The all important US jobs report was out Friday night and at first blush was soft given market consensus was for 200k plus (all chart from Calculated Risk):

Total nonfarm payroll employment increased by 160,000 in April, and the unemployment rate was unchanged at 5.0 percent, the U.S. Bureau of Labor Statistics reported today. Job gains occurred in professional and business services, health care, and financial activities. Job losses continued in mining.

… The change in total nonfarm payroll employment for February was revised from +245,000 to +233,000, and the change for March was revised from +215,000 to +208,000. With these revisions, employment gains in February and March combined were 19,000 less than previously reported.

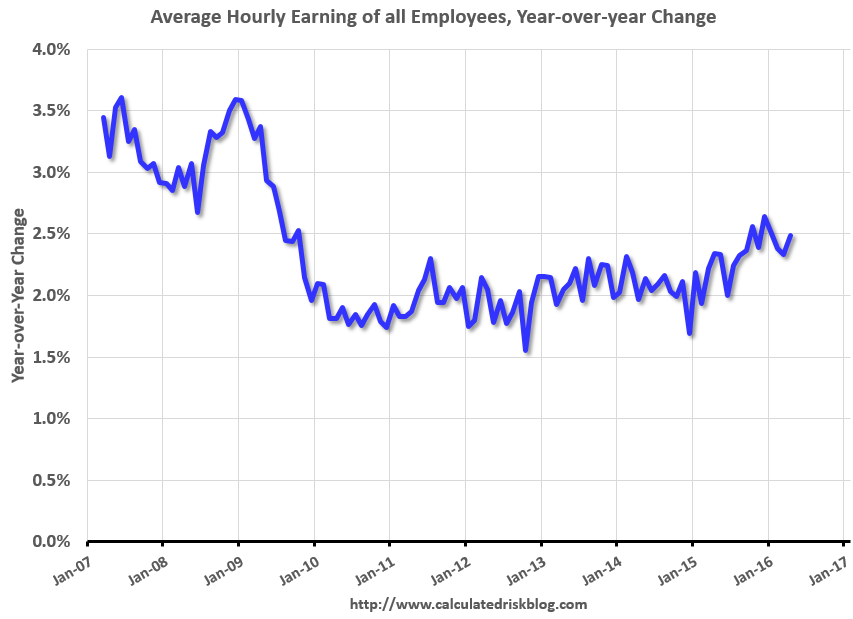

…In April, average hourly earnings for all employees on private nonfarm payrolls increased by 8 cents to $25.53, following an increase of 6 cents in March. Over the year, average hourly earnings have risen by 2.5 percent.

