stories that probably doesn’t get the accolades it deserves. REITs are basically an Aussie invention and many oversees markets have tried to copy them. If well managed they are stable, high yielding securities that are a great way to play real estate without the liquidity risk.

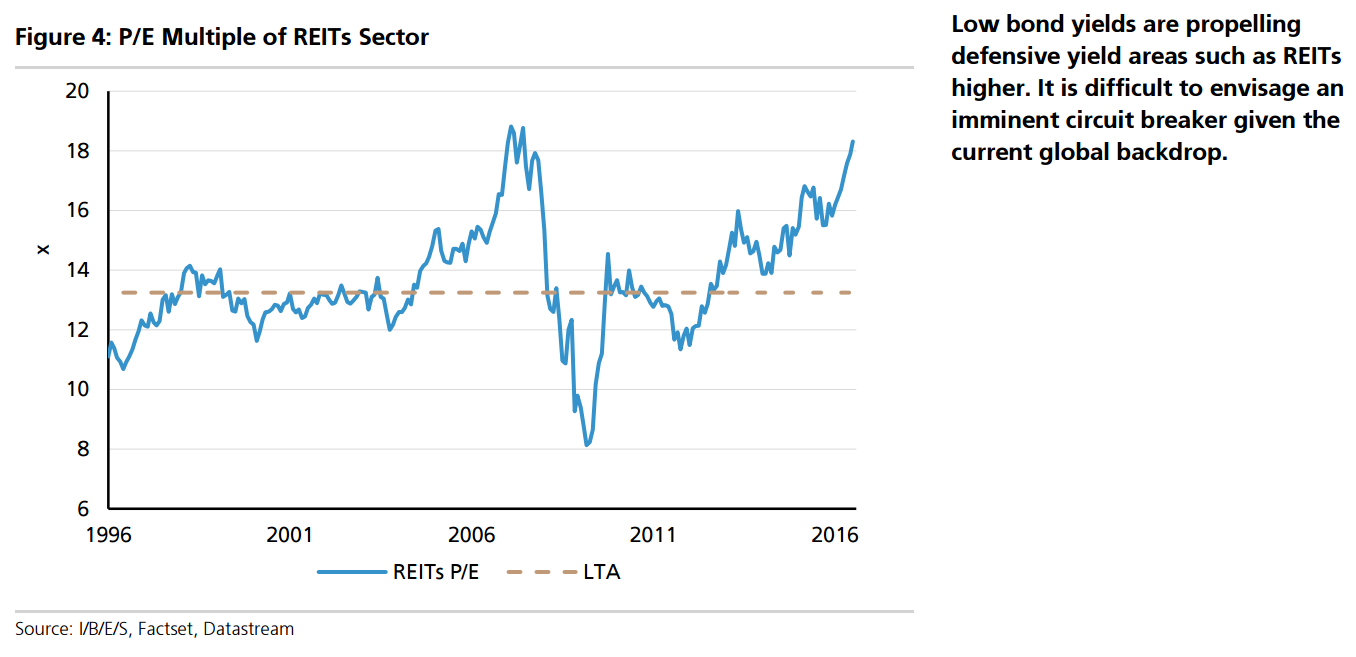

Unfortunately, like the underlying assets, during periods of low interest rates and chases for yiled they are also prone to over-inflation. Like now, from UBS:

Now, there are two ways to look at this. If the inflation in multiples is the result simply of a crashed risk free rate in government bonds then this is not a bubble.

But, if this is an unsustainable inflation based upon easy money that has dislocated from the economic fundamentals and is at risk of implosion then it is a bubble.

