May was a calm-ish month after the recent period of extreme volatility. This was not surprising given the confluence of risk events we have approaching over the coming weeks, including the BoJ, FOMC, ECB, possible Brexit and the Spanish election. The key event of May was the surprisingly hawkish Fed minutes which reopened the possibility of a Fed hike over the coming few meetings. This is in direct contrast to the uber-dovish message we received from Fed Chair Yellen in April and caused the front end of the US yield curve to give up its recent gains.

The picture was altered again early in June as US payrolls printed a seriously weak number and confirmed the growing risk to a slowing economy. While the Fed clearly wants to hike rates now and the rising inflation picture superficially supports this view, our belief continues to be that the US economy is now slowing and the uptick in wages pressures is the counterpart to falling productivity – a late cycle phenomenon. A rate hike now would only have the effect of slowing the economy further and driving the USD higher – the opposite of what the US and world economies need right now.

After the Fed there were two other significant events this month. The first was the rhetoric/ statement from China that it is stepping back from its recent stimulus and that it is ready to embrace more reform. The second was the RBA rate cut. We have been looking, and positioned, for this cut for a while now and generated strong returns when it happened, which helped us outperform strongly in all of our flagship funds over the month. In the RBA SOMP (statement of monetary policy) following the cut the RBA ‘marked to market’ its view and has clearly started the next rate cutting cycle which will take rates to 1% if not lower.

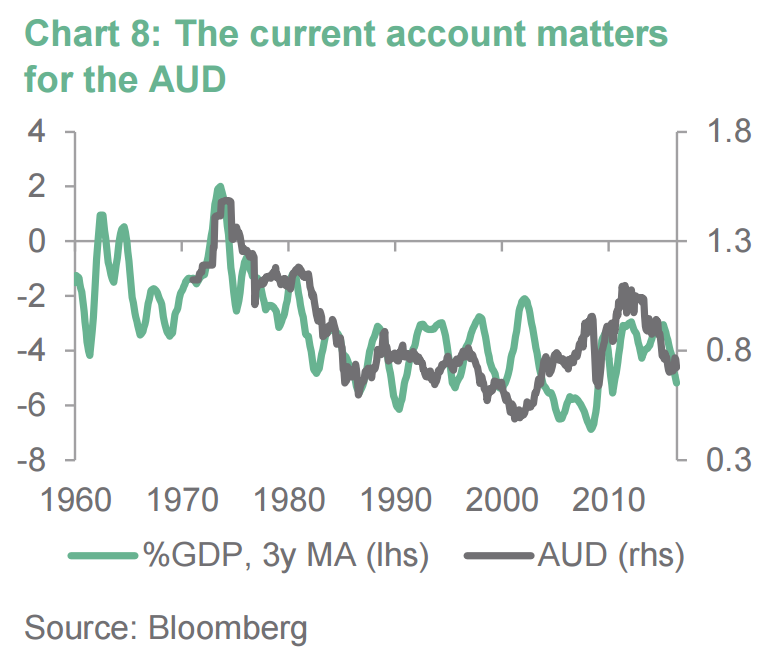

In this Newsletter I want to focus on the recent GDP numbers and the bad, and deteriorating, external situation to show how worrying the picture is for our beloved Aussie Dollar. We had originally thought 50c versus the US Dollar was achievable but our recent analysis highlights that we have been too optimistic and that 40c is now our base case.

Monetary policy 1; fiscal policy 0

Last month’s Newsletter highlighted the problems central banks have when trying to fix the underlying issues in the global economy by just using monetary policy. The aggressiveness of policy easing is one of the best examples of ‘Maslow’s hammer’, or more commonly: “if all you have is a hammer, everything looks like a nail”. While global central banks have seen the weakness in the global economy for what it is and correctly eased monetary policy, the tools available to central banks are few and limited in scope.