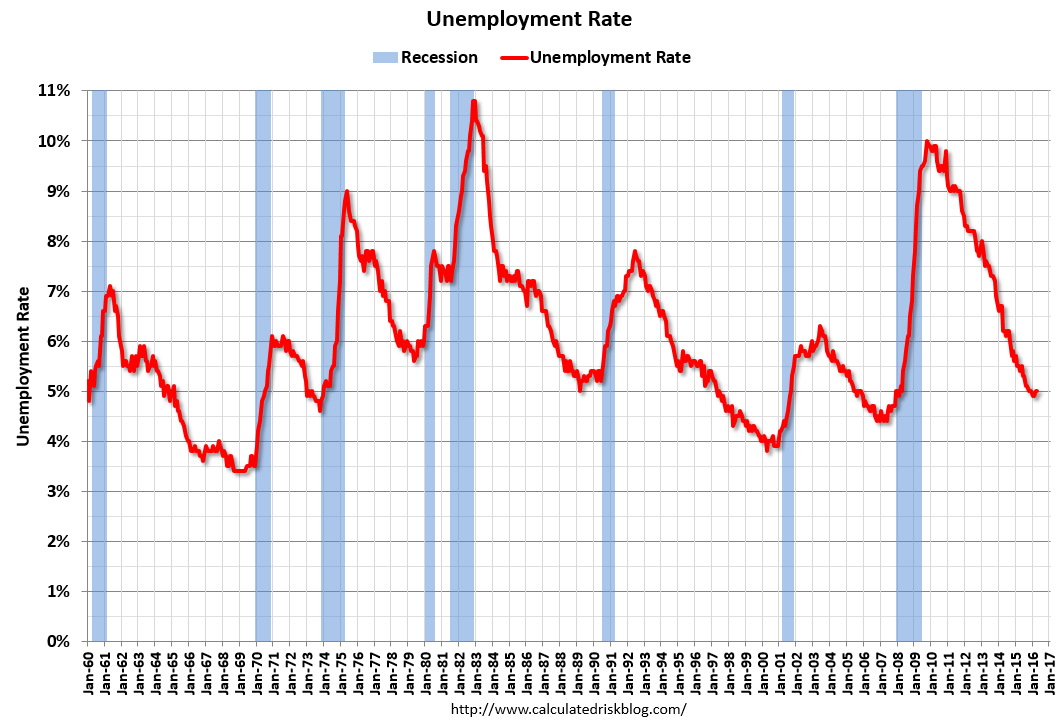

A bit on the soft side but no surprise given the various stresses that the US economy is chewing through in its shale bust. Under the hood it was better. The unemployment rate was still 5%:

Advertisement

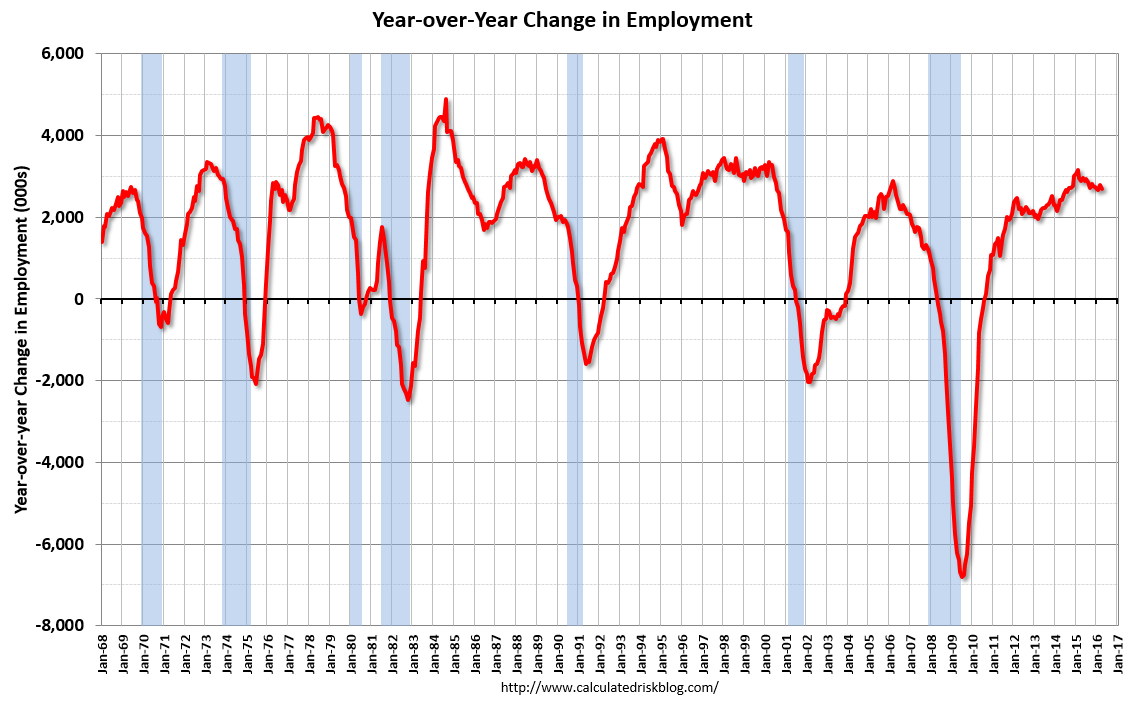

Year on year jobs growth is easing but solid:

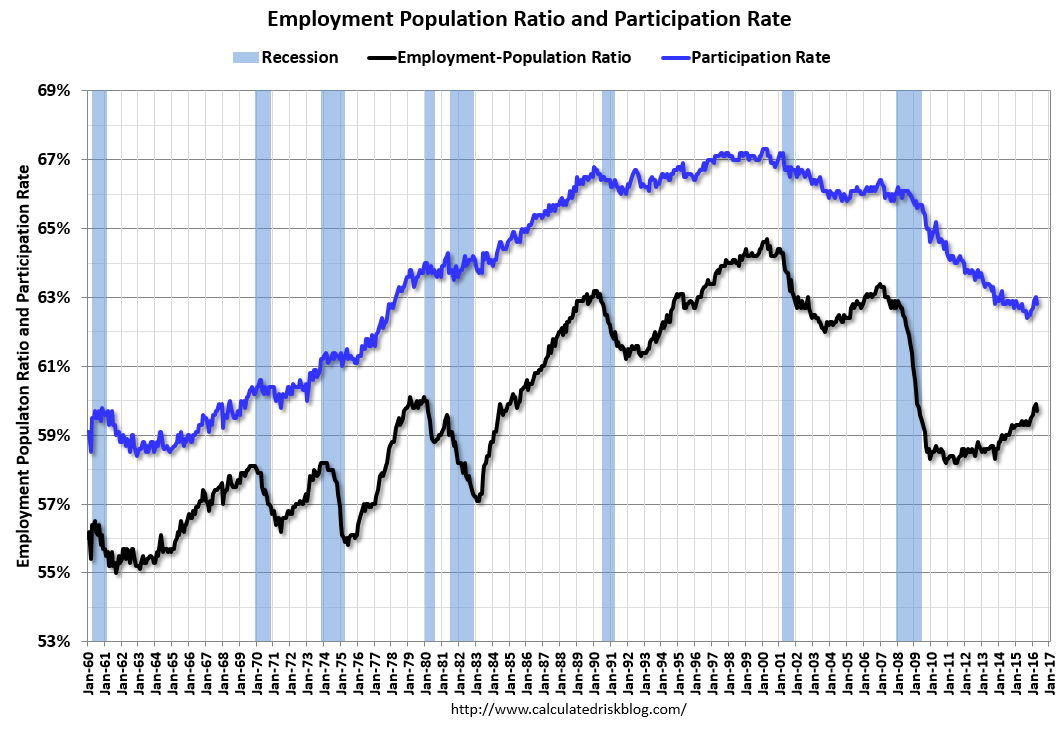

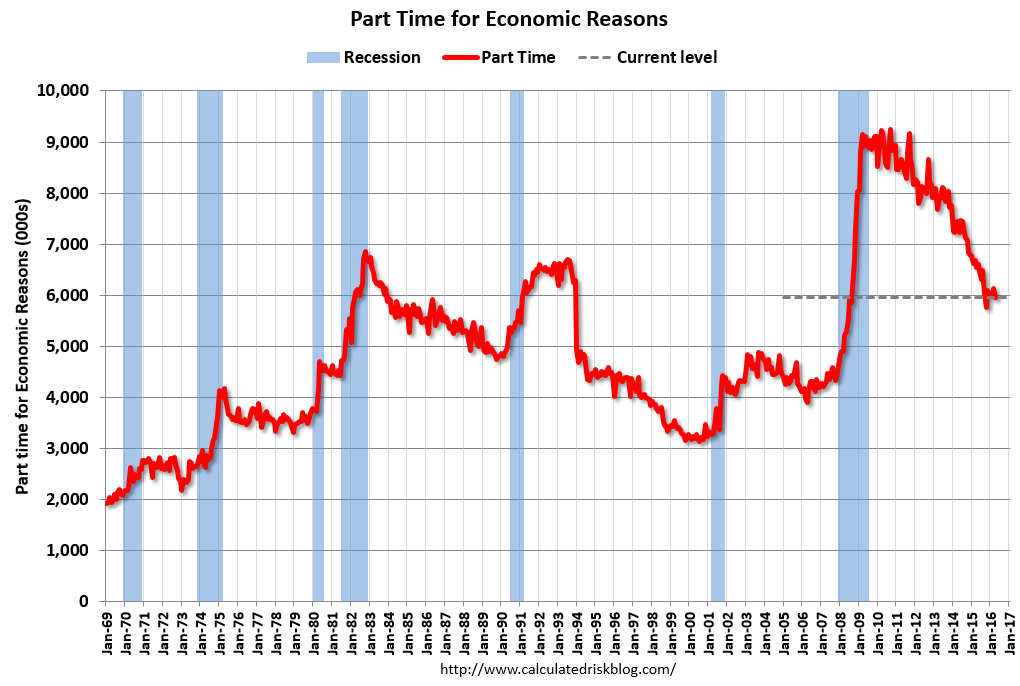

Analytical measures fell within improving trends:

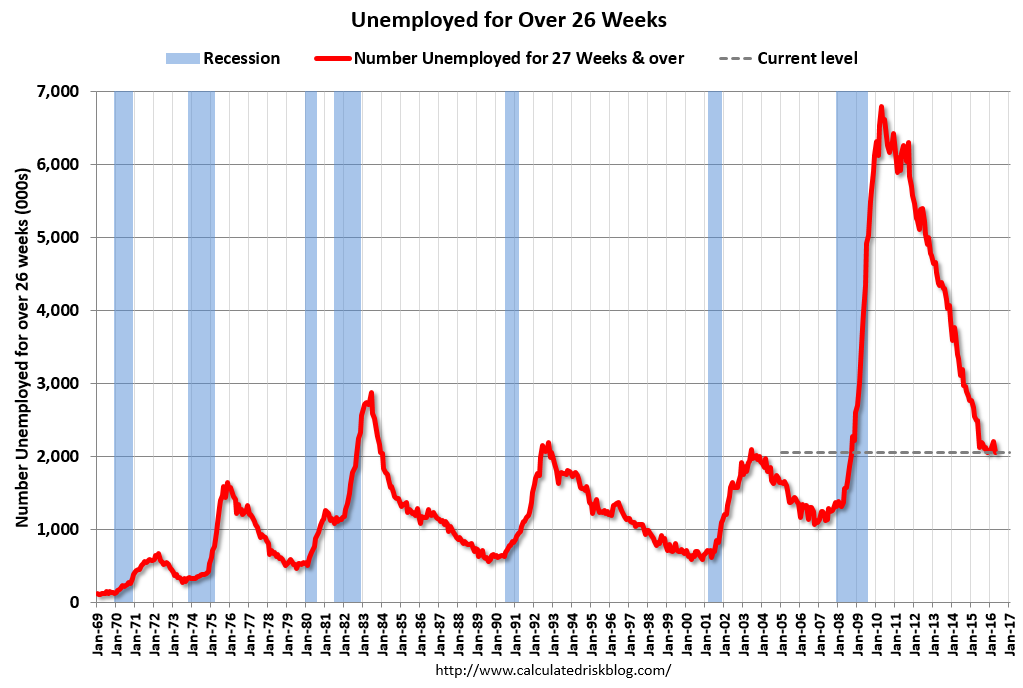

Shadow slack is still falling:

Advertisement

And wages growth returned to an uptrend:

A decent report which is why the US dollar was supported despite the headline miss and a raft of analysts junking their rather silly June rate hike forecasts. We’ll need to see further improvement this year to see another hike but that’s still a reasonable prospect after this report.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.