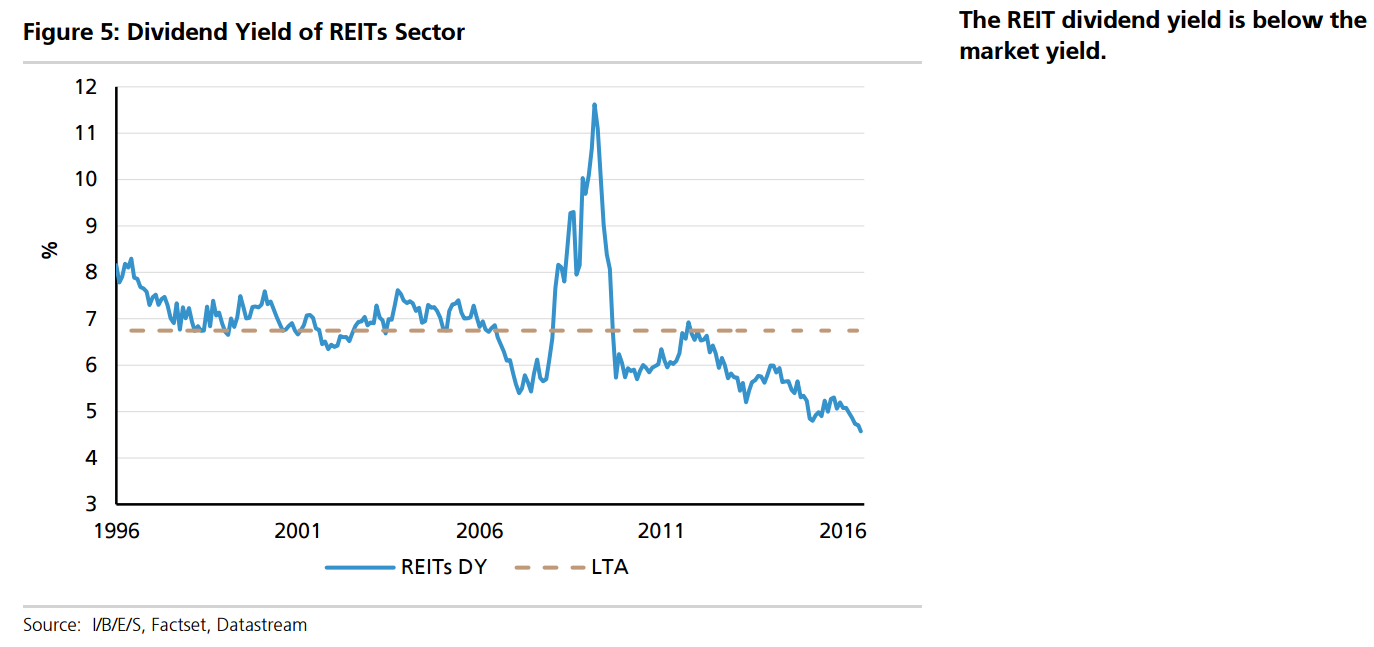

Which is it then? The RBA has warned repeatedly here, here and here for starters. And a few charts show why as yield and capital value diverge:

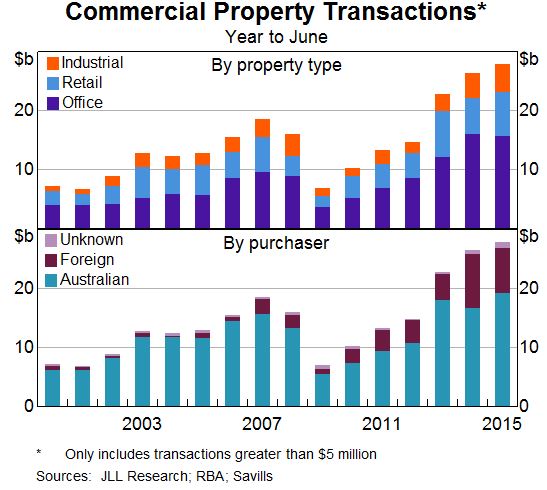

Foreign investors rush in:

And the exposure is concentrated in the big bubble cities:

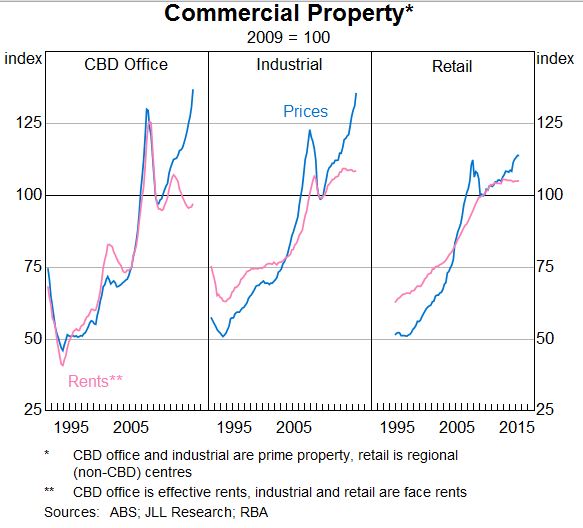

One saving grace may be that much of it is existing property though this chart is a bit old now:

Morgan Stanley still has a 12% rental office growth target for next year and year after which will very clearly be required to close the valuation gap. It is still bearish retail. Sydney and Melbourne office markets are passed their office vacancy peaks but double-digit rental growth clearly relies upon an ongoing bullish out look for these two economies that I do not share given the rollover in apartment market scheduled for year end and increasing international volatility. The development associated with the bubble is Australia’s last great bastion of growth so if it does pop then it will be ugly given the growth singularity that will result.

It is important to remember that when they go, commercial property bubbles go big:

Thus with yields approaching 4.5% my view is that this market is no longer appropriately discounting the risks.