The RBA took its turn and pounded its hammer in early May, and in our opinion will follow with many more cuts in the next year to take the official interest rate to at least 1%, if not lower. I argued last month though that this may not end up having the desired effect to lift inflation back into the RBA’s band. In this world of competitive currency devaluations the race to zero interest rates is inevitable and, to extend the analogy, if you have any nails left in your nail gun you have no choice but to fire them even if you have no chance of stopping the strong winds of deflation ripping your roof clean off.

Over-extended analogies aside, while we expect the RBA will be forced to cut rates to keep up with the rest of the world, low rates in an economy like Australia will genuinely be a test of the stability of an economy that has a very specific relationship with the rest of the world. This relationship has become one of ever increasing reliance on foreign capital to continue to do business, and allow us to live beyond our means. When the commodity boom was in full force everyone wanted to be Australia’s best friend, but since the commodity boom ended with a whimper in 2014 Australia has become the little weedy kid no one wants on their team.

Paying away the gains

This reliance on foreign capital has come about because economic growth in Australian Dollars has been so weak for a number of years even as real economic growth continues to show some pretty encouraging headline numbers (Australian GDP last week printed a developed world-beating 3.1% on the year), yet we keep sending this growth overseas through high imports and paying out on past borrowings. This trend has deteriorated in the last year meaning we have to borrow from and sell assets to the rest of the world at a new, faster pace.

This reliance on outside capital to fund our lavish lifestyle, which is still stuck in 2006, puts us in a very different situation to pretty much every country that is currently running a zero or negative interest rate policy. These countries are generally exporting capital because of extremely strong export performance (or weak imports, or a combination of both) and are encouraging capital outflows because of the ultra-low rates available at home. Low interest rates in this situation have had a far smaller effect on allowing currencies to fall as much as some central banks have hoped (with the Euro and the ECB being the classic example), but the unique combination of a large and increasing reliance on foreign capital and fast falling interest rates means that the Australian Dollar is at far more risk than most people think.

A shock downside could easily see it move to 40c against the US Dollar if current trends continue, commodities fall to lows again and economic growth deteriorates. This is a highly likely outcome given the weakness in the composition of the latest GDP numbers.

Inside the balance of payments

Economists measure this reliance on foreign capital through the “balance of payments”. It can be an extremely dry topic because it’s hard to understand and analyse, but when looked at from a helicopter height it can give a lot of insight about the health of our country and its economic relationship with the outside world. It is similar to the financial accounts of a company in that it describes ‘why’ capital is moving across our border overseas (similar to a profit and loss statement), and ‘how’ this change is being funded/invested (the balance sheet of a company). The ‘why’ is made up primarily of two components – the trade balance and the flow of income.

When looking at the ‘why’ side of the accounts (otherwise known as the current account) the trade balance is the easiest to understand, being the difference between exports and imports at any point in time. If we import far more than we export (which is the case at the moment and it’s getting worse) we need to fund these purchases by either borrowing www.btim.com.au 3 money and running up debt, or by selling assets. The flow of income includes the difference between the income earned (this includes coupons, dividends and profits) by Australians owning overseas assets versus foreigners holding our assets. This measure has traditionally also been negative for Australia, meaning we are paying out far more to foreigners than we receive through our investments overseas.

Since both of these numbers are negative the ‘why’ is describing what is called a “current account deficit”’ it tells us about a country that is spending more than it is earning. This isn’t necessarily a bad thing, within reason. It is positive if prior borrowing that we are now paying interest on was invested well and produced returns above the servicing cost, but not so much if it was just ploughed into the existing stock of housing.

