From ADCM Review:

Financial markets mostly rallied on Thursday, in expectation that the UK referendum would result in a vote to remain in the European Union. On Friday morning, the SPI futures index showed that the Australian share market was set to open up by 60 points, after the Dow Jones index ended Thursday above 18,000 points for the first time in more than two weeks.

The Australian share market climbed by as much as 45 points in the first thirty minutes of trading but then, from the news coming out of the UK, it became clear that the outcome of the vote would be very close. The market turned and it was mostly all down hill for the rest of the day, as Bremain became Brexit.

The Australian market finished the day down by 167.5 points or 3.17%. This performance was mirrored elsewhere around the world and in different markets.

The FTSE 100 finished Friday down by 199.41 points or 3.15% and in the last market to close, the Dow Jones Industrial Index finished the day down by 610.32 points or 3.39%.The reaction in equity markets is unlikely to be over. Morgan Stanley is predicting that European equities will fall by 15% to 20% from where they closed on Thursday.

The reaction in credit markets was more extreme than in equity markets. And if, Morgan Stanley is right about European equities, then there will be more adverse movement in credit markets too.

The European Main CDS index widen by more than 26% on the day or almost 20bps, to close at 94.82bps. And Markit reported that the UK sovereign five year CDS spread widened by 69% to 56bps.

Across the Atlantic, the CDX index moved 14% wider to close at 86.93bps. But the Aussie iTraxx widened by only a little more than 9%, to close at 135.65bps, not far from where it closed only a week earlier.

However, the big four banks were hit harder, with spreads on five year CDS for the banks moving out by more than 15% to 90bps, on the day.

But the performance of UK sovereign CDS spreads should be contrasted with that of Gilts. The ten year UK government bond yield contracted by 29bps to 1.08% per annum.

Yields on ten year bunds went negative, falling by 14bps to -0.05% per annum. The yield on ten year US Treasury bonds fell by 17bps to 1.57% and here and across the Tasman, ten year government bond yields fell by 24bps and 22bps to 2.00% and 2.34% per annum, respectively.

The Euromarket was hit hard with no new corporate bond sales occurring on Friday, and Bloomberg has reported that market participants believe the Euromarket may be closed for weeks. It is expected that there will be no investment grade bond sales until mid-July and junk bond sales could take even longer to return, as investors and issuers consider the ramifications of Brexit.

37.5% of respondents to a Bloomberg survey expect that there will not even be any sovereign bond issuance this week.

The UK currency was hit by the outcome of the vote. After closing on Thursday at the high for the year, of US$1.50 to the pound, it dropped by more than 8% on Friday to finish at US$1.3649 and had gone as low as US$1.33 during the day.

Morgan Stanley is predicting that the currency will go lower in the short term, with an expectation that the pound will move into the US$1.25 to US$1.30 range.

But the greatest and longest lasting impact of the Brexit decision will be felt in the UK economy.

Fitch Ratings said on Friday that the decision will be broadly credit negative across most sectors of the UK economy. Fitch also said that the UK sovereign rating will be reviewed shortly but did not put the ‘AA+’ rating on Rating Watch.

Moody’s Investors Service echoed Fitch’s comments about the negative impact of the decision on the UK economy but went one step further and revised the outlook on the ‘Aa1’ rating assigned to the UK, to negative from stable.