This leads us to the ‘how’ side of the accounts (otherwise known as the capital account). This part describes how the earnings/ spending of the ‘why’ side gets funded. If the current account is in deficit then the flows going out of the country will need to be funded from somewhere overseas to counter that outward flow. A company would have to do this by raising debt or issuing new equity; the options for an entire country are fairly similar. The main options are that we can choose to sell assets (foreign direct investment) or raise debt (either through the government running up debt or banks/ corporates borrowing from overseas). The capital account is another way of describing the difference between investment and saving within an economy. If the current account is perfectly balanced then no money is flowing in and out of the country. Investment and saving is matched domestically as no capital is needed from outside of the country. At last measure the Australian current account deficit was more than 5% of GDP. This is on par with the largest deficits seen at the more testing times for the Australian economy throughout the ‘80s and ‘90s, but under the debt-fuelled binge in the commodities boom of 2003 to 2007.

Australia takes a BOP to the head

The deterioration started a year ago as net trade and income payments to the rest of the world worsened with falling commodity prices. This is even during a time when real net exports are making up all the economic growth in Australia, and it shows how powerful the effect is of falling export prices is on the welfare of our economy. Right now it is the main story in describing how money flows into and out of the country. A recovery in the current account deficit tends to only be associated with economic weakness and recession as demand for imports weakens. The alternative is a much lower currency, but this brings about its own stability problems.

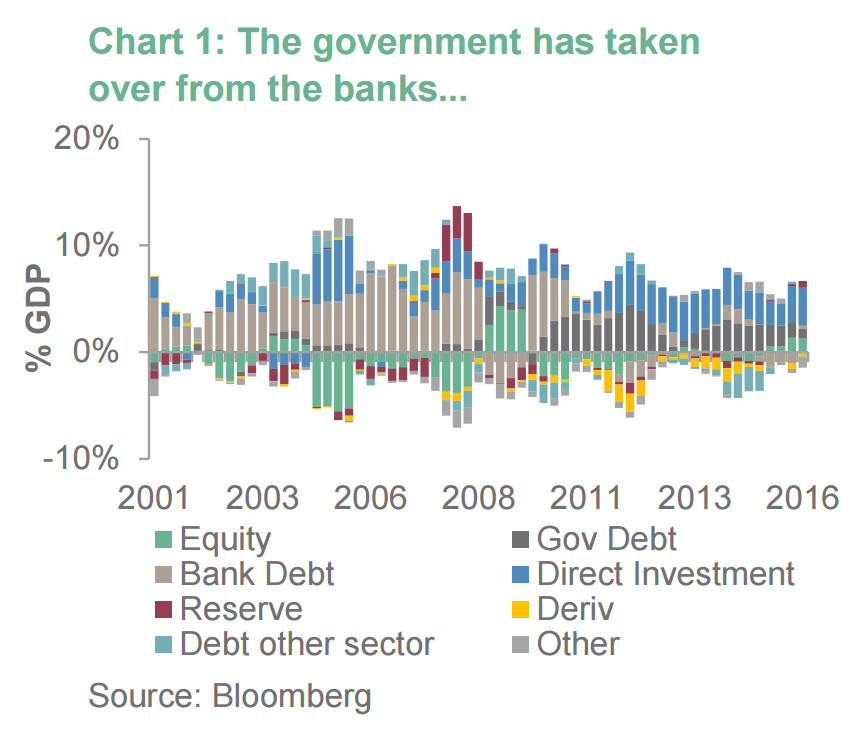

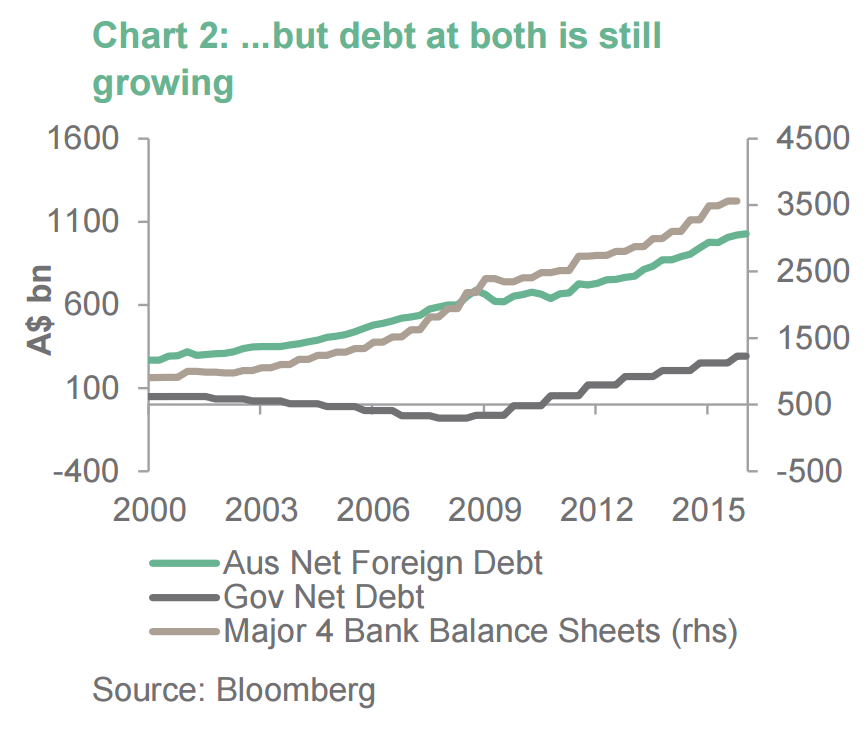

So if the current account is in deficit by more than 5% of GDP, collectively as a nation we have to raise this amount of capital from overseas to net the flow. In the commodity boom times the banks did this by borrowing a massive amount of money, mostly in the form of long-term bank bonds, from foreign markets. This grew the banking system to the massive size you see it today. To get away with this we effectively borrowed against the windfall of rising commodity prices, essentially acting as if they would last forever. This money went straight into house prices in Australia with housing credit growing at up to 20% every year. The income windfall from rising commodity prices was spent as quickly as we earned it. The balance sheets of CBA, Westpac and NAB more than doubled from 2003 to 2008, and foreigners were more than happy to oblige.

This led to a record net foreign liability claim of 67% of GDP in the most recent balance of payments data. To put this 67% number into context, the IMF consider the 50% mark as the point at which the financial stability of a country comes into question. We are obviously well past that mark.

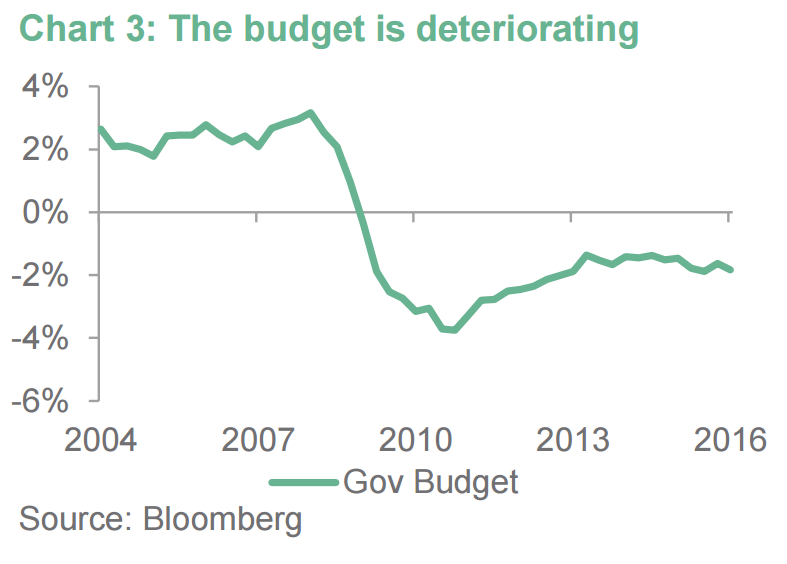

The GFC put an end to this largesse – somewhat – and brought the current account back to around 3.5% of GDP. Commodity prices rose again in the commodity boom Mark II from 2010 onwards and it helped bring our trade balance back to surplus which has normally only been associated with recessions in the past. This period however was also defined by deleveraging of banks and the emergence of the government (at both the state and federal level) becoming a borrower for the first time in a decade. The budget hole opened up during the GFC has never been successfully closed, no matter how much forward budget estimates say that we are going to return to surplus.