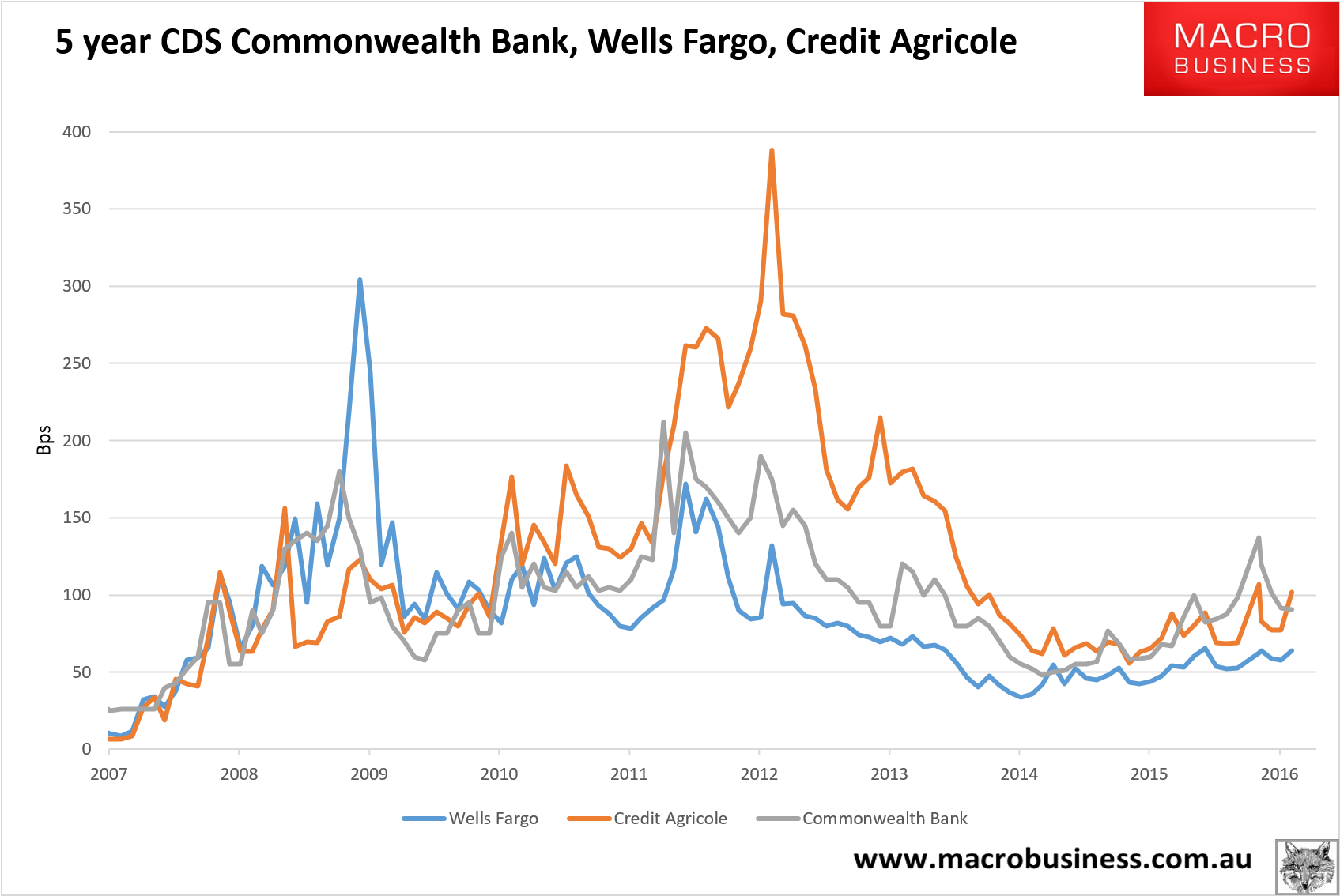

Turning to the MB metrics, the CBA CDS price jumped 15% to 90bps:

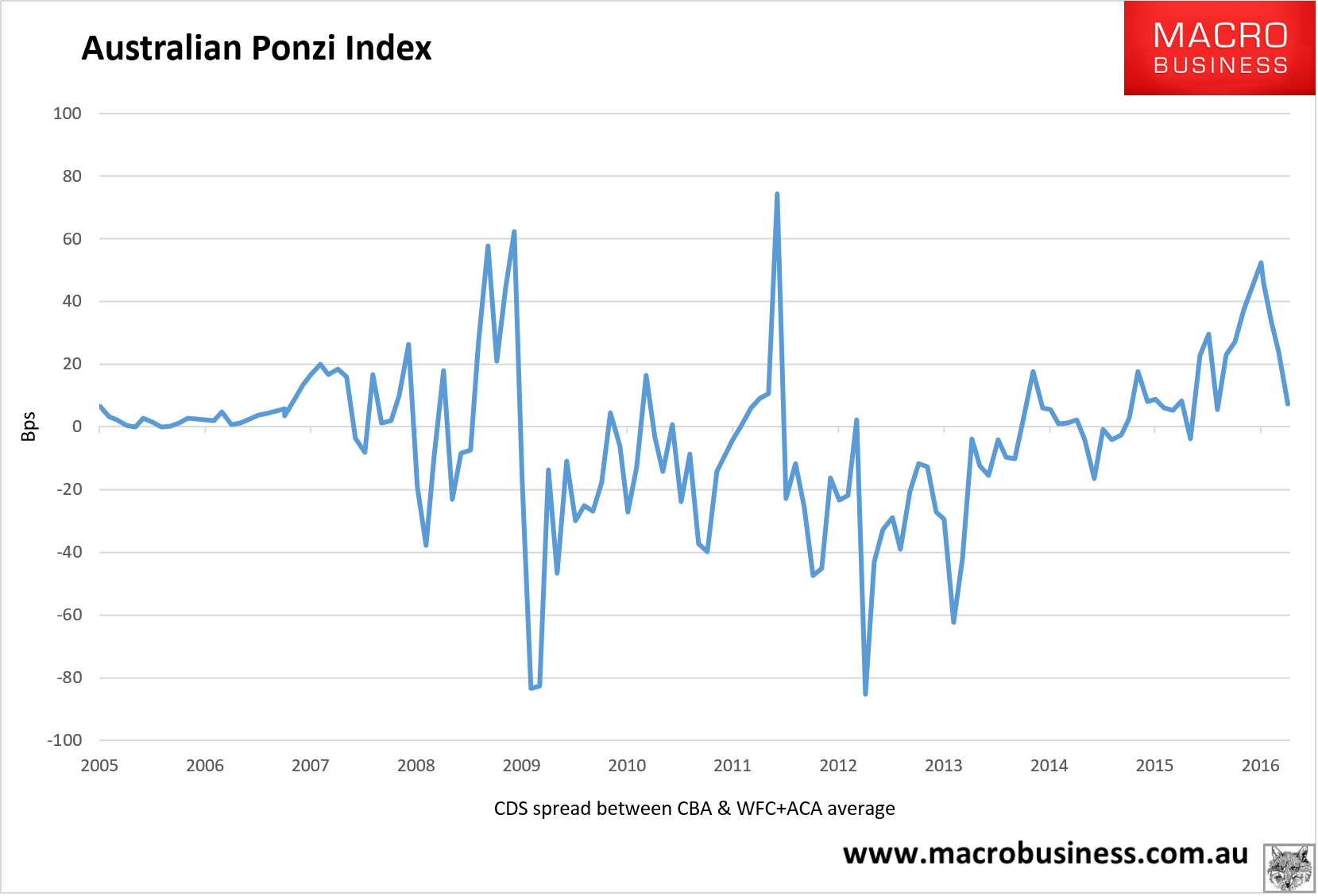

However, our European proxy, Credit Agricole, launched 30% to 102bps while out US proxy, Wells Fargo, was stable. Thus the Australian Ponzi Index actually fell:

So long as China and commodity prices hold up the Aussie banks should trade at a discount to European stress. But if China slows and prices fall, which is the MB outlook for H2, then the funding cost rocket is going to head for the moon.