The second deficit – the Budget

The status of the budget deficit, surely a point of frustration for our more conservative readers, is resulting in a record projected year of issuance of Commonwealth Government bonds at around $72 billion, or above 4% of GDP. This translates to more than $2 billion per available week of new issuance, requiring foreign central banks and funds to participate consistently to fund this deficit. Plans are to increase the issuance at the super long end of the yield curve as well, introducing bonds that mature well past 2040.

The first sign of disinterest has been evident at this part of the curve. Even though yield curves have flattened in nearly every market in the world our long bonds are steepening relative to 10 year bonds. A lot can be put down to a number of external influences but the fact remains that the market has been demanding more for these long dated bonds because even a yield that is well above a number of other markets isn’t sufficient for the extra risk. It is also likely that the amount of issuance in this part of the curve will increase further to fund new infrastructure initiatives, and therefore we believe this relative pricing move has got more room to move. We are short this part of the curve.

Foreign direct investment became another funding source in more recent years. As we have discussed when looking at the US shale revolution in a prior monthly commentary, a huge amount of investment went into expanding supply of commodities as rates went to zero everywhere around the world. Australia received significant inward investment during this period by foreign owned companies investing in large projects such as LNG and iron ore. This investment was associated with rising imports as the capital goods needed came in from overseas, but a considerable amount of the investment from overseas was used to fund spending in other areas of the economy.

This direct investment is still coming through, and has been supported more recently by foreign buying of residential property. However, as mining capex reduces, this funding source will dry up. It is usually associated with future income flow out of the country as these investments pay their owners back. Not great news.

Twin deficits theory – the new Lazarus

The big issue with the large twin deficits (budget & current account) is that they are putting Australia’s AAA rating under pressure and this rating is likely to be put under review in the next few months. Debt at the government level has obviously risen quickly since the GFC, with future prospects for a contraction in the budget deficit looking grim.

The level of foreign capital needed to support the current account deficit is a clear weak point as well. A downward move in the rating to AA+ will still leave us as one of the highest rated countries in the world. But the move, at the margin, will make the debt of the government and more importantly the banks less desirable than it was before. A downgrade to the sovereign rating would see the banks likely moved down one notch as well, from AA- to A+ for the majors. This will drop their short-term debt out of the important rating of A1+ (the highest bracket for short-term debt), meaning it will be harder to find a buyer for this type of debt, particularly in markets such as the US and Europe where regulation around money market funds is changing substantially to make them safer. These moves will impact the Big 4 as it will make the cost of funding greater and place further pressure on their margins, other things being equal.

However, a current account deficit isn’t always a bad thing. In a lot of cases it is better than a surplus if the surplus leads you to lend to countries that you don’t really want to have exposure to, such as Germany to the PIIGS. Large surpluses/deficits shouldn’t exist if everyone had a proper floating currency as any large persistent flows would move currencies to balance competitiveness. On the other hand, though, borrowing too much through a large deficit from the rest of the world will eventually lead you to a point where you go ‘bust’, further digging yourself into a hole (funnily enough Australia dug enough holes to put itself into this hole).

Bank, and now government borrowing, is allowing us to live beyond our means as a nation. The borrowing we did in the early 2000s was OK given how fast our income was growing at the time. Unlike a promotion with an increased salary, the commodity prices that supported this income growth weren’t forever. So as these prices have fallen, our ability to support a current account deficit that is just as big as it was pre-crisis has fallen and we are now borrowing more than we are earning. This is a really poor and highly worrying trend.

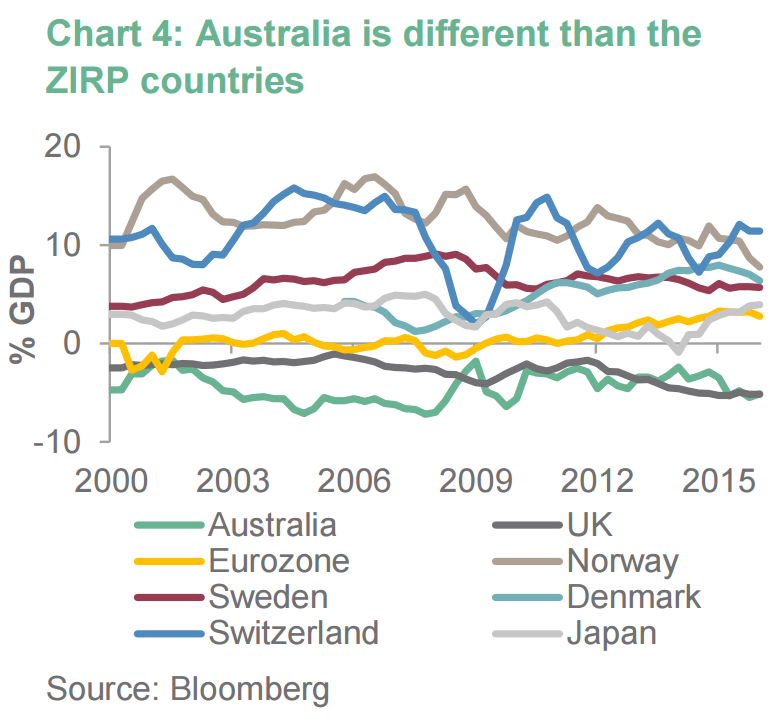

The dynamics for the external balance aren’t very positive, and this is at a time when the spread of Australian interest rates is at a low to the G4. The move towards zero for the RBA will be the first for a country so reliant on foreign capital. Europe, Norway, Sweden, Denmark, Switzerland, Japan all have big current account surpluses, meaning that they have no requirement to access capital from anywhere else in the world. This partly explains why they’ve had to cut rates so much, but also explains how they’ve been able to do it.

The exceptions to this current account surplus rule have been the US and the UK. While technically these economies didn’t get their rates to zero, they got close enough to warrant analysing them. The US enjoys the benefit of “exorbitant privilege” where they have very little choice but to run a current account deficit as they are the world’s reserve currency.

The UK cut rates before their current account was as negative as ours is now, but since that point in time things have deteriorated significantly. While the UK trade balance is doing OK, especially relative to our own one domestically, the income balance is falling rapidly. There are a number of reasons for this which mostly circle around foreign ownership of large companies in the UK paying out profits, while large UK companies having very poor performance in mainland Europe.

This extremely large current account deficit (at the same size as Australia’s at more than 5% of GDP) makes a Brexit even more perilous for the UK. The current account deficit needs to be funded. If a Brexit occurs that funding source may dry up while uncertainty rules about the status of the UK as it transitions out of the Union. This makes the high stakes of June 24th even greater for the global market, and the Brexit campaign is gaining steam again as I write.

Canucks no schmucks

Canada represents, in some ways, the antithesis of the historical government budgetary response as experienced in Australia. While Canada isn’t at zero rates, the target of 0.5% offers a realistic target for the RBA over the next two years, especially if commodities find a new low or China has a real misstep. Interesting parallels can be drawn from their experience, given that they are a very similar country in a number of ways, including their reliance on commodity markets for growth.

Canada cut rates in late 2008 with the rest of the world to 0.5% just as Lehman went under and oil prices briefly traded at $40. Immediately after this the current account deficit moved from being in surplus to deficit and hasn’t recovered since. Most of this is attributable to oil prices cratering of course, but this happened to Australia too. The Canadians are in a far better situation than Australia though, and it’s a result of restraint in the past rather than any choices available to Canada today.

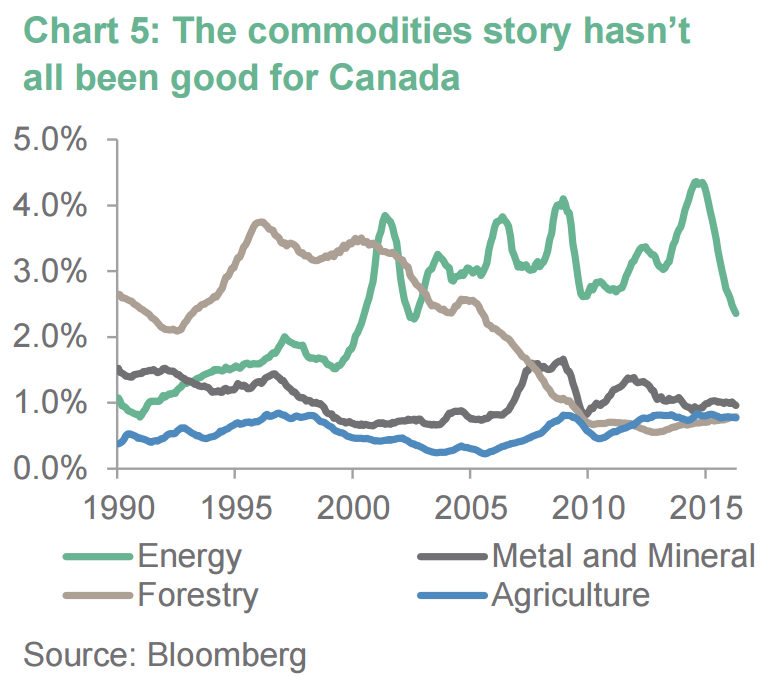

The key difference was that Canada didn’t borrow against the windfall given by rising commodity prices through the strong days in the 2000s, choosing to take the income gains from rising commodity prices and become a creditor to the rest of the world. As a result while Australia owes the rest of the world debts totalling 67% of GDP, Canada is in a situation where the world owes them 15% of GDP and not the other way around. This saving has meant that they are in a far better position to weather a large downturn in commodity prices while the rest of the economy rebalances away from the positive income effect from the temporary boom.

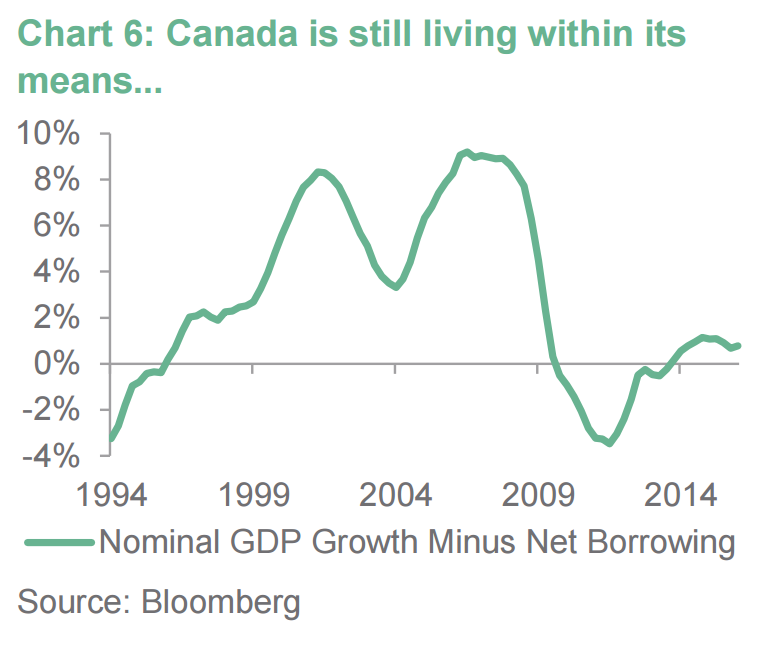

This can be shown by looking at the chart of growth in national income versus external borrowing. This chart for Canada shows a considerable amount of ‘saving’ in the boom years, sometimes above 8% of GDP. This saving managed to happen at a time also when demand for other commodities in Canada such as timber was decreasing rapidly, offsetting much of this gain. This has led to Canada being able to support a current account deficit without having to borrow against future income.

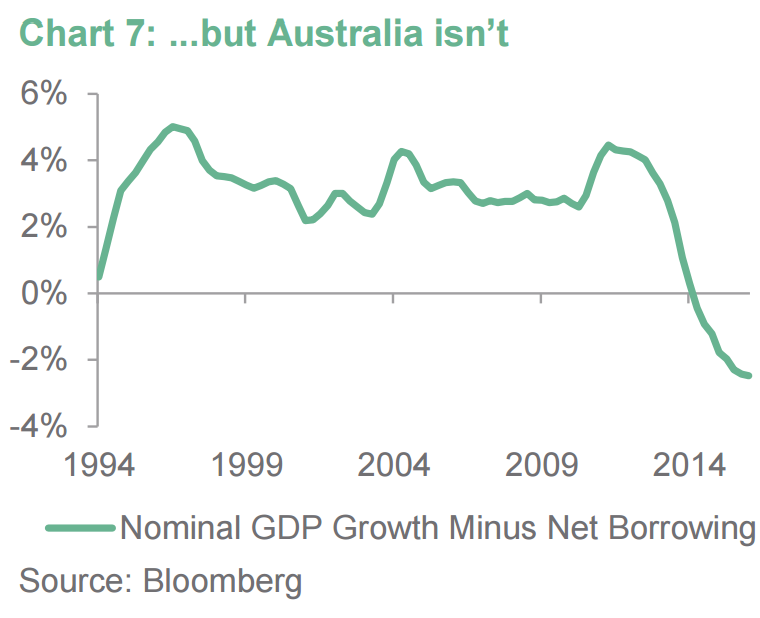

The Canadian example shows how irresponsible Australia was during those times. Australia is now living beyond our means, borrowing from the future, and our past decisions to lever up on what was a temporary situation to create a “structural deficit”. The chart below highlights how little we saved and how much was squandered during that period of time. The same chart shows far smaller saving in the boom years (~3%), but now shows how much we are now borrowing from the future. This borrowing is being done almost entirely by the government sector.

The bad news

The read through from all of this is that we are in more than a little bit of trouble. Ideally to fix it we would have to:

1. Fix the trade balance by cutting imports and save;

2. De-lever by paying back all the debt we’ve borrowed.

Both items are clearly damaging in terms of economic growth domestically, as they both essentially involve giving back all that we’ve taken in previous years. The more realistic outcome is that, as the RBA cuts interest rates and the spread to the US gets smaller and smaller (and maybe negative) we will find it harder to attract the capital that we need just to ‘keep the lights on’, which will result in an Australian Dollar that falls far further than a lot of people expect.

Economists have forecasts for the AUD at 75c in 2018 (according to Bloomberg). This will have to be far lower if questions about funding become an issue, and we will be treated like an emerging market rather than part of the developed market club. An AUD at 40c would force much lower imports and higher exports and will start the necessary rebalancing.

Admittedly borrowing in the near future will be done by the best borrower in the country – the Australian Federal government – so the risk of such a move is low in the short-term. Right now that entity is rated at AAA, but that will likely change soon. We can see no clear path back to surplus for the government any time soon as tightening fiscal policy is highly unlikely given the backdrop of a flagging economy. The day to tighten belts will have to come some time, absent a growth miracle. In the world environment that we find ourselves in twin deficits are a really big problem and one that we should try to avoid at all costs. Our external balance and an RBA cutting rates aggressively might be the trigger to force some hard decisions given our extremely poor starting point.

And that, my friends, is why MB has had a 45 cent dollar forecast for four years.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.